Each reinsurance renewal season sees brokers feverishly chasing down the best premium prices in the market. Frequently, when the panel of reinsurers offer their submissions for a slice of treaty, the broker will discover that the treaty is oversubscribed and will have to go back to the markets to reduce each reinsurer’s commitment by a certain percentage, in a process called signing-down—but the price stays the same.

During this price-discovery process, brokers do their best to get an indicative price of what the market will accept, but “every time a risk is oversubscribed, it means the broker has gotten the price wrong and the ceding company has paid too much; it’s like you’ve left money on the table—perhaps millions of dollars for a single treaty,” according to Sean Bourgeois, founder and chief executive officer of Tremor, the Boston-based technology firm. (See related article: “Reinsurance Pricing Technology That Works During Hard and Soft Markets“)

While insurers and reinsurers know that an oversubscribed program means that it was overpriced, “until recently no one’s been able to show exactly by how much,” he said in an interview with Carrier Management.

Brokers do their best to clear a market price, but it is difficult to calculate because “you need really serious computing power to do that properly,” he added. “Computers can do this a lot better than people because it involves a complex mathematical problem when you have to consider 20 reinsurers that all have different preferences for price and quantity.”

Bourgeois is speaking from a particular point of view because his company, Tremor, has developed an independent marketplace for auctioning reinsurance placements, which in essence provides a procurement placement. He said the platform provides a more efficient way to determine the actual price of risk, providing price discovery and allocation of limits using auction and optimization techniques which enable the insurer to assess price information in real time to find the optimal price that satisfies all its risk preferences at the same time.

Bourgeois believes that Tremor is already creating a structural change within the market, helping ceding companies to get the right price. Since 2019, Tremor has collected more than $4 billion worth of reinsurance quotes. Tremor sits between insurers and reinsurers as a third-party, independent marketplace.

How does the Tremor platform work?

