Greg Hagood didn’t have many details to work with on Thursday afternoon.

Hurricane Irma wasn’t expected to make landfall in South Florida for another 64 hours. Projections for its path were all over the place, especially considering that a centimeter deviation on the map might mean billions of dollars of destruction either averted or heaped onto the tally. So when Hagood phoned his natural-catastrophe bond investors, he had a simple message: Stay calm despite winds strong enough to reduce a house to splinters.

“This is our 20th year in business,” Hagood said. “We’ve lived through other times of stress. It’s not completely foreign to us.”

Hagood’s hedge fund, Nephila Capital Ltd., oversees more than $10 billion, mostly invested in so-called cat bonds, which backstop insurers on claims stemming from natural disasters. Some of that is retirement money from schoolteachers in Pennsylvania and state employees in Alaska and Oregon. They provide protection for Universal Insurance Holdings Inc., the company with the biggest risk in the Florida residential market.

His firm, which he co-created with Frank Majors, has also attracted some of the biggest investors in the world. New York-based KKR & Co., co-headed by billionaire Henry Kravis, has a nearly 25 percent stake. Man Group, the $95.5 billion London-based money manager, owns 19 percent.

Nephila also helps Blackstone Group LP, the world’s largest alternative-asset manager, with part of a $72 billion portfolio run by Tom Hill.

Blackstone declined to comment. KKR didn’t immediately return a message seeking comment.

Nail-Biting Times

These are nail-biting times for insurance companies and the funds that stand behind them. Irma, already responsible for the strongest sustained winds of any recorded Atlantic hurricane, is roaring through the Caribbean in the wake of Hurricane Harvey, which devastated southeast Texas, and in advance of Jose and Katia, storms that could also potentially cause havoc. S&P Global Ratings Inc. has identified 13 cat bonds at risk from damage claims in Florida. Barclays Plc said that insured losses caused by Irma could soar to $130 billion.

Irma has already begun to push down some cat-bond prices. A $125 million Citrus Re Ltd. bond was priced at a 50 percent discount on Thursday.

Brett Houghton, managing principal at Fermat Capital Management, which has most of its $5 billion fund in cat bonds, said he spent most of Thursday avoiding televised forecasts.

“If people just watched the Weather Channel, they’d sell everything,” Houghton said. The round-the-clock coverage is “looking for ways to sound as sensational as possible. We’re trying to look at it from a more cold, detached, calculative perspective.”

Spreading Risk

Cat bonds spread the risk of natural disasters and play an important role by taking on losses that otherwise would be borne by primary insurers. The securities are akin to high-yield debt, but they’re not correlated to credit markets.

“The market for this kind of thing is pretty untested,” said Ryan Tunis, an analyst at Credit Suisse Group AG. “There are questions of how fast they’ll pay out, whether they’ll pay out.”

The cat-bond market is valued at almost $90 billion, and almost half is tied to risks in Florida, where insurers are mostly state-run entities and small regional carriers looking to mitigate risk.

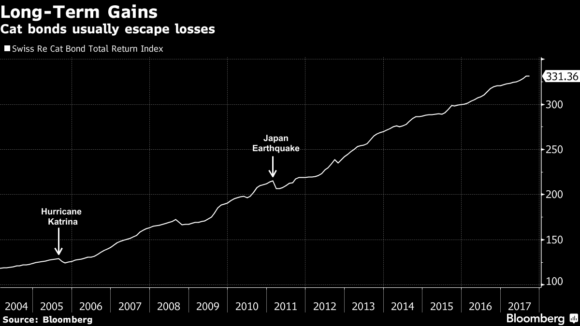

For the most part, the cat bonds have remained resilient. Part of this is due to a lack of major disasters in the biggest U.S. cities, where losses would be large. The Swiss Re Cat Bond Total Return Index has climbed more than 100 percent in the past decade.

The market has drawn in a record amount of cash in the first half of this year, according to insurance broker Aon Plc. Issuance was $11.3 billion, Aon said.

Hedge Funds

For a time, cat bonds provided investors with returns that beat the S&P 500. More recently, the bonds have slipped behind. That’s partly because so many pensions, hedge funds and wealthy individuals have demanded the securities that the price they take to carry the burden has come down.

Michael Millette, the former head of structured finance at Goldman Sachs Group Inc., helped the bank develop a market for cat bonds in 1990. It was one of the first signals that high finance had discovered the reinsurance market. Millette now runs his own fund, with backing from Blackstone, according to Artemis, a trade publication.

The securities began to proliferate in the wake of Hurricane Andrew, a disaster so devastating that the World Meterological Organization discontinued the use of the name after the 1992 hurricane season, according to Swiss Re AG. Significant losses from California’s Northridge earthquake in 1994 and the Kobe temblor in Japan a year later motivated many companies to find reinsurance, or insurance that backs insurance.

More than a dozen hurricanes during the 2005 season, including Katrina, Rita and Wilma, resulted in more than $75 billion of insured losses, causing a dramatic rise in cat-bond issuance, according to the Journal of Alternative Investments.

Not everyone is rushing in. David Havens, an insurance analyst at Imperial Capital LLC, said his company considered wading into the market. Since the firm would be matching buyers and sellers rather than using their balance sheet to invest in the debt, the trading spread was “like a dime,” he said.

“There’s already a preexisting world of clubby guys,” Havens said. “So it’s a hard market to get into.”

Houghton, of Westport, Connecticut-based Fermat, which was founded in 2001, maintained a philosophical coolness Thursday despite contemplating possible Irma-related losses.

“Even if our investors do end up losing a lot of money on this event,” he said, “there will be opportunities to make money in the aftermath.”

Topics Catastrophe Florida Hurricane

Was this article valuable?

Here are more articles you may enjoy.

Tropical Storm Watches Posted Across Florida’s Panhandle Region

Tropical Storm Watches Posted Across Florida’s Panhandle Region  Air Taxi Service Across Parts of Florida Moving Closer to Reality

Air Taxi Service Across Parts of Florida Moving Closer to Reality  Iran Renews Attacks on Gulf States After Another Night of US Strikes

Iran Renews Attacks on Gulf States After Another Night of US Strikes  Allstate’s $1.7M RICO Claims Fraud Suit Merits Trial, Not Arbitration: NJ High Court

Allstate’s $1.7M RICO Claims Fraud Suit Merits Trial, Not Arbitration: NJ High Court