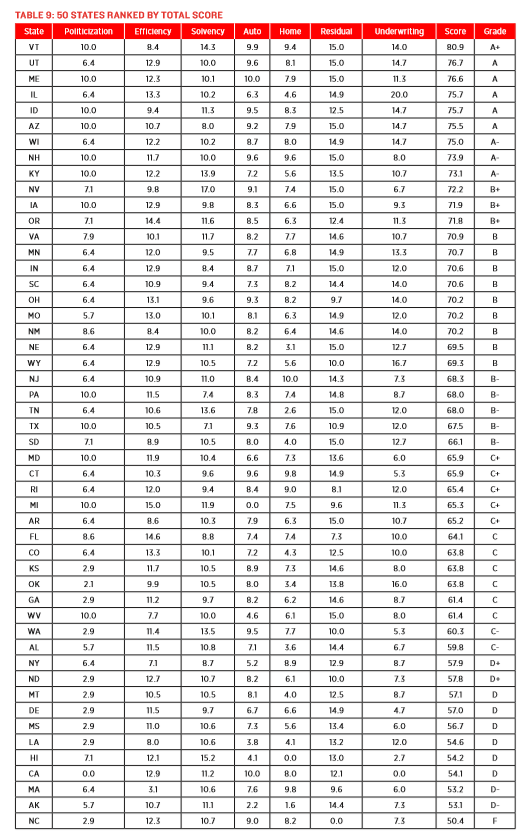

For the second year in a row, Vermont has been graded at the top of the class as having the best insurance regulatory system, while North Carolina has again been graded as having the worst, according to the fifth edition of R Street Institute’s Insurance Regulation Report Card.

Written by R Street Senior Fellow R.J. Lehmann, the annual report grades each state on how “effectively and efficiently they discharge their duties to monitor insurer solvency and to foster consumer choice and competitive, private insurance markets,” according to the Washington, D.C.-based free market think tank.

“We believe states should regulate only those market activities where government is best-positioned to act; that they should do so competently and with measurable results; and that their activities should lay the minimum possible financial burden on policyholders, companies and, ultimately, taxpayers,” Lehmann writes.

For the third straight year, Vermont had the best insurance regulatory environment in the country, receiving the only A+ score. Other states receiving either an A or A- were Arizona, Idaho, Illinois, Kentucky, Maine, New Hampshire, Utah and Wisconsin.

Meanwhile, for the second straight year, North Carolina had the worst score, receiving a F failing grade for the third year in a row. States in the D range include Alaska, Massachusetts, California, Hawaii, Louisiana, Mississippi, Delaware, Montana, North Dakota and New York.

Among the most significant shifts Lehmann noted in the report is the continued expansion of North Carolina’s two property insurance residual market entities, even as Florida’s Citizens Property Insurance Corp.—previously the nation’s largest residual market entity—continues to shrink.

“Not coincidentally, when R Street issued its first regulation report card in 2012, Florida ranked dead last and North Carolina was somewhere in the middle. This year, North Carolina is dead last and Florida is somewhere in the middle,” Lehmann wrote.

Report Methodology

R Street tracks 10 broad categories that it believes measure how well states: “avoid excess politicization; monitor insurer solvency; police fraud; respond to consumer complaints; how efficiently they spend the insurance taxes and fees they collect; how competitive their home, auto and workers’ comp insurance markets are; and the degree to which they permit insurers to adjust rates and employ rating criteria as they see fit.”

The 10 categories are weighted as follows to come up with a final grade:

- Politicization 10%

- Solvency 10%

- Consumer Protection 5%

- Anti-Fraud Resources 5%

- Fiscal Efficiency 10%

- Auto Insurance Market 15%

- Home Insurance Market 15%

- Workers’ Compensation Market 10%

- Rate Regulation 10%

- Underwriting Freedom 10%

The report is largely focused on regulation of property/casualty insurance and particularly on those lines of business Re Street says “have the most direct impact on regular people’s lives,” namely homeowners, auto and workers’ compensation.

The report notes that these lines of insurance also tend to be the most closely regulated.

While the report is critical of some states, it says that “on balance,” states do a good job of encouraging competition and monitoring solvency.

“As a whole and in most individual states, U.S. personal lines and workers’ compensation markets are not overly concentrated. Insolvencies are relatively rare and, through the run-off process and guaranty fund protections enacted in nearly every state, quite manageable,” the author says.

However, Lehmann continues writing in the report, state-by-state regulation leads to inefficiencies and policies that have the effect of “discouraging capital formation, stifling competition and concentrating risk. Central among these are rate controls.”

Lehmann cautions that the report is not intended as a referendum on specific regulators. “Scoring an F does not mean that a state’s insurance commissioner is inadequate, nor is scoring an A+ an endorsement of those who run the insurance department,” he says.

Lehmann is senior fellow, editor-in-chief and co-founder of the R Street Institute. He is the author of numerous policy papers, including the 2012 to 2015 editions of R Street’s Insurance Regulation Report Card.

Lehmann and other fellows at R Street Institute are authors of the Right Street blog on Insurance Journal.com.

For a deeper dive into how R Street rated states in each region, and what some of the state insurance commissioners in each region think about their state’s grade, check out the following Insurance Journal reports:

- West Regulation Report Card: California Most Politicized State

- Southeast Regulation Report Card: North Carolina Flunks; Florida, South Carolina Dispute Grades

- East Regulation Report Card: Vermont Ranks Best for 3rd Straight Year

- South Central Regulation Report Card: Texas’ Grade Rises, Arkansas’ Drops

- Midwest Regulation Report Card: States’ Grades Range from A to D

Topics Legislation Florida Workers' Compensation North Carolina

Was this article valuable?

Here are more articles you may enjoy.

Insurance Broker Stocks Sink as AI App Sparks Disruption Fears

Insurance Broker Stocks Sink as AI App Sparks Disruption Fears  CFC Owners Said to Tap Banks for Sale, IPO of £5 Billion Insurer

CFC Owners Said to Tap Banks for Sale, IPO of £5 Billion Insurer  US Supreme Court Rejects Trump’s Global Tariffs

US Supreme Court Rejects Trump’s Global Tariffs  Carmakers Push Toward ‘Eyes-Off’ Driving, Raising Questions of Safety, Liability

Carmakers Push Toward ‘Eyes-Off’ Driving, Raising Questions of Safety, Liability