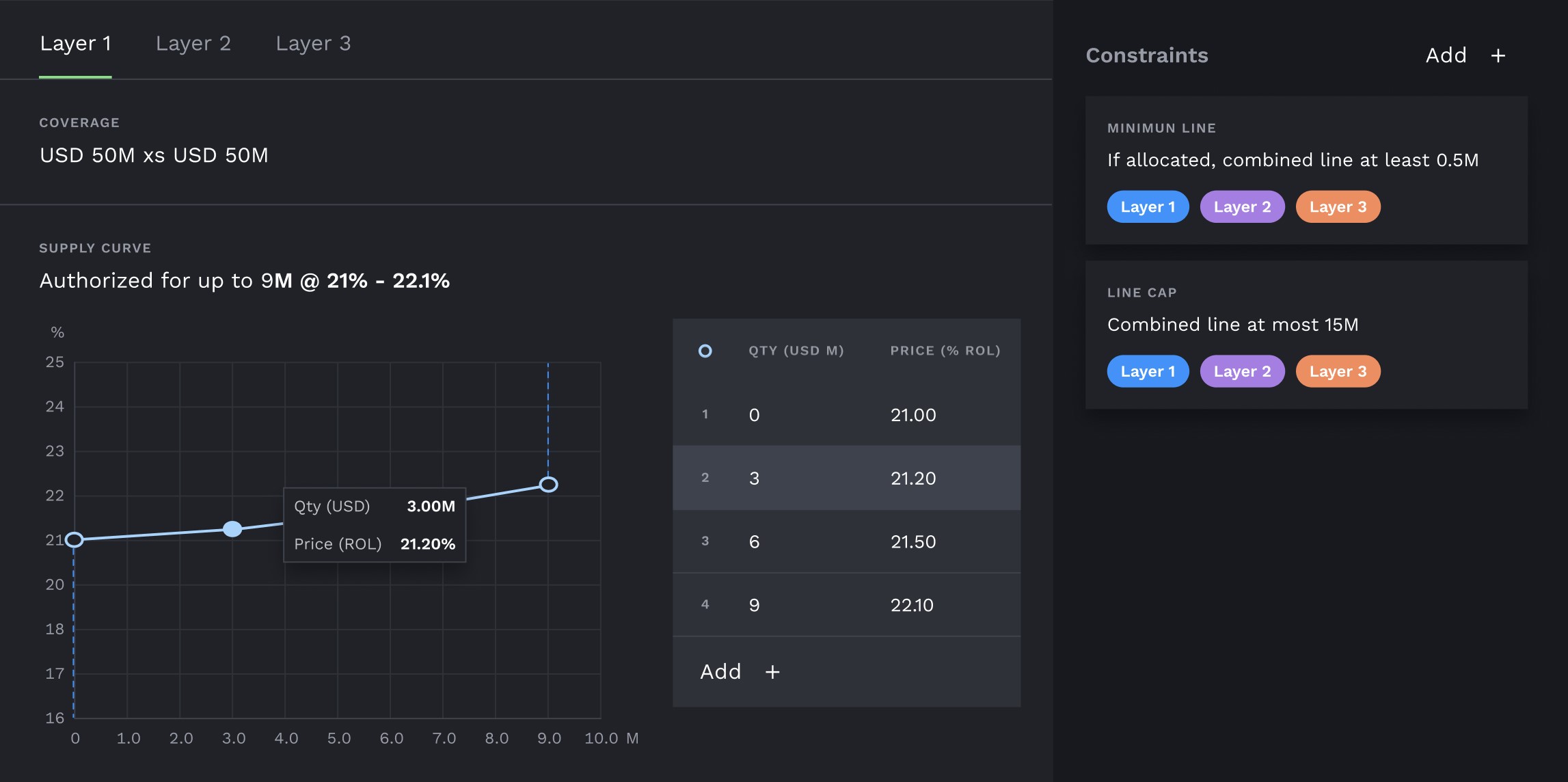

Tremor first collects reinsurers’ authorizations across their price and quantity preferences as well as their “constraints.” For an individual reinsurer, constraints may include setting the maximum amount capacity the reinsurer wants to offer for a single layer and the maximum capacity it will offer across layers (e.g., up to $40 million for the first layer 1 and $40 million on the second layer, but not more than $50 million across both layers). They can also include allocation requirements. (In other words, the reinsurer might specify that it needs at least 10 percent of its allocation to be on the first layer.

Bourgeois described the process as creating “a set of pricing quantity pairs.” For example, a reinsurer may be comfortable giving $10 million of capacity at a 10 percent rate-on-line, but if it could get a 15 percent rate-on-line, it would offer $15 million of capacity.

“The reinsurer is basically building several data points, which we then connect as a supply curve,” Bourgeois said. “We create a supply curve by connecting the price and quantity points the reinsurer enters; they can enter as many points as they would like to.”

Below is an example of what it looks like on the Tremor platform for a reinsurer to enter a supply curve/authorization for a layer of a program:

Each reinsurer has a target portfolio that it is building across dozens of reinsurance treaties. “Tremor allows reinsurers to express exactly how much quantity they want at different prices for the risk profile in question, which should fit perfectly with their portfolio strategy,” Bourgeois went on to say, noting that every reinsurer is likely to have a different strategy for the same quantity of risk.

The reinsurer’s price and quantity preferences along with “subjectivities” (or conditions) are then submitted to Tremor as a blind and sealed quote, which allows them to put forward their best offer without revealing their trading strategy.

All the aggregate bids of the reinsurers’ that participate in the auction—the individual supply curves—are stitched together into a large aggregate supply curve, which slopes upwards from left to right, as a blue “s-curve.” This chart shows quote counts by quantity.

“This ‘heads-up display’ shows the buyers for the first time the real midpoint of the market along with how much capacity was willing to bid under, and over, the market clearing price,” he said. Bourgeois defined market clearing price as the equilibrium price of where the market should trade.

Tremor then automatically renders to the buyer an aggregate supply curve of all the capacity quoting for the program, with best and final prices.

This means if there are 20 reinsurers competing on a placement, “we can show you the full market for your placement and the optimal clearing price in a way that the traditional market simply cannot, for your 20 reinsurers.”

After it sees the full view of the competition for each placement, the insurance company chooses its price and “fill” or limit placed. The insurer decides how much coverage it wants to buy, its demand, subject to its particular constraints, which can include maximum allocations per reinsurer and a preferred subset of reinsurers.

“The perfect clearing price is revealed where aggregate supply intersects their demand. In the above example graphic, the clearing price for $50 million of limit is 22.06 percent rate-on-line, which respects all constraints from the insurers and reinsurers simultaneously,” Bourgeois noted.

“It’s exactly the right amount of capacity needed to clear the amount of limit that the cedent wants and no more. So, there’s no oversubscription, and no sign-downs needed. Supply perfectly meets demand, satisfying the [insurers’ and reinsurers’] constraints every time.”

Bourgeois called this the most competitive capacity because “these are not indications or modeled prices; these curves are actual, bindable best and final offers from reinsurers.”

Quick Auction Process

Although reinsurers are given several days to enter their data, Bourgeois said the process usually takes only minutes, while the auction process and computation only take a few hours.

After the auction, Tremor reports the price selected by the insurer and the quantity purchased and who gets what percentage of each layer.

“Reinsurers receive the precise quantity they asked for at the price they required, whether that price is rate-on-line for a non-proportional placement or ceding commission for a proportional placement, at the perfect market clearing price for everyone, with no oversubscription, sign-downs or follow-on negotiations required,” he said.

The data flows back into the pre-agreed contract, and lines are signed the same day, Bourgeois said. “It’s very, very fast at the end of the process.”

He explained that because the reinsurer authorization process is limited to only a few days and there is no further negotiation on the contract, the entire placement process on Tremor is less than a week.

Pre-Auction Preparation

Before risks are entered on the Tremor platform, the insurance company and its broker design the structure of the placement, such as layers for non-proportional reinsurance. They choose their reinsurer markets and then present the submission with the wording.

