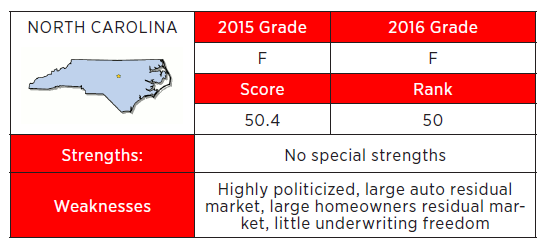

North Carolina ranks the worst of all 50 states when it comes to insurance regulation, according to a 2016 insurance regulation report card by an insurance industry think tank.

The R Street Institute’s 2016 Insurance Regulation Report Card scores state insurance regulatory environments in seven different categories: politicization; fiscal efficiency; solvency regulation; auto insurance market, homeowners insurance market, residual markets and underwriting freedom.

Based on these ratings, each state is given a letter grade. Overall, Vermont received the highest grade of all states with an A+ and North Carolina came in last with a grade of F.

Other states, including Florida and South Carolina, fared better but their regulators still dispute some of R Street’s claims in its report and say some are based on inaccurate information.

The author of the fifth annual report, R.J. Lehmann, writes that states have for the most part done an effective job of encouraging competition and, at least since the broad adoption of risk-based capital requirements, of ensuring solvency. The report also says that, for the most part, U.S. personal lines markets are “not overly concentrated, insolvencies are relatively rare and, through the runoff process and guaranty fund protections enacted in nearly every state, generally quite manageable.”

But the report contends that state-by-state regulations does lead to inefficiencies and particular state policies that have discouraged capital formation, stifled competition and concentrated risk.

R Street bills itself as a think tank dedicated to free markets. The institute believes that “an open and free insurance market maximizes the effectiveness of competition and best serves consumers.” The report, which focuses on personal lines, grades states’ regulatory systems against principles of “limited, effective and efficient” government.

R Street said it believes there is a role for insurance regulation, particularly in the area of insurer solvency, but Lehmann told Insurance Journal that the group is ultimately a free market advocate.

Lehmann says the point of the report is not to be anti-government but to outline what the role of state insurance regulation is.

“The largest single factor in our report is solvency regulation,” Lehmann said.

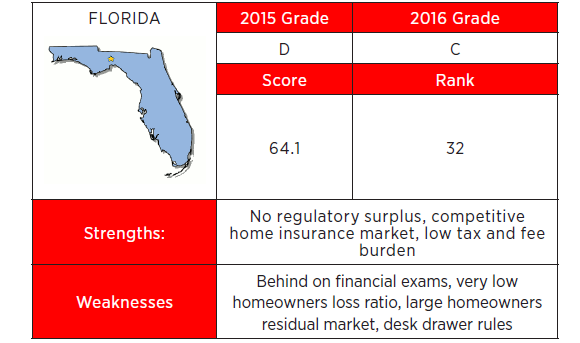

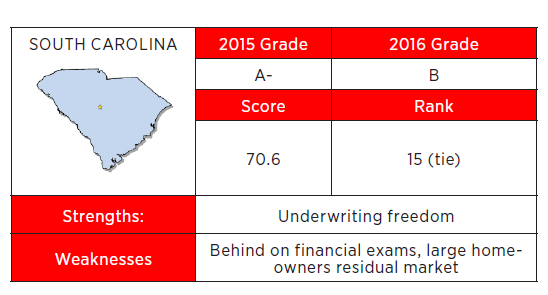

For the Southeast, the states ranked as following: Kentucky –A-; South Carolina – B; Tennessee – B-; Georgia – C; W. Virginia – C; Alabama – C-; Florida – C; Mississippi – D; and North Carolina – F.

Each state was graded on its strength and weaknesses in the aforementioned categories.

North Carolina Issues

According to R Street, North Carolina had “no special strengths” and its weaknesses included being highly politicized, having a large auto residual market and a large homeowners residual market, as well as little underwriting freedom.

The report says that North Carolina’s Beach Plan and FAIR plan have increased significantly in just a few years. In 2011, the Beach Plan wrote 3.37 percent of the state’s market and the FAIR Plan wrote 0.62 percent. In 2015, the North Carolina FAIR Plan was up to 2.16 percent and the North Carolina Beach Plan was up to 7.03 percent.

North Carolina was also dinged for having an elected insurance commissioner.

Lehmann said elected commissioners, as well as those appointed by a governor, can get caught up in playing politics instead of regulating the industry.

“Among non-elected commissioners, in states where you serve a set term that can overlap multiple (gubernatorial) administrations, that seems like the independence that is the best,” he said, adding that this means a commissioner isn’t serving “at the pleasure of one executive.”

The state also suffered a downgrade because of the central role the North Carolina Rate Bureau plays in the personal lines market. The report calls the state an “outlier” because of its large residual auto market – saying that 30 percent of the state’s auto market is in the North Carolina Reinsurance Facility.

“North Carolina had the worst score for the second year in a row and received a failing grade for the third year in a row,” the report states.

The North Carolina Department of Insurance (NCDOI) did not respond to requests for comment by Insurance Journal on the report or its failing grade of the state. Insurance Commissioner-Elect Mike Causey has stated that reforming the North Carolina Rate Bureau will be one of his tasks when he takes over next month from the incumbent he defeated, Wayne Goodwin.

