Problem: Less than 20% of Floridians in vulnerable areas carry flood insurance. Uninsured flood losses from Hurricane Ian are projected to be as high as $16 billion – almost half as much as insured wind damages, according to CoreLogic, the data analytics firm.

Another problem: Many policyholders with Citizens Property Insurance Corp. who did not carry flood insurance will likely end up in hard-fought claims disputes with the insurer over whether the Ian damage was from wind or water, adding to Citizens’ $3 billion in annual litigation expenses.

Comes now a bold but not-so-new idea that some believe would salve if not solve both issues: Require all Citizens’ policyholders to purchase flood insurance, no matter where they live in Florida. It may sound heavy-handed but has met with approval from at least one industry heavyweight.

“We would strongly support that strategy,” said Mark Friedlander, director of corporate communications for the Insurance Information Institute.

Scott Johnson, an insurance consultant, educator and former lobbyist who has spent decades examining Florida’s insurance issues, said the idea was discussed in the Legislature in the mid-2000s, but never got off the ground. Maybe now is time to revive it, he said.

“Just about everyone is in a flood zone in Florida,” Johnson said, echoing what private flood insurance companies have said for years. Yet, flood insurance is a notoriously hard sell for homeowners who aren’t required to obtain it.

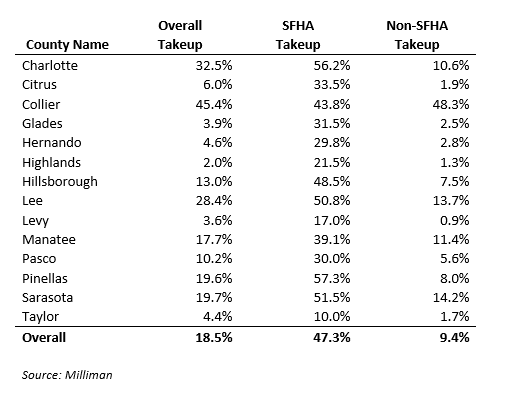

Data from Milliman, the actuarial and data firm, shows that flood coverage in the Federal Emergency Management Agency’s designated flood hazard areas in 14 Florida counties, for single-family homes, ranges from a high of 57% of properties to a low of 10%. Outside the hazard area, but still in relatively low-lying areas in those counties, the vast majority of homes had no flood insurance. (See chart, below).

Requiring NFIP flood insurance would mean that thousands more homeowners would be protected against total losses. But it also would help save Citizens from so many claims disputes, Johnson said. If people receive some payment for losses due to rising waters, they’re less likely to file suit over wind coverage.

“If people don’t have flood insurance, they’ll never agree that all of their losses came from water,” Johnson said.

It’s not just coastal areas that are vulnerable. After Ian hit, dumping as much as 20 inches of rain in parts of Florida, many homes as far inland as Orlando were flooded. And with climate change, some models predict more hurricanes, more rain and more flooding in the years to come, all across the Sunshine State.

A flood coverage requirement also might help solve another problem: Citizens’ runaway growth, fueled in part by its statutory caps on rate increases. The state-created insurer of last resort is now the largest property carrier in the state and has shown no signs of slowing down as other carriers raise premiums significantly or go out of business. As more property owners are forced to spend money on flood coverage, they might find that they can do better with a wind-only policy from a primary market insurer.

Mandating flood would require legislation. When Citizens was created in 2002, its enabling legislation specifically barred such a plan, Citizens officials explained.

“The corporation shall not require the securing of flood insurance as a condition of coverage if the insured or applicant executes a form approved by the office affirming that flood insurance is not provided by the corporation and that if flood insurance is not secured by the applicant or insured in addition to coverage by the corporation, the risk will not be covered for flood damage,” reads Florida Statute 627.351(6)(aa).

Changing that may not be so far-fetched. A number of insurance industry insiders have said that more than a few Florida lawmakers are contemplating another special session, perhaps in December, to address the continuing insurance crisis in the state. The flood insurance mandate could be one of several changes to Citizens’ statutes and regulations, some have speculated. And there’s precedent for rapid reforms: At the May special session, a package of reforms sailed through the three-day gathering with little dissent and few amendments.

Some Citizens officials aren’t so hot on the idea. CEO Barry Gilway said “it is and should be a homeowner’s decision based on their exposure, risk appetite and cost.”

Citizens Board member Jason Butts, a Palm Harbor insurance agent and vice president with SimplyIOA, formerly known as the Insurance Office of America, said the idea has not been broached at Citizens’ meetings. “But it could lead to some discussions.”

He noted that “it’s a great idea for everyone to have flood insurance, especially in Florida.” But mandating it would be up to the Legislature.

The cost of flood, on top of a wind or all perils policy, may be prohibitive for some policyholders, but not for others. A quote from Neptune Flood Insurance, for example, showed that for a modest home in Cape Coral, in the heart of the Hurricane Ian strike zone, with one previous flood claim, coverage could cost more than $10,000 annually. If the house is elevated on stilts, though, the cost drops to about $2,200 a year.

And in an area on higher ground, in slightly hilly northwest Florida, the premium is about $545 per year.

Others in the industry said Johnson’s idea is provocative and worthy of consideration.

Don Brown, a lobbyist, former state representative and now a member of the Florida Building Commission, said that requiring flood insurance may not solve everything, though. Some homeowners would still be prone to argue that a Citizens’ wind policy should cover damage above the $250,000 coverage limit provided by an NFIP flood policy.

Getting some type of payout to the insured quickly would help reduce disputes, “but it wouldn’t eliminate the problem completely,” Brown said. “There would still be some conflict there.”

He agreed that most properties in Florida need flood insurance, even if owners think they are outside of the historic floodplains.

Johnson argued that even if a condominium unit owner is on an upper floor of a high-rise building, flood insurance can prove to be beneficial. Otherwise, all unit owners could end up paying a large assessment to cover flood damage on the first floor of the building, he noted.

Top photo: Resident Mike Kelley navigates flooded streets in Geneva, Florida, when Lake Harney and the St. Johns River left their banks after historic levels of rainfall from Hurricane Ian. (Joe Burbank/Orlando Sentinel)

Topics Flood

Was this article valuable?

Here are more articles you may enjoy.

California Chiropractor Sentenced to 54 Years for $150M Workers’ Comp Scheme

California Chiropractor Sentenced to 54 Years for $150M Workers’ Comp Scheme  Vintage Ferrari Owners’ Favorite Mechanic Charged With Theft, Fraud

Vintage Ferrari Owners’ Favorite Mechanic Charged With Theft, Fraud  USAA to Lay Off 220 Employees

USAA to Lay Off 220 Employees  FBI Says Chinese Hackers Preparing to Attack US Infrastructure

FBI Says Chinese Hackers Preparing to Attack US Infrastructure