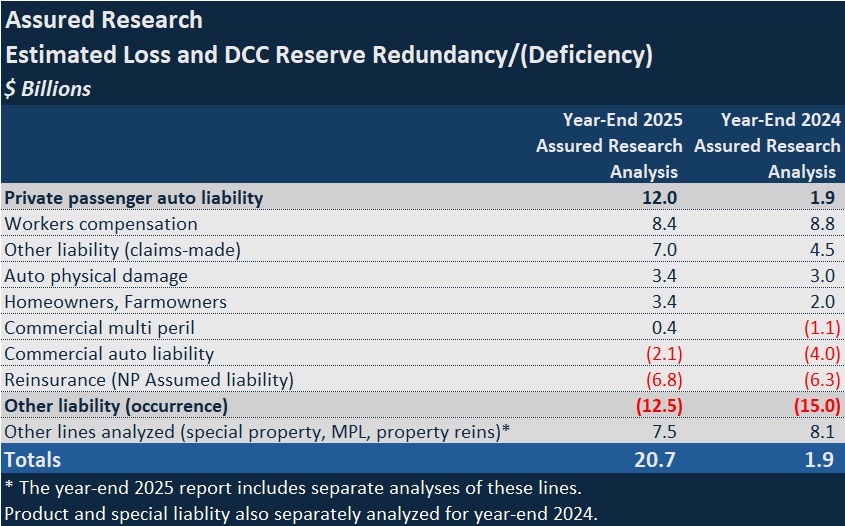

The year-end 2025 carried loss reserve position for the property/casualty insurance industry is more than $20 billion redundant, according to a loss reserve analysis published this week by Assured Research.

In the report titled “P&C Loss Reserves at Year-End 2025: Signs of Improvement…Support for Distinct Pricing Cycles,” Assured Research President William Wilt indicates a big sign of improvement when comparing the overall result of his analysis based on data for year-end 2025 to one he performed a year earlier using year-end 2024 data: The $20.7 billion estimated redundancy as of year-end 2025 is 10-times bigger than the estimated redundancy at year-end 2024, which was just $2.0 billion.

The biggest improvement in reserve position was in the private passenger auto liability line of business.

With the redundancy in year-end personal auto liability reserves now estimated at $12.0 billion, compared to $1.9 billion at year-end 2024, that improvement is signaling an “outright soft market” for personal auto insurance, notes Wilt, who is also a Fellow of the Casualty Actuarial Society.

On the other hand, Wilt gives a more nuanced read of tea leaves on pricing for the other liability (occurrence) line. While still showing the biggest reserve deficiency of any line analyzed by Assured Research, the level of deficiency is lower than the deficiency indicated in a prior reserve analysis last year—$12.5 billion at year-end 2025 vs. 15.0 billion at year-end 2024.

Related: Loss Trends Outpacing Pricing Assumptions: Other Liability Analysis

“The once monolithic pricing cycle is morphing into a series of more distinct, but still correlated market cycles. Our loss reserving work in this Assured Report lends support to the idea that will continue…at least for the near term,” Wilt wrote in the report. “Loss reserving and pricing cycles are interrelated with some lines more sensitive to prior period development (PPD) than others.”

The report includes two types of exhibits for each of the 13 lines of business analyzed. The first page for each line shows comparisons of industry booked losses and Assured Research’s estimates of ultimate loss ratios by accident year (AYs 2012-2025) for the line, along with the estimated redundancy or deficiency for each accident year in dollars. The second displays the dispersion of loss ratios throughout the industry around a median for each line for selected accident years, indicating the direction that most carriers have taken with their reported numbers for recent accident years.

(Editor’s Note: The Assured Research report does not include analysis of accident years prior to 2012.)

For private passenger auto liability, the industry’s ultimate loss ratios of 73.3 and 74.3 as of year-end 2025 for accident years 2024 and 2025 are 1.6 and 3.3 points below those projected by Assured Research.

Wilt noted that there were substantial reserve takedowns on accident years 2022-2024 for private passenger auto liability, and Assured Research is estimating material further redundancies on accident years 2024 and 2025. The analysis shows a $5.0 billion redundancy in accident years 2022-2024—$3.0 billion for 2024 alone—and $6.7 billion for accident year 2025.

