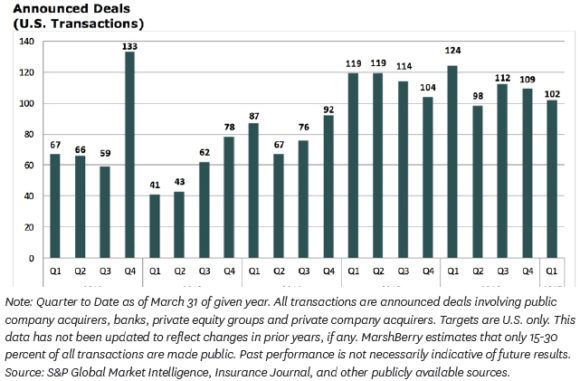

Deal count for the first quarter of 2017 was down relative to the first quarter of both 2015 and 2016. There were 102 announced transactions in the first quarter of 2017, compared to 124 in the first quarter of 2016 (a decrease of 13.8 percent). Forty-three deals closed in January; 29 in February; and 30 in March. By comparison, historical first quarter deal counts in the past five years were 41 in 2013, 87 in 2014, 119 in 2015, 124 in 2016, and 102 in 2017 (average of 94.6 per year).

For the first quarter of 2017, 52 percent of all acquired agencies were property/casualty firms, 31 percent were multi-line agencies and 17 percent were employee benefits firms. Specialty distributors made up 18.6 percent of the total deal activity year-to-date. This is a slight increase compared to 2016, when 15.8 percent of recorded transactions were with specialty distributors.

Private-equity backed buyers continue to drive the market with 44 closed transactions through March 2017. However, this represents a 29.5 percent decrease compared to the first quarter of 2016. This represented 43 percent of all deal activity in the first quarter of 2017. Independent agencies completed 33 transactions and public brokers accounted for 13 deals in the same period. Insurance carriers, banks and thrifts and other buyers closed 12 deals in the first quarter of 2016.

The top five buyers for the year represented 33.3 percent of total deal activity through the first quarter of 2017. The top 10 accounted for 48 percent.

BroadStreet Partners Inc. took over the top spot as the most active acquirer with 11 closed transactions. BroadStreet typically applies a co-ownership structure to its acquisitions and allows agency owners and/or key employees to retain some ownership.

Arthur J. Gallagher (AJG) was the second most active acquirer and the most active public broker in the marketplace with nine deal closings in the first quarter of 2017. AJG’s acquisitions were evenly spread throughout the country and consisted of both retail and wholesale agencies. AJG also closed two deals in Australia in the first quarter of 2017.

Hub International Ltd. was the third most active buyer with seven closed transactions in the first quarter of 2017. Hub purchased four agencies in the West, two agencies in the South/Southeast, and one in Midwest/East. Hub continued to expand internationally by purchasing two agencies in Canada. Hub has closed 126 transactions in the United States since 2012.

Hub International Ltd. was the third most active buyer with seven closed transactions in the first quarter of 2017. Hub purchased four agencies in the West, two agencies in the South/Southeast, and one in Midwest/East. Hub continued to expand internationally by purchasing two agencies in Canada. Hub has closed 126 transactions in the United States since 2012.

Baldwin Risk Partners (BKS), a new private equity backed buyer formed in 2012, closed four deals in the first quarter of 2017. BKS is headquartered Tampa, Fla., and all four deals were with Florida agencies.

Acquisition activity is down from the pace set in 2015 and 2016, but demand remains high as there are more buyers than in any time in history. Private equity backed brokers continue to drive the market, while public brokers and independent brokers continue to be aggressive in their search for growth and talent. With private equity facing large sums of capital yet to be deployed, we believe that the acquisition market will remain healthy during the rest of 2017.

Securities offered through MarshBerry Capita, Inc., Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co. Inc. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 (440-354-3230). Except where otherwise indicated, the information provided is based on matters as they exist as of the date of preparation. Past performance is not necessarily indicative of future results.

Was this article valuable?

Here are more articles you may enjoy.

US Supreme Court Rejects Trump’s Global Tariffs

US Supreme Court Rejects Trump’s Global Tariffs  AI Claim Assistant Now Taking Auto Damage Claims Calls at Travelers

AI Claim Assistant Now Taking Auto Damage Claims Calls at Travelers  Viewpoint: Runoff Specialists Have Evolved Into Key Strategic Partners for Insurers

Viewpoint: Runoff Specialists Have Evolved Into Key Strategic Partners for Insurers

From This Issue