New requirements regarding the implementation of changes in workers’ compensation loss costs have been passed by the South Carolina Legislature, and the insurance department is reminding insurers to ensure they follow the new filing rules as loss cost increases will take effect Sept. 1.

The South Carolina Department of Insurance (SCDOI) approved a loss cost increase of 2.5 percent put forth by the National Council of Compensation Insurers (NCCI) for workers’ comp policies in the state as of Sept. 1, 2016. NCCI, South Carolina’s workers’ comp insurance rating organization, files prospective loss costs with SCDOI for approval. Once approved, insurers writing workers’ comp in the state must adopt the new loss costs. Loss costs represent claims experience, which is a main driver of workers’ comp costs. Claims experience is measured by the number of workplace injuries and the average cost of injuries.

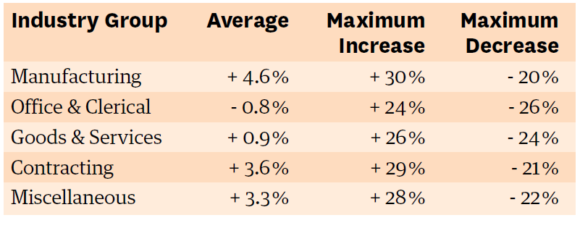

The exact loss cost changes for South Carolina vary depending on the following classifications:

In a July 6 bulletin from SCDOI Director Raymond Farmer, all insurers transacting workers’ comp insurance business in South Carolina were notified of the loss cost changes, as well as changes passed by the Legislature this year regarding new procedures for workers’ comp insurers filing loss cost adoptions or loss costs multipliers.

Insurers writing workers’ comp in the state must now file their intent to adopt NCCI’s filing within 60 days of the approval date of the new loss costs in accordance with the new law. Insurers must also now implement the latest NCCI loss costs within 120 days from the new loss cost effective date. SCDOI approved NCCI’s South Carolina loss cost filing on June 21, giving insurers until Aug. 20 to make their filing to adopt the new loss costs and until Dec. 30, 2016 to implement the loss costs adoption.

The new law, which amends the 1976 Code of Laws of South Carolina relating to rate filing requirements, also requires an insurer to file its multiplier for expenses, assessments, profit and contingencies within 60 days before using a new multiplier. The section relating to the filing requirements for rating organization members was also amended to establish that an insurer writing workers’ comp insurance may satisfy its filing obligation by becoming a member of or subscriber to a licensed rating organization.

SCDOI recommended the legislative changes in its “Workers’ Compensation Insurance Coverage: The State of the South Carolina Market” report released in Dec. 2015, saying they would regulate the marketplace in a “more efficient manner” and “codify the current regulatory practice.”

SCDOI has posted a timeline in under the “Insurers” section on its website to help insurers understand the deadlines of the new requirements, as well as information on the new procedures. It also directs insurers to how they can prepare and complete rate, rule and form filings, which are submitted via the State Electronic Rate Form Filing (SERFF) system. Filings must be submitted by insurer and by line of business.

Farmer said the overall loss cost increase of 2.5 percent comes on the heels of the 1.9 percent increase in 2015, and he hopes that it’s not an indication of a trend towards future increases, despite some concerning factors.

“We have had higher medical costs here for the last several years – that is the main reason for the increase,” Farmer said. “Medical costs, whether for individuals or group or workers’ comp continue to rise, so when you look at that and review, it isn’t a surprise.”

SCDOI characterized the workers’ comp market as stable in its December 2015 report, with new carriers entering the marketplace “continuously improving the availability of coverage.”

Rate levels for the state’s assigned risk plan, which is also administered by NCCI for employers who are unable to procure workers’ comp coverage in the voluntary market, were also approved to be raised by an overall 6 percent. The increase was in response to a revision request by NCCI for corrective action because of excessive losses within the assigned risk plan that jeopardized the ability of the plan to operate as a self-funded mechanism. South Carolina law requires the assigned risk plan be able to operate on a self-funded basis. Accordingly, rates may be adjusted to the assigned risk plan as necessary to ensure that it can continue to operate in such a manner.

Topics Trends Carriers Legislation Profit Loss Workers' Compensation South Carolina

Was this article valuable?

Here are more articles you may enjoy.

Preparing for an AI Native Future

Preparing for an AI Native Future  Fla. Commissioner Offers Major Changes to Citizens’ Commercial Clearinghouse Plan

Fla. Commissioner Offers Major Changes to Citizens’ Commercial Clearinghouse Plan  World’s Growing Civil Unrest Has an Insurance Sting

World’s Growing Civil Unrest Has an Insurance Sting