View this article online: https://www.insurancejournal.com/magazines/mag-features/2016/03/07/400394.htm

Private passenger automobile insurance remains one of the most competitive segments in the U.S. property/casualty industry, with a number of large, well capitalized organizations battling for market share and searching for competitive advantages and better profits through pricing and risk selection, advertising, and claims management efficiency.

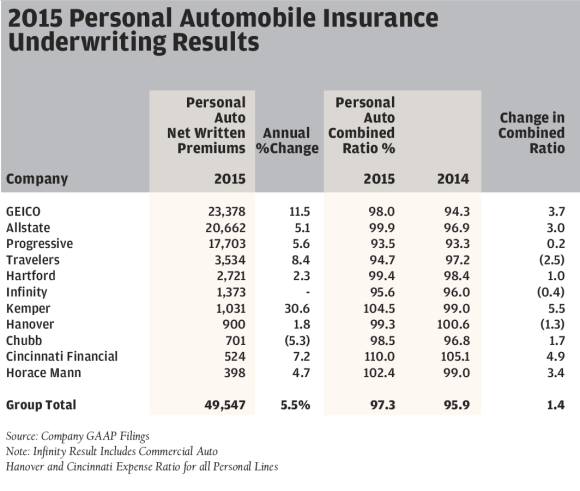

Auto insurers continue to generate relatively robust premium growth and benefits from price increases, but top line growth has not translated into better underwriting performance in 2015. The personal auto insurance combined ratio rose by 1.4 percentage points in 2015 to 97.3 percent for a group of 10 publicly traded insurers. Underwriting performance deteriorated despite over 5 percent annual growth in segment written premiums for the group, as well as a modest decline in the expense ratio and reduced natural catastrophe related losses compared with the previous year.

The property/casualty industry in aggregate has generated consistent moderate statutory underwriting losses in personal auto for the last six consecutive years, including a projected combined ratio above 102 percent in 2015. Several large non-public insurers that tend to have less ambitious return objectives drive up the industry results compared to the group of public insurers. Market leader State Farm reported a statutory underwriting margin of -12 percent in personal auto for 2015.

Recently, a number of insurers have pointed to claims frequency trends shifting unfavorably as a contributor towards higher loss ratios. The Allstate Corp. reported a 5.9 percent increase in bodily injury frequency and 6.3 percent increase in property damage frequency in full year 2015. Hartford Financial Services Group Inc. reported that frequency in auto business rose to 3.5-4 percent in the second half of 2015. In Hartford’s recent earnings conference call, the company suggested that this frequency change may represent a new norm that will need to be incorporated into future rate filings.

Development of additional safety features in cars, such as anti-lock brakes, back up cameras and parking assist have promoted accident reductions, making this shift in frequency a bit unusual. While determining specific causes behind changes in claims trends is difficult, an increase in miles driven as gasoline prices sharply declined and the employed labor force expanded is a likely contributing factor. Greater prevalence of distracted driving with Americans ever growing dependence on handheld electronic devices may be another contributor to higher claims frequency.

Profit improvement in private passenger automobile has been hindered for some time by periodic increases in claims severity. Rising auto claims severity is attributable to medical cost inflation, and higher repair bills. New and used automobile prices continue to increase. The cost of maintaining and repairing vehicles made of more technologically sophisticated materials and replacing more complex devices and equipment within a vehicle is also rising.

Claims severity in 2015 moved higher in auto insurance in major coverages including: bodily injury, property damage and collision. GEICO Corp. reported claims severity increased 4-5 percent for property damage and collision claims, and 6-7 percent for bodily injury.

Individual underwriter 2015 results in personal auto insurance varied considerably. Only three companies, Travelers Cos. Inc., Infinity Property & Casualty Corp., and The Hanover Insurance Group reported year-over-year improvement in GAAP basis auto underwriting profits. Progressive Corp., a strong performer and fourth largest auto writer by premium, reported a 93.5 percent auto combined ratio for the year.

In contrast the second largest private auto underwriter, GEICO, reported a 3.7 point auto combined ratio increase in 2015, and third largest auto underwriter, Allstate, reported a three point increase in the auto combined ratio in 2015 to essentially break-even results. Three underwriters, Kemper Corp., Cincinnati Financial and Horace Mann reported combined ratios in personal auto insurance above 100 percent for the year.

Looking ahead to 2016, personal auto results may show moderate improvement, but will ultimately hinge on how well insurance pricing keeps pace with loss trends that are likely to continue to outpace general inflation.

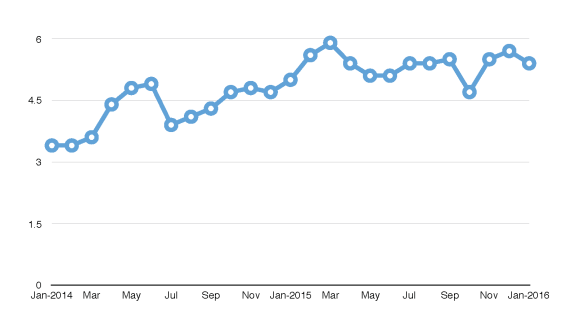

Premium rate trends are currently more favorable in personal lines relative to commercial lines, as publicly traded insurers report regular renewal rate increases in quarterly earnings disclosures, while most commercial segments are experiencing flat to declining pricing trends. Consumer Price Index (CPI) data shows that costs for motor vehicle insurance continues to increase and the monthly change averaged 5.4 percent through all of 2015.

Monthly Change in Motor Vehicle Insurance Costs

Source: Bureau of Labor Statistics: Consumer Price Index Statistics Insurance information Institute

Besides the perpetual striving for pricing adequacy, personal auto insurers face other obstacles that could hinder future profitability, including reduced investment earnings amidst continued low fixed income market asset yields and a weakening equity market, balancing technology improvement with expense control objectives.

Automobile insurance premium rates will continue to rise in the near term as targeting rate increases in response to recent loss experience is a key theme in auto underwriters’ recent remarks to investors.