While there still seems to be a big discrepancy between the two, is it possible one major reason there’s a difference is because the article you linked talks about auto and home losses, while the report on this site only discusses home losses?

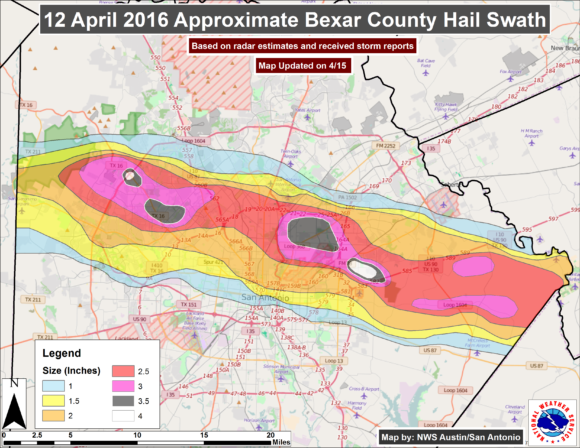

We utilize Core Logic for their hail swath data (although we consume it in a different GIS program) and we’ve found it to be quite helpful and accurate. For what it’s worth, I am not affiliated with Core Logic in any capacity.

Aren’t the insurer’s actuaries aware of the cat. exposure in Texas?

Prudent underwriting would suggest that if rate adequacy is not in place, then the risks should be declined.

Boonedoggle- The hail size and the scope of this storm is unprecedented in San Antonio, plus 40-50% of dwellings have been built in the last 20- 25 years, so ordinarily they’re good risks.

Interesting. These numbers are much different than a recent report put out by the ICT. http://www.insurancecouncil.org/docs/public/news/2016/June022016.pdf

They have total losses at 2 Billion for these combined storms.

While there still seems to be a big discrepancy between the two, is it possible one major reason there’s a difference is because the article you linked talks about auto and home losses, while the report on this site only discusses home losses?

So the home losses are 700 million and the auto losses are 1.3 billion? Doesn’t make sense.

We utilize Core Logic for their hail swath data (although we consume it in a different GIS program) and we’ve found it to be quite helpful and accurate. For what it’s worth, I am not affiliated with Core Logic in any capacity.

Aren’t the insurer’s actuaries aware of the cat. exposure in Texas?

Prudent underwriting would suggest that if rate adequacy is not in place, then the risks should be declined.

Boonedoggle- The hail size and the scope of this storm is unprecedented in San Antonio, plus 40-50% of dwellings have been built in the last 20- 25 years, so ordinarily they’re good risks.