In a Tremor placement, contract terms are finalized upfront before the pricing and allocation step, he said. “In the traditional market, however, the price is set first and then the features of the product are often sorted out later. That’s really inefficient and not good for buyers—or necessary.”

Bourgeois emphasized it’s much better to first pin down contract terms, perhaps with one or two options, and then use technology to price and allocate.

“Once we compute the allocations based on the cedent’s desired price and fill, lines can be signed immediately and the contract can be signed.”

![]()

Common Clearing Price; Independent Third Party

Bourgeois believes that Tremor’s platform is unique in its ability to compute a single common clearing price and simultaneously syndicate risk, subject to everyone’s constraints.

He said that some companies call themselves marketplaces, but they offer administrative technology, rather than true marketplace technology. “From our perspective, a marketplace is only a marketplace from a technology perspective if you can find the common price and determine who gets what.”

Tremor is agnostic about the products that trade on the platform. “It doesn’t matter if it’s property or casualty, treaty or facultative, or proportional or non-proportional. As long as you need to have a common price found and syndicated allocation, we can be very helpful.”

Property reinsurance was a natural place for Tremor to start but it also has done some catastrophe bond placements, industry loss warranties (ILWs) as well as some major casualty treaties.

He said Tremor also has started to engage with several large excess and surplus lines carriers and is also working with a large number of captives to help them buy their reinsurance protection.

One of the major attractions of Tremor is that it operates an impartial, third-party marketplace, said Bourgeois.

Similar platforms have been developed and owned by brokers in the past but have failed to take off because they had a conflict in that they represented one side of the market—the reinsurance buyers, he emphasized. “It’s kind of like the fox running the henhouse; brokers are out to get the best deal possible for their buyers.”

As a result, reinsurers don’t want to give a broker-owned auction platform their best and final authorizations and inform the broker of their complete trading strategy, which ultimately would benefit the broker’s client now and in the future, he said. On broker-owned platforms, reinsurers are not likely to provide their best and final authorizations, which would inform the broker of their trading strategy, which “is highly problematic for reinsurers.”

“At the end of the day, a marketplace has to be third-party, independent technology, otherwise it’s just not going to work very well.”

Another problem for brokers that want to develop these platforms is that they have a hard time building acceptance by their own producers. Bourgeois explained that brokers make a good living from the traditional way of placing reinsurance, “profiting from opacity, so they aren’t often motivated to start placing risks on even their own auction platforms.”

Nevertheless, Bourgeois did not believe that Tremor would disintermediate brokers. “Tremor works in cooperation with brokers to optimize outcomes,” he said, explaining that using Tremor doesn’t mean an insurer has to abandon its broker relationships.

Indeed, Tremor has secured agreements with eight major reinsurance brokers, which represent more than 95 percent of reinsurance placements worldwide.

“As a result, if you’re working with a broker, it’s incredibly likely they have an agreement with Tremor and can help you place part or all of your program on the platform.” However, it’s not a requirement for Tremor to have an agreement with a cedent’s broker in order to work with that cedent and place its reinsurance.

He said that insurance company members on Tremor can invite their brokers to have a view of the auction process. “It depends on the buyer and whether they want the broker to be in the Tremor platform; it’s totally up to them. We’re willing to manage it however they would like it.”

Tremor is beginning to push some restructuring in the market, which is healthy, he said, but brokers will remain a very important part of the advisory process for a company that’s looking to purchase reinsurance.

“We, at Tremor, believe that the price and allocation piece should be done with technology. The broker is not directly involved in price discovery or allocation in the Tremor system, as is the case in all modern capital markets,” Bourgeois said. “However, a broker is still very much involved in a programmatic transaction on Tremor because they’re going to advise the ceding company how to structure their program; they’re going to help them build their submission,” he continued.

“They’re probably going to run property-catastrophe models for property business. They’re probably going to help in the selection of the reinsurance panel. They’ll probably handle the premiums. They’ll probably handle claims verification. So there’s still an important role for brokers to play.”

Bourgeois noted that the building of a submission, exposure information and contract wording is completed before an insurer puts its risk on the platform, which is a major part of a broker’s role.

Part of the market structure has to change for efficiencies to be delivered, he affirmed. “And, I think, ultimately that will be good for everyone and ultimately good for brokers who embrace it.”

Bourgeois said he often hears that insurance and reinsurance is special in that it’s an industry based on trading relationships built over many decades—and it is not just about computers and market efficiencies. “Inevitably these comments tend to come from people with limited experience working in industries where this type of trading has evolved and is now common, so the echo chamber has them believing that reinsurance is somehow unique with regards to relationships.” The reality is that every industry is built on relationships, including most of financial services, and this doesn’t change with computers, he continued.

“Buyers still need to choose their counterparties. Relationships still matter. This doesn’t change as dramatically as people seem to think it will.

(Related article: “Reinsurance Pricing Technology That Works During Hard and Soft Markets“)

This article first was published in Insurance Journal’s sister publication, Carrier Management.

Topics Reinsurance

Was this article valuable?

Here are more articles you may enjoy.

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?  eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million

eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million  After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed