Treating cyber risk as a standalone insurance market holds the promise of unlocking the potential for meaningful coverage for both insurers and buyers, according to a new report by JLT Re and JLT Specialty Limited.

According to the report released at the annual RIMS Conference that is getting underway in Philadelphia, buyers are clamoring for better cyber products to address the growing and complex risks of cyber, while underwriters are being cautious over concerns around “unquantified cyber exposures potentially buried in traditional policies.”

JLT said it believes considering cyber as a standalone line of business rather than a peril will result in more resilience to cyber risk in the (re)insurance market and this shift will benefit insurance buyers in the form of “greater certainty, expertise, capacity and stability from the (re)insurance market in a complex and growing risk area.”

“Cyber exposures have grown considerably for companies of all sizes and domiciles in recent years, causing business costs to rise sharply,” said David Flandro, global head of Analytics, JLT Re. “Companies face challenges in understanding their exposures and the type of insurance cover needed as the underlying drivers of cyber risks frequently change, requiring insurers and brokers to explain and quantify these exposures as clearly as possible. Increased coordination and collaboration between key markets will be crucial in meeting evolving demands and unlocking the huge potential associated with cyber for the benefit of companies and carriers alike.”

JLT notes that insurance approaches for cyber risk can differ considerably from one company to the next, a reflection of the view that cyber can either be considered a peril that falls within traditional property/casualty products or a line of coverage in its own right.

JLT views a standalone cyber market as a way to address both buyers’ changing needs and insurers’ uncertainty.

“As more premiums flow into the standalone market, carriers will be able to evaluate and price risks more accurately as good-quality claims data and sophisticated modelling tools become increasingly accessible,” said Sarah Stephens, head of Cyber, Technology and Media E&O for JLT.

“This, in turn, will help ensure the market is better placed to trade through future systemic losses by encouraging innovative reinsurance and insurance-linked securities (ILS) structures. ”

Stephens said governmental support is also likely to be needed in back-stopping some of the more catastrophic loss scenarios.

She said a more robust cyber market, with comprehensive, standalone policies at its core, would also help “eliminate the risk of silent exposures and, ultimately, make the market more resilient to future catastrophic cyber losses.”

She said given the strong likelihood of a major cyber event in future, the market needs to prevent a situation where (re)insurance buyers are faced with a dearth of capacity as happened in the aftermath of the 9/11 attacks.

Given the complexity of cyber risks, access to reinsurance capital is essential in alleviating the primary market’s aggregation burden and supporting the innovative cover needed for future cyber risks, according to JLT.

“There is sufficient reinsurance capacity for the current cyber insurance market and increased reinsurer appetite for cyber risk bodes well for long-term growth prospects,” according to Chris Bennett, partner, London Market and International Non-Marine, Cyber Treaty for JLT Re. “New approaches have emerged in recent years as competition between reinsurance companies has stiffened, making non-proportional structures such as excess-of-loss, stop-loss and aggregate covers as commonplace today as the more traditional quota share arrangements.”

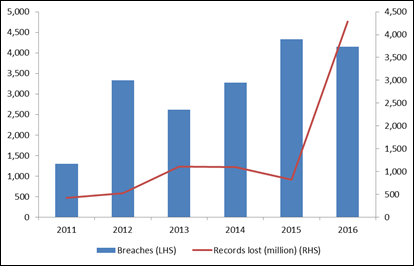

The report notes that cyber risk has changed since the first policy was underwritten around the turn of the century and it claims the market now needs to respond decisively to the changing scale and scope of cyber risk. For example, data breaches have become more frequent in the last five years, with the number of reported data breaches globally rising by more than 300 percent.

The report also cites considerable concern over the scalability of the risk, where one cyber event is capable of triggering multiple claims under different policies at national, or even global, levels. As technologies become further embedded in the operations and strategies of organizations across all geographies and sectors, malicious actors will increasingly look to exploit the vulnerabilities associated with innovations such as the Internet of Things, cloud computing, autonomous vehicles, machine automation and connected devices.

“Market participants have begun to explore how catastrophic cyber risks such as systemic cloud service provider failures or targeted cyber attacks on power grids could impact businesses and risk carriers,” said Flandro. “These efforts have highlighted the real potential for multi-billion dollar (re)insured pay-outs. Products designed to mitigate such systemic cyber risk accumulations are less readily available, but considerable progress can be achieved by drawing on the expertise that exists in the standalone cyber market.”

Topics Cyber Reinsurance Market

Was this article valuable?

Here are more articles you may enjoy.

Florida Regulators Crack the Whip on Auto Warranty Firm, Fake Certificates of Insurance

Florida Regulators Crack the Whip on Auto Warranty Firm, Fake Certificates of Insurance  Sompo Receives Regulatory Approvals to Acquire Aspen Insurance in $3.5B Deal

Sompo Receives Regulatory Approvals to Acquire Aspen Insurance in $3.5B Deal  Former Broker, Co-Defendant Sentenced to 20 Years in Fraudulent ACA Sign-Ups

Former Broker, Co-Defendant Sentenced to 20 Years in Fraudulent ACA Sign-Ups