Asked to assess the underlying factors behind the favorable developments, Wilt pointed to a combination of factors—”the classic case where rates shot higher in 2022 and 2023, and in 2024-2025 you had claims come down appreciably.” Offering further ideas about the drivers of declining claims, Wilt said he suspects that some of it is attributable to the secular trend of more cars with advanced safety features. “But much of it is from claiming behavior that has inured to the benefit of auto insurers—people being reluctant to file small to modest-sized claims,” he suggested.

Wilt still sees some conservatism in the industry booked loss ratios, which remain well above pre-COVID levels, perhaps indicating an industry view that severity is higher on remaining claims. The actuary estimates a 2025 ultimate loss ratio of 71.0—just about the average of the 2017-2019 pre-COVID accident years, according to a chart in the report.

Some insurers are still booking loss ratios around 80 for the latest accident year, one graph in the report shows. “If our ULR [ultimate loss ratio] estimates are right, downward loss development will feed into pricing algorithms during 2026 and make rate decreases increasingly likely,” Wilt wrote, referring to the lower Assured Research estimates.

“All that favorable development on accident years 2022 through 2024, and I also expect 2025, has to roll through rate filings in the form of lower loss ratios that get baked into pricing algorithms,” he said.

For auto physical damage, loss ratio projections also point to softening rates. “Did you notice on auto physical damage that the ULR for AY25 is down near COVID-level lows,” Wilt wrote in an email explaining his pricing predictions. In fact, the report shows a booked loss ratio of 55.7 for auto physical damage for accident year 2025—just slightly above the lowest booked loss ratio for any prior accident year—compared to 55.2 in 2020.

“Rates will go lower in 2026. Results are too good and affordability matters too much,” Wilt wrote in the report. “Separately, as competition among carriers heats up, we expect the claiming behavior tailwind to shift into a headwind,” he added.

As for the line with the biggest indicated deficiency, other liability-occurrence, while most of the deficiency is concentrated in the 2021-2024 accident years—$10.5 billion of the overall estimated $12.5 billion is from those years—Assured Research is projecting a much smaller deficiency for accident year 2025 ($200 million for AY 2025 vs $1.7 billion for AY 2024 and $3.5 billion for AY 2023).

Across carriers, accident year 2025 ultimate loss ratios are generally more conservative than the ultimate loss ratios for accident years 2021-2024, Wilt notes.

Still, Wilt sees enough of a reserve shortfall in all the recent accident years to prevent outright softening—instead supporting a “gradual recalibration of pricing.” In his view, rates are likely “to remain elevated as adverse PPD comes through on AYs 21-23. But assuming less comes through on AYs 24-25, it seems less likely…that rates move higher than loss trend,” he said.

Separately, Tim Zawacki, principal research analyst at S&P GMI offered a similar view about the other liability (occurrence) line.

“Our view is that pricing in a broad sense does need to go higher—and is going substantially higher in certain coverages like personal umbrella/excess— but it will struggle to catch up to loss costs in certain coverages given both the impact of competitive pressures on the magnitude of price increases and the role social inflation is playing in some jurisdictions,”

When adverse development clusters in recent accident years, it signals that loss trends are outrunning pricing, Zawacki and two co-authors wrote in a recent S&P GMI report, “Other liability (occurrence) trouble shifts to recent years in 2025.”

In the Assured Research report, Wilt offers pricing forecasts that tie into the estimates of loss reserve positions for several lines in the report. The headings on the sections devoted to each line—”too good” for private passenger auto, “also too good” for property, “still good” for workers compensation and “less bad” for commercial auto—give a shortcut read on his indications.

For workers comp, for example, Assured Research still estimates there are material reserve redundancies. But rising accident years loss ratios and turbulent labor and health care markets offer a mixed picture, pointing to a mix of small positive and negative rate changes.

Featured image: AI-generated image (ChatGPT). Not the actual Assured Research analyst

Topics Profit Loss Property Casualty Market

Was this article valuable?

Here are more articles you may enjoy.

As Parasite Spawned Chaos, Taylor Farms Slow-Walked Response

As Parasite Spawned Chaos, Taylor Farms Slow-Walked Response  Two Years in, Ortiz Steps Down as CEO of Florida Re

Two Years in, Ortiz Steps Down as CEO of Florida Re  NYC Says Source of Legionnaires’ Disease Has Been Eliminated

NYC Says Source of Legionnaires’ Disease Has Been Eliminated