The Agent’s Role as Advisor and Risk Manager

Editor’s note: This is the last of a three-part series to explain insurers’ requirements for building updates and to help agents advise clients on mitigating risks inherent in older buildings. The first article addressed aging electrical systems and appeared in the Feb. 25 edition of Insurance Journal. The second article, which offered advice for aging plumbing systems, appeared in the March 25 edition. This final installment covers heating, ventilation, air conditioning (HVAC) and roofing systems.

The older a building, the more likely it is to have serious defects, particularly in critical building systems such as electrical, plumbing, HVAC and roofing. Older buildings generate more claims than younger properties, especially if they have not been well-maintained or if their building systems have not been updated.

This is why an insurer will ask a policyholder about the age of the original building, the age of renovations or additions and the age and condition of critical building systems. The information helps the insurer price the coverage fairly, and brings to light any serious defects to be corrected. In the case of serious roofing defects, such as failure-prone fiber-cement tiles, or when a major update is needed, like an aging rooftop air-conditioning unit, the insurer may request the upgrades as a condition of coverage.

Heating, Ventilation and Air-Conditioning (HVAC) Systems

Heating, ventilation and air conditioning (HVAC) systems typically require updating only on as “as-needed” basis, such as when components fail due to age or inadequate maintenance, or when the discovery of material weaknesses or failures during inspections warrants repairs and replacements.

A building’s heating system — furnace, boiler or heat pump — can last for many years, with proper maintenance. Heating equipment generates relatively few claims.

The primary loss driver in the HVAC equation is the air conditioning system, particularly roof-top units, which are especially vulnerable to damage and neglect. Roof-top AC units, which are used to cool nearly half of all commercial floor space in the United States, need special care and maintenance to guard against damage caused by dust, debris and, in certain areas of the country, damage caused by hail. (See Figure 1)

Photo courtesy of CR Roberts Consulting Engineers.

An air conditioner is designed so that air can flow freely and smoothly over the fins and through the condenser coil. When the fins are distorted or damaged, air cannot flow easily to the coil. In cases of severe damage, the airflow to the coil may be blocked altogether. A few bent fins will not typically affect the AC unit, but when extensive fin damage reduces or blocks the air flow, the unit cannot operate efficiently. Over time, the damaged unit will function less efficiently, and may fail completely. Because the damaged unit must run for longer periods and at hotter temperatures to produce cool air to meet demand, the cost of operating and maintaining the damaged AC will rise over time.

Outdoor air conditioning units can be protected from hail damage with the installation of hail guards, also called hail shields, which are designed to protect the condenser coil from contact damage. The guards also protect against falling branches, storm-blown debris, and any casual contact damage, such as may occur during maintenance activities. Hail guards can also protect ground units from damage by weed-whackers, lawnmower discharge, balls, etc.

While hail guards can offer effective protection against hail and large airborne debris, some guards, especially those with small-gauge openings, may create new problems by restricting airflow, trapping and retaining organic matter such as seeds, especially cottonwood, dust, insects, leaves, thus blocking the required air flow to the condenser coils. To address this concern, air intake filters are available that combine effective hail protection with air filtering technology. These products use materials specifically engineered to promote air flow, thus making them highly suitable for use on high-velocity and high-volume systems. (See Figure 2)

Photo courtesy of Air Solution Company.

If the property is more than 30-years-old, expect the insurance underwriter to ask specific questions about the HVAC system, such as:

- What type of heating system is used in each part of the building? Wall heaters, floor heaters? Or forced hot air, steam or other?

- What type of fuel is used in the heating system? Natural gas, propane, electric, oil?

- When was the heating system or furnace installed? What is its condition? Has it been installed and vented, if appropriate, according to the manufacturer’s specifications?

- Has the heating system been updated in any part of the building? When was this done? Describe what updates were made and note whether the updates were full or partial.

- Have there been any problems or failures of the heating system? If so, describe the problem and how it was addressed.

- How is maintenance of the heating system handled?

- When was the boiler installed? What is its condition? Has it been installed and vented, if appropriate, according to the manufacturer’s specifications?

- What type of fuel is used in the boiler? Natural gas, propane, electric, oil?

- How is maintenance of the boiler system handled?

- What type of air conditioning is used in each part of the building? Central air, window units?

- Has the air conditioning system been updated in any part of the building? When was this done? Describe what updates were made, and whether they were full or partial.

