It was an eventful first quarter, with the Iran conflict co-mingling with market concerns over the private credit exposures held by both European banks and insurers. Unsurprisingly, debt issuance has been affected, with March and much of April seeing a drought after a reasonably lively start to the year, although the on-off-again nature of peace talks has seen activity pick up.

Insurers don’t appear to have been particularly affected so far both in their underwriting and investment portfolios, and it will be interesting to see what is said in their first half 2026 results. However, based on FY25 results, they have generally delivered healthy profits and maintained solid solvency levels, thereby ticking most analyst boxes.

There’s been some softening in prices witnessed in this year’s renewals (both the January and April renewals), given the benign natural catastrophe experience in 2025 and, so far this year — especially for reinsurers. The softer pricing environment also reflects non-traditional capital flowing into the reinsurance space attracted by uncorrelated returns as seen by the strong demand for products such as catastrophe bonds, whilst private equity has been tapping into the traditional insurance world via M&A, setting up reinsurance sidecars and providing funded and unfunded reinsurance solutions.

This means that traditional insurers and reinsurers are waking up to the need to embrace this new capital but also to protect their turf from new and non-traditional invaders. One way to help manage this risk of profit erosion is with better capital management by substituting expensive equity capital with lower cost solvency eligible debt.

Insurers and reinsurers have historically taken a fairly relaxed approach to managing capital, hoarding equity (known as “unrestricted Tier 1” in solvency parlance, which was around 79% of their eligible solvency capital based on FY24 numbers). Insurers are now becoming more aware of the need to keep shareholders happy by delivering strong returns on equity by growing the numerator and managing the denominator.

Therefore, they either use or lose their excess equity capital via M&A, new business growth (where they can find it) as well as capital returns. As such, solvency is being massaged down closer towards their target levels.

Whilst this has led to rising dividend payouts and share buybacks, FitchSolutions’ CreditSights is observing an increasing propensity by insurers to make their capital stacks more efficient, and to more proactively manage their cost of capital, whilst balancing the expectations of the various stakeholders – be they shareholders, creditors, rating agencies or regulators.

While this article focuses on European insurers and reinsurers, many major insurers globally are traded in the Credit Default Swap (CDS) market, and it is a useful indicator of a company’s credit risk.

Increasing Use of Debt

As such, CreditSights has seen increasing use of debt, and in particular, the issuance of a hybrid debt product known as Restricted Tier 1 (known in the trade as RT1), which combines certain features of debt and equity. RT1s are perpetual in nature, paying coupons and absorbing losses in the event of actual or anticipated regulatory solvency breaches.

Last year saw issuance of around €10.5 billion (US$12.1 billion) equivalent, equating to around 38% of total debt issuance from European insurers that we track. This is just under double that seen in 2024, which equated to around a fifth of total debt issuance. As such the RT1 market is growing and currently stands at around €34 billion ($39.3 billion) equivalent (16% of total debt outstanding for European insurers that we track), with around €3.2 billion ($3.7 billion) issued year to date.

There are various reasons for insurers to issue subordinated and hybrid debt, largely relating to its useful function as regulatory solvency capital, and it is also going to come in handy as the Insurance Recovery and Resolution Directive (IRRD) rolls out across Europe, capturing most insurance companies in its clutches. But it also boils down to relative cost, being generally cheaper to issue compared with new equity, which is more beneficial for their cost of capital. (Due to be implemented in January 2027, the European Union’s IRRD is designed to manage the failure of insurance and reinsurance companies.)

Cost of Equity

Calculating insurers’ cost of equity, however, is no easy task and is open to much interpretation, with the major composites’ estimated cost of equity being somewhere in the range of 8% to 14%, and reinsurers’ cost of equity estimated in the 9% to 14% range, according to Bloomberg.

We also tend to think about the relationship between equity dividend yields and RT1 coupons, as this is an annual recurring cost for insurers, although with the caveat that, in theory at least, insurers have more discretion and flexibility vis-à-vis paying equity dividends compared with RT1 coupons, which tend to be more fixed in nature. Even though insurers do have similar discretion on paying RT1 coupons, we take the view that it is more likely that insurers will opt not to pay a dividend rather than suspend their RT1 coupons.

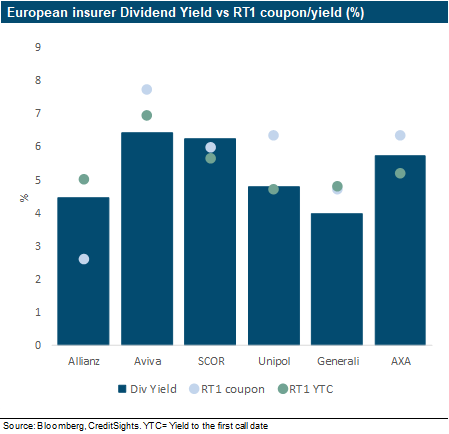

Looking at the sample of 10 insurers and reinsurers that we are using in this article, only six have issued RT1s. These are shown in the chart below, which compares dividend yields with RT1 coupons (green dot) and RT1 yield-to-call (YTC: light blue dot). (See graphic below).

What this shows is that, with the exception of Allianz, RT1 coupons (where we have taken the highest coupon for insurers with more than one RT1 outstanding in euros and British pounds) are around a similar level to, or higher than, dividend yields. So, from an investor’s perspective, they can currently earn a similar or higher annual coupon if they buy the RT1 rather than the equity whilst enjoying more security, as RT1s have a priority claim above equity in distribution and potentially in resolution/liquidation.

However, were we to look at RT1 yields-to-call, which gives an indication of where an insurer or reinsurer may be able to issue a new RT1, we can see that they are around the same level or exceed dividend yields, so from an annual cost argument for the issuer, it is less compelling. But if we consider the cost of equity ranges discussed above, we can see that issuing RT1s would in many cases be cheaper than issuing new equity and therefore beneficial in terms of their cost of capital.

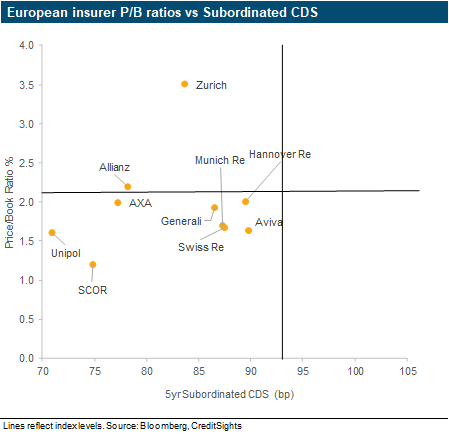

A useful way to look at how European insurers are viewed by equity and credit investors is to compare their price-to-book (P/B) ratios to their 5-year subordinated CDS spreads. The latter acts as a useful proxy given dated subordinated debt (known as Tier 2) is their main source of debt funding, accounting for 61% of current nominal outstanding for the bonds that we track, and for around 15.4% of their eligible solvency capital based on FY24 solvency data.

The chart above plots the P/B ratios for our sample of composites and the four largest reinsurers against their 5-year subordinated CDS spreads. What it shows is that our selection of 10 insurers and reinsurers are trading at P/B ratios in the range of 1.2x to 3.5x, with most trading in a similar ballpark to the SXIP equity index level of 2.1x.

When we look at the x-axis, which plots 5-year subordinated CDS spreads, all of the insurers and reinsurers that we look at in this chart are trading tighter than the Subordinated Financials CDS index level of 93 bp, which is an index consisting of both banks and insurers. What surprises us when looking at this chart is that we would have expected more of the insurers and reinsurers that are in the lower left quadrant to be in the upper left quadrant, where the equity market and credit market appear broadly aligned in their view.

If we look at the outliers, Unipol and SCOR stand out as trading at relatively tight subordinated CDS spreads, yet they have the lowest P/B ratios of our sample, indicating that the credit market has a more favorable view than the equity market. Equally, Zurich Insurance is trading at the highest price/book ratio – probably reflecting its acquisition of Beazley – yet the credit market is less excited, with its subordinated CDS spread trading at around the average for our sample set.

So, whilst traditionally we have tended to look at the equity market for signals as to how capital providers view insurance companies, with the increasing use of debt leverage for capital purposes, it would also make sense to consider how the credit market views insurers and reinsurers.

Additionally, with the outlook expected to remain challenging, insurers are under pressure to use or lose their excess equity, and so we can see insurers increasing their focus on managing their solvency stacks more efficiently given all the competing demands they face. Revenues are slowing, and costs are rising due to artificial intelligence, inflation and competition from both traditional incumbents and new entrants, whilst insurers always face the risk of spikes in claims.

Was this article valuable?

Here are more articles you may enjoy.

Tropical Storm Watches Posted Across Florida’s Panhandle Region

Tropical Storm Watches Posted Across Florida’s Panhandle Region  Air Taxi Service Across Parts of Florida Moving Closer to Reality

Air Taxi Service Across Parts of Florida Moving Closer to Reality  Walmart Removes Four Taylor Farms Salads as Recalls Spread

Walmart Removes Four Taylor Farms Salads as Recalls Spread  Viewpoint: Is Your GL Policy Leaving You Exposed as Digital Risk Shifts?

Viewpoint: Is Your GL Policy Leaving You Exposed as Digital Risk Shifts?