In a statement to Insurance Journal, Causey said that while he is not in total agreement on the methodology used in this report, he does agree that in some areas North Carolina is over-regulated and this over-regulation hurts consumers by limiting competition.

However, he said, contrary to the report’s methodology, allowing voters to vote for an insurance commissioner is actually less political than having a governor appoint one of his top campaign donors or political friends.

“A board or commission is also made up of political appointees, so a free and fair election is the one way voters can directly choose their own insurance regulator,” Causey said. “As commissioner I will work to make North Carolina more competitive in the insurance business and give consumers more choices.”

Florida Takes Issue

Florida moved up from last year’s grade of D to a C this year, but the Florida Office of Insurance Regulation (OIR) took little solace from the upgrade by R Street. The report lists Florida’s strengths as having no regulatory surplus, a competitive home insurance market and a low tax and fee burden.

However, Florida’s OIR took issue with R Street’s “weaknesses” of being behind on financial exams; a very low homeowners loss ratio – an indication of high rates, according to Lehmann; and the state’s utilization of “desk drawer rules.”

Lehmann described “desk drawer rules” as rules of thumb that regulators apply that are not on the books.

“If you know that there’s a certain kind of requirement that would always be denied, even if there’s no rule that it should be denied, we consider that a desk drawer rule,” Lehmann said. “If you try to obey the law as written, you still could be denied any number of business requests.”

Florida’s OIR Communications Director Amy Bogner said they disagree with the report’s assessment.

“We are current with exams. Our residual market has dramatically reduced in recent years, and a low homeowners loss ratio indicates that Florida’s property insurers have the opportunity to earn a reasonable profit. We do not know what “desk drawer rules” are being referenced, but in Florida we enforce statutes and promulgated rules,” Bogner told Insurance Journal.

South Carolina Disputes

South Carolina Insurance Director Raymond Farmer also took issue with R Street’s charge that his state is behind on its financial exams, which was cited in the report as a weakness. Farmer said staying on top of the state’s exam responsibilities is a task he takes very seriously.

“This year was our year to have NAIC Accreditation review and we sailed right through that and if we were behind on anybody’s exam they would have pointed that out,” Farmer said. “Whoever did the report is certainly ill-informed and didn’t do their homework.”

The report also lists the state’s supposedly large homeowners residual market as a weakness and a reason South Carolina’s grade fell from an A- in 2015 to a B in 2016, but Farmer said that information is also inaccurate.

“We have a very competitive homeowners market – the state windpool is actually losing business,” Farmer said. “We have added over 60 companies to our homeowners marketplace in the last 4 years. We think we have a great insurance environment here in South Carolina and think we are as free a market as anyone can be and are always looking to increase competition.”

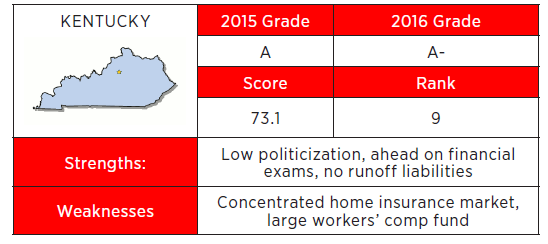

Kentucky’s Grade

Kentucky was the only state to earn a grade higher than B in the Southeast, but it dropped from an A grade in 2015 to an A- this year, ranking no. 9 of all 50 states. The strengths for the state were listed as low politicization, being ahead on financial exams, and no run off liabilities. Its weaknesses were listed as a concentrated home insurance market, and a large workers’ comp fund.

The report gave credence to the state’s “political independence” structure for appointing its insurance regulator – in Kentucky it is done by the governor. The report says this structure offers the greatest political independence for the regulator.

The Kentucky Department of Insurance said it had not viewed the report when contacted by Insurance Journal, but it said it planned to review it.

Lehmann and other fellows at R Street Institute are authors of the Right Street blog on InsuranceJournal.com.

IJ West Editor Don Jergler contributed to this report.

Related:

- West Regulation Report Card: California Most Politicized State

- East Regulation Report Card: Vermont Ranks Best for 3rd Straight Year

- South Central Regulation Report Card: Texas’ Grade Rises, Arkansas’ Drops

- Midwest Regulation Report Card: States’ Grades Range from A to D

- State Regulation Report Card: R Street Grades Them All from Best to Worst

Topics Legislation Florida Agribusiness North Carolina Homeowners Market South Carolina Kentucky

Was this article valuable?

Here are more articles you may enjoy.

Insurance Broker Stocks Sink as AI App Sparks Disruption Fears

Insurance Broker Stocks Sink as AI App Sparks Disruption Fears  Viewpoint: Runoff Specialists Have Evolved Into Key Strategic Partners for Insurers

Viewpoint: Runoff Specialists Have Evolved Into Key Strategic Partners for Insurers  AI Claim Assistant Now Taking Auto Damage Claims Calls at Travelers

AI Claim Assistant Now Taking Auto Damage Claims Calls at Travelers  Judge Tosses Buffalo Wild Wings Lawsuit That Has ‘No Meat on Its Bones’

Judge Tosses Buffalo Wild Wings Lawsuit That Has ‘No Meat on Its Bones’