- Have there been any problems or failures of the air conditioning system? If so, describe the problem and how it was addressed.

- How is maintenance of the air conditioning system handled?

Roofing Systems

Roofing should be the easiest of all the critical building systems to manage, correct? It has a multi-year warranty. What’s there to worry about?

Roofing systems are often more complex than they appear, and can conceal a variety of problems. Because roofing systems may be made from a variety of materials, and because they are continuously exposed to the elements, assessing their condition and longevity requires care. Manufacturer’s warranties detail the life expectancy of the roof under normal conditions. Typically, a roof is expected to last about 15 to 30 years, depending on the type. Some roofing products have 30- to 40-year warranties.

If the property is more than 20–years-old, expect the insurance underwriter to ask specific questions about the roofing system, such as:

- What type of roofing system is used in each part of the building? Tile, slate, wood shake, metal panel, built-up, asphalt? Does the roof include failure-prone fiber-cement shakes or shingles?

- When was the roofing system installed? What is its condition?

- Has the roof been updated in any part of the building? When was this done? Describe what updates were made and whether they were full or partial updates.

- Have there been any problems or failures of the roofing system? If so, describe the problem and how it was addressed.

- How is maintenance of the roofing system handled?

The roofing system should be inspected annually once it shows signs of age or damage.

The presence of multiple layers of roofing materials indicates that the roof has been repaired or replaced, in whole or in part, and may be an indication of problems with the building structure. If the building has more than one type of roof system, or uses a variety of materials, or has the same materials installed on different exposures., north vs. south, each must be evaluated separately.

Roof damage may be caused by a number of factors, alone or in combination:

- Aging: All roof components and materials are subject to natural aging and wear and tear.

- Weather: Extreme heat and cold, snow, wind, hail, and ice can damage roofing materials, weaken structural members and accelerate aging.

- Sunlight:Heat and ultraviolet radiation contribute to degradation of membranes, shingles, sealants and other roofing materials. South- and west-facing roofs almost always deteriorate more quickly than those with northern and eastern exposures.

- Moisture: Water from rain, snow, hail, fog, wind-driven moisture, or roof-top vents and machinery can cause deterioration, mold, mildew, algae, moss and related problems.

- Ponding: Melting snow or accumulated rainfall can form ponds on flat roofs, causing damage and leakage. In extreme cases, the accumulated weight of ponded water can collapse the roof.

- Ice Dams: Melting and freezing snow can form ice dams, which can damage the roof and allow water to enter the building.

- Debris: Accumulated debris – storm debris, vegetation, construction materials – can clog drains and damage roof coverings.

- Physical Damage: Displacement, disturbance or erosion of aggregate ballast, such as caused by winds, storms or human traffic, or direct damage to roof coverings, such as caused by hail, ice, wind, nearby trees or human activity, including vandalism or construction projects, can create penetrations or weak areas into which moisture and dirt can penetrate.

- Nearby Trees: Trees provide shade and aesthetic value, but can also cause problems if their shade traps moisture, or if leaves fall on to the roof, or if limbs scrape the roof or fall there during severe weather. (See Figure 3)

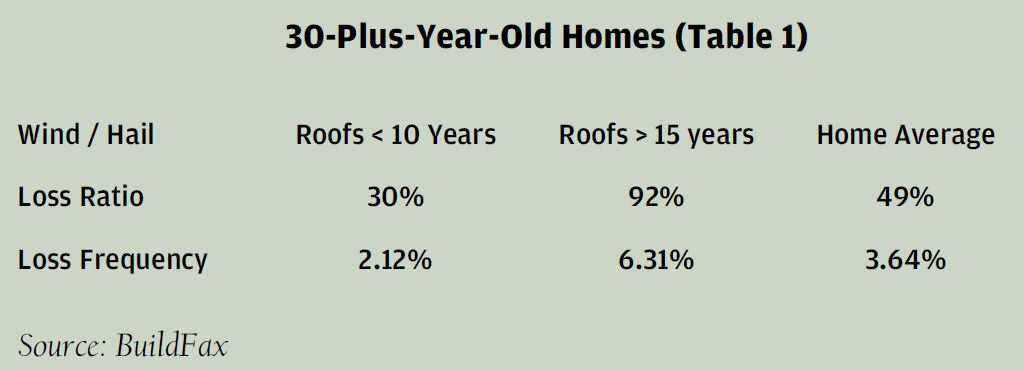

This three-part series has focused on the age of the building as the key driver for maintenance of the structure’s critical building systems. However, when addressing roofing, the main concern is the age of the roof and not the building.

According to BuildFax, an independent company that collects and organizes construction record data, an analysis of roof age information shows compellingly that older buildings with new roofs have more than three times lower loss ratios and loss frequency than older buildings with older roofs. (See Table 1)

Various types of roofing systems are subject to different sorts of damage as they age:

Low-slope roofing systems show their age in damage to roof membranes, such as tears, splits, seam separations, punctures, loose edges, ridges, eroded areas, blistering, and to the ballast which protects it, which can be eroded or displaced by high winds or foot traffic.

Metal panel roofing systems generally age well, though there can be problems with accumulations of moisture under the panels if insulation and ventilation are not appropriate and sufficient. The protective finish must be re-done about every 40 years, or more often in areas where the finish might be worn, as by overhanging trees.

Asphalt (composition) shingles are subject to cracking and rotting. Exterior decay is often a sign of poor attic ventilation. Where moisture is present, growth of mildew, moss, fungus or algae will hasten aging and deterioration.

An accumulation of granules in gutters or on the ground is a sign that the shingles are worn and need replacing.

Wood shakes and shingles can absorb and hold moisture, particularly at their lower edges, where the ends of wood fibers are exposed. Damp shingles and shakes support the growth of moss and lichen, which breaks down the wood and hastens decay. A variety of finishes and preservatives may be applied to wooden shakes and shingles to reduce weathering, retard decay or to achieve desired colors. However, some finishes may increase the combustibility of the wood components and significantly increase the risk of fire. Check state and local building codes for restrictions on the use of wood shakes and shingles, especially in wildfire areas such as California.

Slate and clay tiles, though durable, can be broken by hail, windborne debris, etc.

Fiber-cement roofing products were sold in the 1980s and 1990s with 25- to 50-year warranties promising resistance to fire, insects, fungus, moisture and weathering. Most of these products have been withdrawn from the market because of partial or complete failure due to problems such as swelling, cracking, warping, delamination, crumbling, embrittlement, and breakage. Once damaged, fiber-cement shakes or shingles can no longer protect the building and its contents from rain, snow, sun and other environmental conditions. As the shingles absorb water, the moisture-laden roof often becomes too heavy for the structure, causing sagging and other damage. Remediation may require replacement of the entire roof.

Depending on the size of the building, replacing a roof can cost tens or hundreds of thousands of dollars, an expenditure that must be planned well in advance. Homeowner associations, for example, normally conduct periodic reserve studies to plan for the funding of improvements and repairs. An underfunded reserve may cause the HOA to try to squeeze a few more years out of a roofing system that is in need of replacement, relying on insurance to cover the costs of damages and repairs. However, an insurance policy is not a maintenance policy. For example, if a building or its contents are damaged by water leaking through a roof that has long out-lived it usefulness, the damage may not be covered by insurance.

Whether for air-conditioning units or roofing systems, preventive maintenance, and planned replacement will always be more cost-effective than waiting for a failure and the inevitable damage that results.

While property upgrades often are driven by building codes and insurance requirements, proactive retrofitting can reduce insurance costs during the property’s lifetime. Upgrades to critical building systems should be viewed as long-term investments to protect and increase the value of the building, rather than a short-term means of reducing insurance costs in time for an upcoming renewal. Periodic inspections and maintenance for critical building systems is an extremely effective risk management technique and should be part of every property management program.

By helping the policyholder to understand the “Age of Building” questions, and by assisting with gathering and communicating accurate information to the underwriter, the agent fosters a mutually beneficial relationship between the insurer and the policyholder. By serving as an informed advisor and advocate, the agent can help the policyholder to reduce risk, increase safety, and save money over the long term.

Was this article valuable?

Here are more articles you may enjoy.

Beazley Agrees to Zurich’s Sweetened £8 Billion Takeover Bid

Beazley Agrees to Zurich’s Sweetened £8 Billion Takeover Bid  Nine-Month 2025 Results Show P/C Underwriting Gain Skyrocketed

Nine-Month 2025 Results Show P/C Underwriting Gain Skyrocketed From This Issue