View this article online: https://www.insurancejournal.com/news/national/2015/07/30/377086.htm

Interest in climate change is becoming an increasingly powerful economic driver, so much so that some see it as an industry in itself whose growth is driven in large part by policymaking.

The $1.5 trillion global “climate change industry” grew at between 17 and 24 percent annually from 2005-2008, slowing to between 4 and 6 percent following the recession with the exception of 2011’s inexplicable 15 percent growth, according to Climate Change Business Journal.

The San Diego, Calif.-based publication includes within that industry nine segments and 38 sub-segments. This encompasses sectors like renewables, green building and hybrid vehicles.

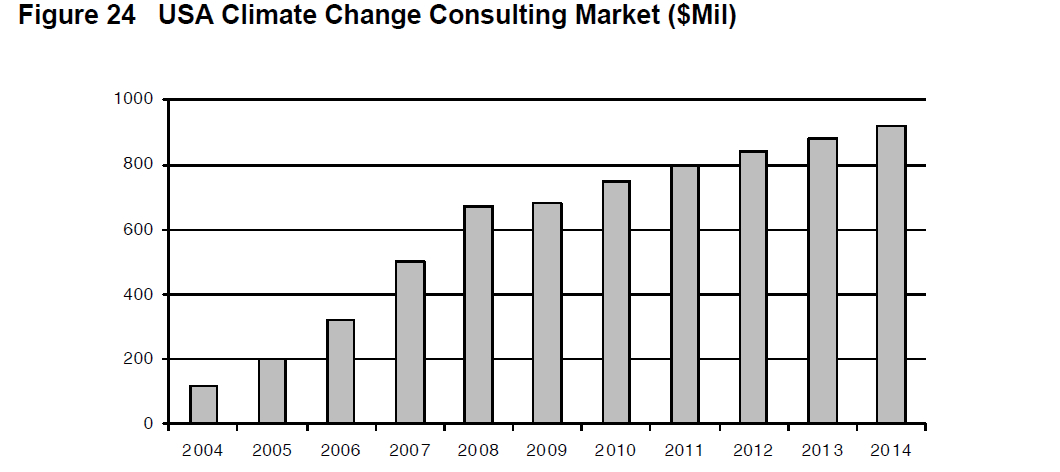

That also includes the climate change consulting market, which a recent report by the journal estimates at $1.9 billion worldwide and $890 million in the U.S.

Included in this sub-segment, which the report shows is one of the fastest growing areas of the climate change industry, are environmental consultants and engineers, risk managers, assurance, as well as legal and other professional services.

Figures for the climate change consulting market are expected to more than double in the next five years, and the report’s authors believe the climate change industry as a whole will have an even steeper and faster growth trajectory than the environmental consulting industry – an industry that in 1976 had billings of $600 million and today generates $27 billion.

This growth in the climate change consulting market will come from newly created consulting firms, as well as from existing firms adding resources to deal with a greater interest in preparing for the impacts of climate change, according to Grant Ferrier, the journal’s editor.

“We see another firm coming out with a dedicated practice area every two or three weeks,” Ferrier said.

The 200 page report on the climate change consulting market came out in April – it’s available for $995 on the publication’s website – but with two major policy turning points upon us it’s worth a new look.

On Monday the final version of the U.S. Environmental Protection Agency Clean Power Plan, national air pollution regulation aimed at curbing carbon emissions from power plants, is scheduled to be released.

Ferrier believes the plan may eventually prove to be a driver of further growth in the industry. That is if the plan withstands any legal challenges from states, industries and entities opposed to it.

“I think the EPA’s Clean Power Plan has a lot more teeth to it than many other attempts of the past,” Ferrier said. “I think we’ll see more (growth) out of that.”

Following this more climate change policy could come out of the United Nations Climate Change Conference in Paris in December, also called COP21 or CMP11.

“I think we’ll see the U.S. and China possibly make more comprehensive commitments rather than at past meetings, where they let the European leadership of the group make commitments while they sat on the sidelines,” Ferrier said.

Policy, or the anticipation of new policy, has been one of the biggest drivers of the industry, the report shows.

A survey of those already in the industry conducted just prior to the U.S. economic downturn, while the industry was a peak growth, shows that 53.5 percent of those polled felt that U.S. or state climate change policy development would be a “strong positive” driver of growth in their business. More than one-third felt that policymaking would have a “very strong positive” impact on their growth.

Much of the growth is expected to come from demand for forward-looking strategic assessments of climate risks, with more corporations making risk assessments to look at the impacts of climate change over the next 10 to 15 years, according to the report.

“Growth in the climate change consulting market continues to shift from greenhouse gas (GHG) management and mitigation to climate change risk assessment and adaptation,” the report states. “Adaptation is increasingly folding into a broader concept of resilience which itself lines up with the even broader goal of sustainability—a focus on how companies, communities and nations can grow economically while enhancing environmental and social values.”

The report credits Superstorm Sandy, along with Hurricane Irene, for jump-starting a new market for climate risk assessment and resiliency solutions in the Northeast and the Gulf Coast.

“I think Sandy definitely stimulated more adaptation planning work,” Ferrier said. “Many more municipalities were requesting climate adaptation study scenarios. (Sandy) was a bit of a shot over the bow of a lot of municipalities.”

Who needs these services? Those who own large property portfolios, big retailers and giant food producers to name a few. In other words it’s anyone who fears losses from more frequent extreme weather events – whether they are climate change related or not is anyone’s guess and a contentious point for some – as well as those who fear business interruption.

Supply chain management is a significant source of new busines for those in the climate change consulting market, according to the report, which states that “climate change consulting for large firms is moving further down into supply chains.”

An example in the report of the need to build climate resilience into supply chains was given by Emilie Mazzacurati of Four Twenty Seven, a newish boutique consultancy focused on climate change risk management and adaptation.

In the report Mazzacurati describes a hypothetical climate risk scenario for a large corporation:

“Let’s say you have a lot of semiconductors being manufactured in a certain region of China that is going to be experiencing higher temperatures and lower water availability. Since manufacturing is very energy and water intensive, you’re going to have a problem there. You may see increasing costs or disruptions in the availability of the products.”

For corporations with several products, a supply chain assessment may be quite a challenge. IBM has disclosed that it has 27,000 suppliers, the report notes.

“Assessing global supply chain impacts for a company like that is probably a two-year study from A to Z, and when you’re done with that you probably have to start over again,” Ferrier said, adding that he believes such assessments are going to be an “ongoing service.”

Not only are corporations beginning to recognize the potential cost impacts of supply chain interruption, but there are reputational impacts to be considered – say it turns out a well-known brand is buying its products or supplies from a far-flung company that’s considered a “gross polluter.”

As Mazzacurati advises in the report, this all requires “a strategic outlook from the risk standpoint.”

Past columns: