The R Street Institute, a nonprofit public policy research organization headquartered in Washington, D.C., has found that Vermont has the best insurance regulatory environment in the U.S. for the third straight year in its annual Insurance Regulation Report Card.

The fifth annual report, written by R Street Senior Fellow R.J. Lehmann, issues letter grades for all 50 U.S. states based on seven categories – politicization, fiscal efficiency, solvency regulation, auto insurance market, homeowners insurance market, residual markets and underwriting freedom. The two factors most emphasized in the report were solvency regulation and underwriting freedom, because it stated it found these factors most illustrative of states’ ability to create healthy and competitive markets.

For 2016, five Eastern U.S. states improved their grade compared to last year (New York, Pennsylvania, Maine, New Hampshire and Vermont), while six received a lower grade (Massachusetts, New Jersey, Virginia, Connecticut, Maryland and Delaware). One state, Rhode Island, received the same grade both years.

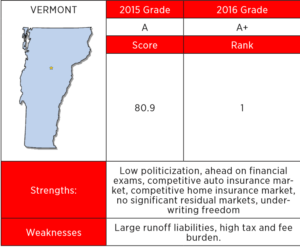

Best in East: Vermont

The report found Vermont had the best insurance regulatory environment in the U.S., receiving the only A+ score and improving from its A grade last year.

“Whether we are serving consumers or working with the industry, we take pride in being accessible and responsive regulators,” Kaj Samsom, deputy commissioner for the insurance division at the Vermont Department of Financial Regulation, told Insurance Journal. “Maintaining the competitiveness of the markets is key for us.

Vermont is a very small market, and we understand that it needs to be an attractive place for insurers to do business, or they simply won’t bother.”

One particular strength the report found in Vermont is its underwriting freedom.

This section of scoring was based on rate-filing system descriptions from the 2015 ISO State Filing Handbook, examining the processes states use to review rates in four property-casualty insurance markets: private auto, homeowners, medical liability and general commercial lines.

The scores ranged from zero points for states that use a prior approval filing system, in which all rates are approved by a regulator, up to five points for states that use “no file” systems, in which the state either does not require rates to be filed or filings are seen as a formality.

In five other Eastern U.S. states – Connecticut, Delaware, Maryland, Massachusetts and New Jersey – a lack of underwriting freedom was found to be a weakness in scoring.

“We experience firsthand that consumer choice and price competition are two of the most important consumer protections when it comes to affordability and service,” Samsom said. “We regularly analyze the personal lines market to ensure that prices are not excessive and that consumers have choice.”

He added that communication and accessibility are also key to this strategy.

“This doesn’t guarantee that there won’t be issues, but when there are, we open a dialogue with the companies and try to get on the same page with how to address the problem,” he said.

One weakness the report outlined for Vermont, however, was its high tax and fee burdens, which factored into the report’s measure of fiscal efficiency for each state.

“My guess is that it is our fines and penalties that drive this metric,” Samsom said. “We make no apologies for that. If you break the law, you may face significant penalties. The penalties go straight to the General Fund, not our budget, to avoid any perverse incentives. If we turn the other cheek or go light on a violation, we are not fostering a level playing field and are actually harming the good players in the industry.”

Samsom acknowledged that while the report’s A+ grade is appreciated by Vermont DFS staff, each market is unique, making it difficult to accurately rank all 50 states.

“Does it mean Vermont is the best regulator? Absolutely not,” he said. “Attempting to rank the performance of a regulator is fraught with problems. Each state’s markets, consumers and issues are so unique that having a standardized scorecard is bound to be problematic.”

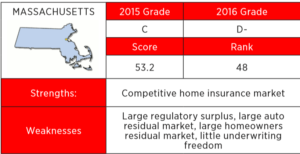

Worst in East: Massachusetts

Chris Goetcheus, director of communications at the Massachusetts Office of Consumer Affairs and Business Regulation, also criticized aspects of the scoring rationale as too one-size-fits-all. Massachusetts received the lowest grade of the Eastern U.S. states with a D-, down from its grade of C last year.

“I think the D- grade is unwarranted,” he said. “There are areas where I think this report is flawed in regard to its evaluation of the Massachusetts Division of Insurance.”

The report pointed to a regulatory surplus of more than eight times the size of the insurance department budget as one weakness for the state.

The regulatory surplus for each state was considered in determining its fiscal efficiency. One issue outlined in the report was that total fees and assessments collected by state insurance departments across all 50 states were more than double the amount spent on insurance regulation in 2016.

“Limiting the consideration just to those regulatory fees and assessments that are paid by insurers and insurance producers, states collected about $1.87 billion more in regulatory fees than they spend on regulation, up from $1.61 billion last year,” the report said.

Goetcheus contested that under Massachusetts law, however, revenue and regulatory spending are divided appropriately.

“The Massachusetts DOI in the 2016 fiscal year generated $88 million in total revenue, and under our law, the majority of

those revenues go to the General Fund,” Goetcheus said. “The legislature annually appropriates the agency funding, which for the 2016 fiscal year was $15.7 million. The remaining $72.3 million went to the General Fund as it is supposed to do.”

The report also found Massachusetts’ large residual markets to be a weakness.

“Where residual markets grow large, it generally represents evidence that regulatory restrictions have prevented insurers from meeting consumers’ needs by disallowing what would otherwise be market-clearing prices,” the report stated.

Based on Automobile Insurance Plans Service Office (AIPSO) data, the report found that three Eastern U.S. states – Maryland, Massachusetts and Rhode Island – have residual markets that account for more than one percent of auto insurance policies. The report measured the size of residual markets for home insurance as well using the most recent available data from the Property Insurance Plans Service Office.

“They were correct that Massachusetts’ auto residual market is less than two percent – it’s hovering around 1.4 percent of the total market share, which is very healthy,” Goetcheus said. “The reason why our residual market for property insurance may be higher than a lot of other states is that Massachusetts’ FAIR plan offers a full homeowners policy portfolio. Some states don’t offer such a broad portfolio, thereby tempering the market share size for those states.”

Indeed, 30 states and the District of Columbia operate Fair Access to Insurance Requirements (FAIR) plans, originally created to serve consumers in areas where it is difficult to obtain homeowners coverage.

One strength the report found in Massachusetts is its ability to regulate insurer solvency.

The report looked at how well states examine the companies they regulate by using the National Association of Insurance Commissioners’ (NAIC) data on the number of financial exams and combined financial/market conduct exams states reported for domestic companies from 2011 through 2015. It compared those figures to the number of domestic companies listed as operating in the state for those five years.

“The number one responsibility of an insurance regulator is to monitor company solvency,” said Goetcheus. “We’re very proud of the job that our financial examination staff does at the Massachusetts Division of Insurance. They do a lot with a little, and we haven’t had an insolvency here since before 2000.”

Ratings Methodology

The report acknowledged that because it is limited to factors it can quantify for all 50 states, there are considerations that it does not reflect.

“Among other variables, we lack good measures of how well states regulate insurance policy forms and the level of competition in local markets for insurance agents and brokers,” the report listed as one example.

R.J. Lehmann told Insurance Journal that The R Street Institute believes there is a role for regulation and tries to outline what it believes that role is in its report.

“We are free market advocates. That is not something we would hide,” he said. “We’re not going to say it’s not ideological, but it’s not anti-government.”

Scores for each state were calculated by adding the weighted results from all seven variables. For each of the categories, data from the most recent available year were used.

“The report has some great metrics and provides good discussion and context about the methodology used, and I think it has the potential to provoke good conversations,” Samsom stated.

East Region Grades

The three Eastern U.S. states receiving A grades are: Maine with an A, New Hampshire with an A- and Vermont with an A+.

The three Eastern U.S. states receiving D grades are: New York with a D+, Massachusetts with a D-, and Delaware with a D.

Six Eastern U.S. states received B and C grades, including Pennsylvania and New Jersey with a B-, Virginia with a B, and Connecticut, Maryland and Rhode Island with a C+.

Lehmann and other fellows at R Street Institute are authors of the Right Street blog on Insurance Journal.com.

IJ West Editor Don Jergler contributed to this report.

Related:

- West Regulation Report Card: California Most Politicized State

- Southeast Regulation Report Card: North Carolina Flunks; Florida, South Carolina Dispute Grades

- South Central Regulation Report Card: Texas’ Grade Rises, Arkansas’ Drops

- Midwest Regulation Report Card: States’ Grades Range from A to D

- State Regulation Report Card: R Street Grades Them All from Best to Worst

Topics USA Trends Legislation Homeowners New Jersey Massachusetts Maryland Connecticut

Was this article valuable?

Here are more articles you may enjoy.

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns  Former Insurance Agent Sentenced to Jail for Fraud, Again

Former Insurance Agent Sentenced to Jail for Fraud, Again  Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal

Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal  FTC Sues Hims & Hers for Sending User Health Info to Meta, Snap

FTC Sues Hims & Hers for Sending User Health Info to Meta, Snap