A California broker is promising to bring a “first-of-its-kind financial resource” that pays homeowners after an earthquake for a low monthly premium whether there’s damage to the home or not.

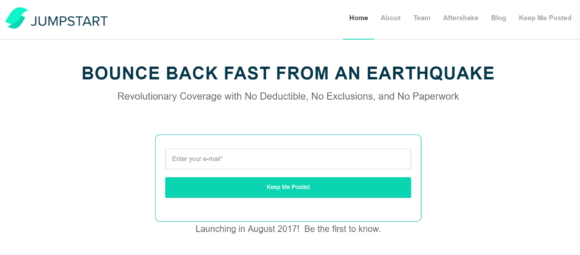

A Berkeley, Calif.-based firm called Jumpstart Insurance Solutions Inc. recently made known its plans to launch the new product in late August on its website.

The Jumpstart site touts that the coming product provides “Revolutionary Coverage with No Deductible, No Exclusions, and No Paperwork.” It also has a disclaimer that the product does not yet exist.

Under what appears to be a parametric product, which does not indemnify the pure loss but makes a payment upon the occurrence of a triggering event, policyholders pay a monthly amount and are promised they will get paid a set amount automatically if there is an earthquake in their area, even if they do not suffer damage. The payment would be enough to help pay for minor repairs but not be sufficient for a major loss or rebuild.

A spokesperson declined to discuss the firm, its product or what the premium or payout would be prior the launch.

About Jumpstart

Jumpstart is registered with the California Secretary of State as a benefits corporation. According to the articles of incorporation filed on Nov. 4, 2015, the purpose of this particular benefits corporation is “to generate a general public benefit including, but not limited to, the specific public benefit of increasing economic stimulus after a natural disaster.”

Jumpstart is licensed with the California Department of Insurance as a property insurance broker-agent, casualty broker-agent and surplus lines broker. All licenses were issued in 2016 and are still active.

Nancy Kincaid, a CDI spokeswoman, couldn’t offer much detail on the broker or the product the firm may be offering.

“They are properly licensed as a surplus lines broker, but we don’t have any products filed from them with the Department of Insurance,” Kincaid said.

According to the Surplus Lines Association of California, Jumpstart received its license on Dec. 7, 2016, but it has not yet submitted any filings to the SLA.

Jumpstart and Recoup

Jumpstart is headed by Kate Stillwell, who is the founder and CEO. Stillwell is a former structural engineer and earthquake risk consultant. From 2010 to 2012, she was an earthquake products manager for EQECAT Inc., a catastrophe risk modeling firm acquired by California-based data and analytics firm Corelogic in late 2013.

Another co-founder and advisor on the team is Alan Hampton, who is also the founder and CEO of Recoup Financial, a catastrophe emergency funds startup, which was reportedly acquired by Jumpstart. The Recoup Financial website is currently previewing a product similar to what Jumpstart is promising that gives “cash the day after an earthquake.” Consumers can choose from $1,000 up to $30,000 in coverage as well as select the quake intensity at which they want the funds paid — all for a small monthly payment that is calculated on the site.

Stillwell’s team also includes others with a background in data and risk analysis. Joseph Kim, listed as Jumpstart’s head of technology, was formerly the vice president of software development with RMS, while Michael Shilman, the lead developer, was the former chief technical officer of Lab80.

According to Crunchbase, which tracks venture capital activity, Jumpstart received $400,000 in angel funding on Sept. 1, 2016. The investors are listed as Berkeley Angel Network and an undisclosed investor. The Berkeley Angel Network is a group of angel investors who are alumni, faculty and former faculty of U.C. Berkeley. The group has invested in a craft beer company, a business in the healthcare industry, a biotech company and an environmentally friendly product maker.

Stillwell’s LinkedIn profile lists her as a graduate of U.C. Berkeley’s Walter A. Haas School of Business.

Financial Product

Tom Larsen, a product architect for Irvine, Calif.-based CoreLogic, which owns EQECAT, is intrigued by what Jumpstart is planning to offer, which he called “purely a financial product.”

However, he emphasized that buyers must be made to realize the risk they are taking by accepting a fixed payout in lieu of compensation for the rebuild value on their homes.

It’s one thing for a sophisticated buyer, such as a large company, to purchase a parametric product because they often buy a wrap-around type of insurance product to cover their loss from a given peril, he said.

A consumer buying only the parametric product for earthquake is relying on luck, he added.

He drove home his point about the randomness of damage that occurs from an earthquake and the difficulty knowing just how much coverage will be enough in the event a temblor strikes.

Not all earthquake damage is total, he noted.

“As a scientist I go to an area after an earthquake has hit and when I see a block of homes, I do not see rubble, rubble, rubble. I see no damage, no damage, oops,” he said. “It’s that uncertainty that your accepting as a buyer for this Jumpstart product.”

Quake Coverage Competitor

The executive who is the face of the state’s earthquake insurance business has heard about what Jumpstart is trying to do, and he has no problem with it.

“We’ve heard of companies like Jumpstart that are exploring offering some sort of parametric product,” said Glenn Pomeroy, CEO of the California Earthquake Authority (CEA).

He said the product may have a few regulatory hurdles to clear but he welcomes it.

While the CEA board has not taken an official stance on parametric products, Pomeroy’s attitude is that the more people in California who are covered for earthquake loss, the better.

“There’s huge uninsured exposure for earthquake in California,” he said. “That’s why we as the CEA have not tended to view other companies that are out there as competitors. Whether someone buys a policy from us or coverage from someone else, we think that’s a good thing.”

A little over 10 percent of California homes have earthquake insurance, according to the California Department of Insurance. This makes California’s market ripe for firms like Jumpstart, Pomeroy said.

“Uninsured risk invites innovation,” he said.

Both Larsen and Pomeroy see the upside in Jumpstart’s business model being that the firm can offer products cheaply because of low overhead.

“They can put a fair amount of coverage out there cheaply because they don’t have all the cost of underwriting or claims adjusting,” Pomeroy said.

Topics Catastrophe California Agencies

Was this article valuable?

Here are more articles you may enjoy.

Former Broker, Co-Defendant Sentenced to 20 Years in Fraudulent ACA Sign-Ups

Former Broker, Co-Defendant Sentenced to 20 Years in Fraudulent ACA Sign-Ups  AI Claim Assistant Now Taking Auto Damage Claims Calls at Travelers

AI Claim Assistant Now Taking Auto Damage Claims Calls at Travelers  Munich Re Unit to Cut 1,000 Positions as AI Takes Over Jobs

Munich Re Unit to Cut 1,000 Positions as AI Takes Over Jobs