Florida lawmakers late last week gave final approval to a long-debated condominium bill, one designed to give condo owners a little relief on the high cost of bringing structures up to code.

But the final version of the bill seems to have divided the condo insurance community. Some in the industry now worry that House Bill 913 went too far and may have inadvertently given owners options that could thwart spending on repairs or allow buildings to be undervalued and underinsured.

“It has to be a mistake. It’s the exact opposite of what was intended, it seems to me,” said Phil Masi, agency president of AssuredPartners, one of the largest writers of condo insurance in Florida.

The bill is the latest development to come out of the 2021 Surfside condo collapse that killed 98 people. In 2022, Florida lawmakers put strict new rules on condo associations, mandating regular inspections and upgrades, adequate reserve funding to pay for repairs, as well as limits on condo owners’ ability to veto needed spending.

But after an outcry from owners and associations that the cost of improving condo buildings was proving to be too much, too soon for some owners — and as some insurance carriers backed away from condos and premiums rose, the Legislature this year hashed out a number of changes.

HB 913, if signed into law by Gov. Ron DeSantis, will allow certain condo associations to fund their reserves through a loan or line of credit, will give residents greater flexibility to pause payments to their reserves while they prioritize needed repairs, extends the deadline by which associations have to complete structural integrity studies, and exempts some smaller buildings from having to do those analyses.

“We have strived to reach that delicate balance between the safety of our constituents that live in condominiums, as well as understanding the incredible financial impact that sometimes these particular bills that we pass have,” bill sponsor state Rep. Vicki Lopez, a Miami Republican, said, according to the Associated Press.

But Masi and others argue that some things were overlooked in the rush to complete the bill in the final days of the 2025 legislative session, and lawmakers may have to return to Tallahassee later this year to make revisions.

For starters, video conferencing: An earlier version of the bill would have limited condo video conference meetings to no more than twice a year. That language was removed in the final draft but the bill would still require that a quorum of board members be physically present at a meeting site.

“If the annual meeting of the unit owners is conducted via video conference, a quorum of the members of the board of administration must be physically present at the physical location where unit owners can attend the meeting,” the final, amended bill reads.

That could make it difficult or impossible to hold some board meetings, which could have the effect of postponing needed repairs, said Matt Mercier, national practice leader for CBIZ Insurance Services, which represents condo associations around the state. Many board members live out of state part of the year, making it tough for them to attend all meetings in person.

“And if another pandemic hits, some people are going to be stuck out of state and can’t attend in person,” Mercier said.

Also, the final legislation removed the word “must” in key sections, giving condo associations options that could prove problematic, the brokers said.

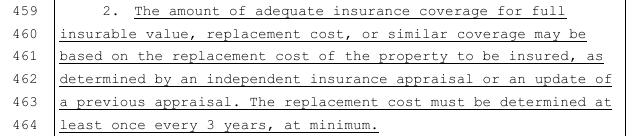

On pages 16 and 17, for example, the bill requires that “every condominium association shall have adequate property insurance as determined under this paragraph.”

But the next sentence appears to upset the long-standing method for determining adequate insurance. The bill struck the wording that previously said replacement cost MUST be determined by an independent appraiser. The new wording notes that the replacement cost MAY be determined by an appraisal or by an update to a previous appraisal.

Does that mean either an appraisal or an update is acceptable under the law? Or does it mean the condo group may choose another valuation method altogether? Mercier and Masi argued it means the latter. That’s an issue because the appraisal process has been used for years and has proven to be a tried-and-true method.

“It was a great law on that. There was nothing wrong with that,” Mercier said.

Using other methods of determining cost may open a can of worms, encourage bad actors, and introduce significant disagreements on the amount of insurance coverage needed, they said.

“Not sure who would argue for amending this language. I think it was just a mistake,” Masi added. “There is no upside to it and plenty of problems that can come with making this optional.”

But others said the concerns are overblown. Mike Clarkson, managing director of Hilb Group of Florida, the insurance brokerage for some 1,200 condo associations, said the new language continues to require either an appraisal or an update to a previous appraisal.

“You would still have to get an appraisal,” Clarkson said.

But it may not matter, anyway, he said. Insurance carriers that write condos already require an appraisal. On top of that, they usually won’t accept a value on a concrete structure of less than $170 per square foot, regardless of what an appraiser says.

Related: Clearwater Condo Building Evacuated After Support Beam Cracks

The next paragraph in the final bill version gives a loss-limit option and has raised its own concerns. The section notes that insurance requirements “MAY be satisfied” by obtaining enough to cover the probable maximum loss in a 250-year windstorm event. The probable loss would be determined through an accepted hurricane loss projection model.

That could mean that buildings could still be greatly underinsured, Masi argued. Condo leaders may think they’ll be getting lower premiums with the lower coverage level, but they won’t save much because most of the premiums are largely based on the first several million in value.

The final bill should have required the insured value on the structures to be based on an appraisal, then could have let condos purchase a lower limit – but only if the 250-year model allows for it. Drafters of the legislation may have worried that the original “must” wording would have required insuring everything to the appraised value limits, Masi suggested.

“But there were other ways to amend that language and certainly they didn’t need to mess with the appraisal option, which virtually everyone uses,” he said.

State Sen. Jennifer Bradley shepherded the condo bill throughout the 60-day session. She and her staff could not be reached for comment on final version of the bill. But Travis Moore, a lobbyist and consultant who represents condo associations and who worked on the bill this year, said the language is not a mistake. The bill provides a balanced approach and options for struggling condo owners and associations.

“We want them to have enough insurance, but not too much,” Moore noted.

Besides, the Florida Office of Insurance Regulation is unlikely to approve policies that allow loss limits without covering the full value of the condo building. OIR is expected to provide some clarity on that in coming days, he said.

Top photo: The rubble of Champlain Towers South in 2021 (Amy Beth Bennett /South Florida Sun-Sentinel via AP)

Topics Florida

Was this article valuable?

Here are more articles you may enjoy.

Husband and Wife Insurance Brokers Sentenced for Fraud Scheme

Husband and Wife Insurance Brokers Sentenced for Fraud Scheme  eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million

eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million  Florida’s Share of Claims Lawsuits Now About Half of 2020 Numbers, Data Show

Florida’s Share of Claims Lawsuits Now About Half of 2020 Numbers, Data Show  Florida Appeals Court Strikes Jury’s $335,000 Award in Universal Plumbing Claim

Florida Appeals Court Strikes Jury’s $335,000 Award in Universal Plumbing Claim