Insurers with the strongest new business yield rates also have strong combined ratios in personal auto in the J.D. Power 2017 U.S. Insurance Shopping Study.

We define new business yield rates as the proportion of prospective customers who purchase with the insurer after shopping.

Three companies emerge as leaders in profitability and new business yield in personal auto insurance. GEICO, Progressive, and Automobile Club of Southern California, a AAA insurer, all maintain a combined ratio less than 100 (in 2015) while acquiring new business more successfully than the other insurers included in the study. Their yield rates are 7.6 percent (GEICO), 4.3 percent (Progressive) and 4.1 percent (ACSC), respectively—well above the industry average of 2.4 percent (Figure 1).

Looking at the direct premium written (DPW) growth of insurers included in the “2017 U.S. Insurance Shopping Study,” GEICO has the highest three-year (2013-2015) DPW compound annual growth rate (CAGR) for private passenger auto, of any brand profiled in the study, at 7.0 percent for private passenger auto. The average CAGR for brands included in the study is 2.5 percent. (Source: J.D. Power Insurance Performance Portal)

Not surprisingly, the three brands (GEICO, Progressive, and ACSC) with the strongest yield rates in the study have above average direct premium growth rates for private passenger auto.

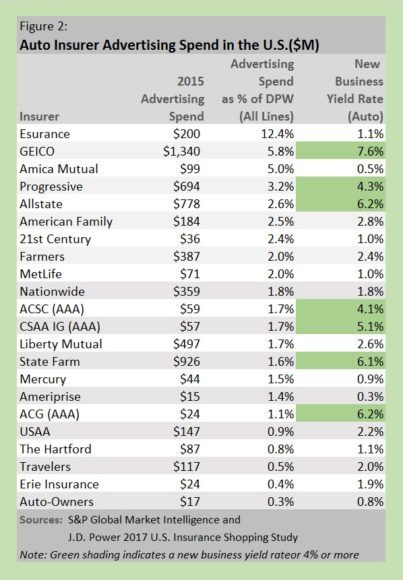

Advertising Spend Impact on New Business Yield Rates

Advertising is a critical component to any business and industry, especially so for a service based industry like insurance. Businesses spend billions of dollars on advertising in the United States every year. According to IHS Global Insight Inc.’s report (IHS Economics and Country Risk, Economic Impact of Advertising in the United States, March 2015. ihs.com), total U.S. advertising expenditures in 2015 reached $311.6 billion and were expected to increase to $332.9 billion by 2017.

The property/casualty insurance industry alone spent $6.5 billion on advertising in 2015, with GEICO the only brand to surpass the $1 billion mark, spending $1.3 billion. (Source: J.D. Power calculations based on S&P Global Market Intelligence Platform) See Figure 2 for advertising spend by brands included in the “2017 U.S. Insurance Shopping Study.” New business yield rates for personal auto vary widely across insurers, as does advertising spend compared to total direct premium written (all lines) in 2015.

As previously mentioned, GEICO, Progressive, and ACSC (AAA) are the only three insurers in the study to achieve an auto new business yield rate of more than 4 percent and a 2015 combined ratio of less than 100. GEICO and Progressive both target all regions of the United States and have well-known advertising campaigns using such characters as Progressive’s Flo and the GEICO Gecko. ACSC (AAA) is a regional insurer, but is part of the AAA brand, which utilizes products such as roadside assistance and the AAA brand discounts in its advertising. In recent years, ACSC (AAA) has begun to focus more on services like planning trips, discounts on clothes, restaurants, event tickets, and hotel rooms in its advertisements—much more than just roadside assistance.

The analysis in Figure 2 demonstrates that it is not necessarily the amount of money spent on advertising that influences the new business yield rate, but other factors such as advertisement content, advertisement demographics targeted, word of mouth, brand reputation and other items. Insurers spending large amounts of money on advertising should examine factors influencing below-industry average new business yield rates and potentially realign spending.

Ad Spend, Customer Satisfaction Not Driving Higher New Customer Rates

A strong combined ratio and a higher new customer yield rate appear to be related for private passenger auto insurance. Brands with the strongest combined ratios also have the highest new customer yield rates; however, dollar amount spent on advertising and overall purchase experience satisfaction don’t necessarily align. Insurers with the strongest yield rates have near-industry average Purchase Experience Satisfaction scores, yet they are still gaining the most new customers. Is it that these brands are most effective in their advertising and pricing, allowing customers to overlook an average purchase experience?

Brands that spend the most on advertising per direct premium written (DPW) are not necessarily seeing a payoff in new customer acquisition, as shown in Figure 2. Brands need to consider advertising content, channel method, and effectiveness rather than just quantity and spend.

Brands should also take a hard look at costs spent on customer acquisition and balance the costs of customer satisfaction initiatives, advertising, and operational/staffing areas and understand how moving the lever on one will impact all. What are the appropriate levels of investment for each of these items which will lead to the company achieving maximum profitability and new customer yields?

Customer satisfaction is still crucial, especially in retaining the hard-fought-for new customers as insurers seek to avoid future churn.

This article originally appeared on CarrierManagement.com.

Topics USA Carriers Auto Underwriting

Was this article valuable?

Here are more articles you may enjoy.

Judge Tosses Buffalo Wild Wings Lawsuit That Has ‘No Meat on Its Bones’

Judge Tosses Buffalo Wild Wings Lawsuit That Has ‘No Meat on Its Bones’  Viewpoint: Runoff Specialists Have Evolved Into Key Strategic Partners for Insurers

Viewpoint: Runoff Specialists Have Evolved Into Key Strategic Partners for Insurers  CFC Owners Said to Tap Banks for Sale, IPO of £5 Billion Insurer

CFC Owners Said to Tap Banks for Sale, IPO of £5 Billion Insurer  Sompo Receives Regulatory Approvals to Acquire Aspen Insurance in $3.5B Deal

Sompo Receives Regulatory Approvals to Acquire Aspen Insurance in $3.5B Deal