Several recent reserve cover deals—including the single-largest reinsurance transaction on record—demonstrate a growing interest on the part of insurers to shed their long-tail liabilities.

A sharp uptick in reserve disposals in 2017, bolstered by continued momentum in early 2018, indicate the legacy market is here to stay. Some 25 reserve covers were closed in 2017—five of them transferring reserves of $750 million or more. Thus far in 2018, approximately 10 deals have been announced.

The rise of the legacy market can be attributed to several factors:

- Sophisticated insurers are questioning the wisdom of carrying large long-tail exposures on their balance sheets when that capital could be better used elsewhere.

- Those same insurers also realize that transferring liabilities can result in a host of immediate financial benefits.

- The legacy reserve cover marketplace has become more robust than ever. New capital and new counterparties interested in higher returns are driving pricing efficiencies as well as new solutions for a broad range of exposures.

Long-tail exposures on balance sheets can drive capital charges and result in volatility and/or lower earnings. In the current market, insurers are being forced to scrutinize their businesses more carefully as earnings power is squeezed. Many are seeking ways to free up capital when legacy liabilities begin to drag on earnings, preferring to focus their efforts on ongoing projects that are core to their business. And with the prospect of a market turn, forward-looking carriers are actively seeking ways to liberate trapped capital.

Benefits of Legacy Transfer Deals?

Legacy transfer deals are no longer considered to be an acknowledgement of failure. They are now seen as a capital management tool for insurers looking to hand off liabilities. Well-structured adverse development covers (ADCs) and loss portfolio transfers (LPTs) provide a number of key benefits, including risk transfer, stabilization of earnings, capital relief, prospective underwriting and enhanced investment returns.

Motivations for purchasing a reserve cover can range from exiting unwanted lines to eliminating the burden of claims handling to releasing capital for new lines of business. An LPT/ADC transaction also can provide stabilized earnings protection, especially when reserves develop adversely or payout is accelerated. And by providing substantial capital relief, these transactions can improve a carrier’s Best’s Capital Adequacy Ratio (BCAR) and/or risk-based capital (RBC) ratio. Rating agencies and regulators value these transactions and reward carriers for purchasing them. Analysts also praise these covers as a way of harnessing volatility and eliminating drag on earnings.

Large, Complicated Deals

By their nature, LPT and ADC transactions are large, complex and require specialized tools. Structuring a reserve cover requires careful consideration of many variables, including quality and duration of reserves, the subject exposure, line of business, respective capital charges, investment parameters, and the overall placement timeline.

It is crucial for the buyer to work with an experienced specialized broker with the requisite analytics capability to determine both the optimal transaction structure as well as a marketing plan before approaching reinsurers/counterparties.

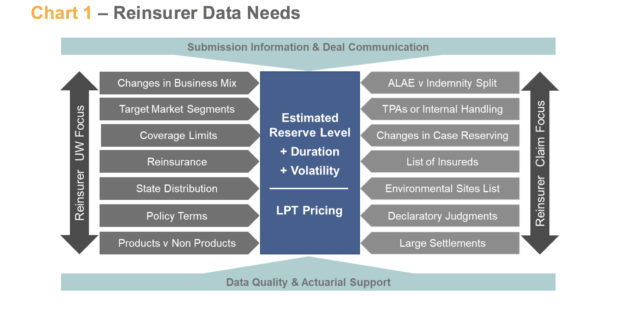

Significant actuarial support of the reserves is an important component of the reinsurer valuation and pricing process. Effective transfer of information through submission materials and appropriate dialogue are core to the process of understanding the nature of the exposure, the level of reserves and the formulation of a reasonable price.

Key information requirements and areas of emphasis for reinsurers are summarized in Chart 1 with underwriting on the left and claims on the right. Reinsurers’ data needs, requests for follow up and discussion typically focus on these areas.

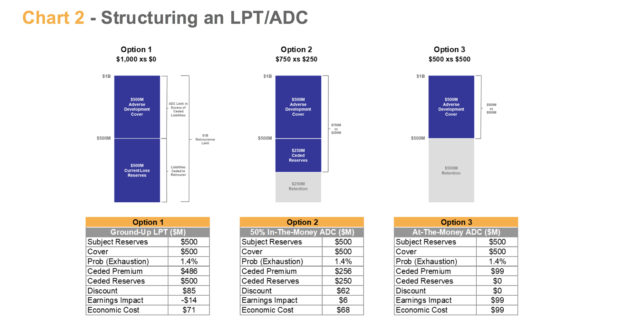

The figures in Chart 2 illustrate the various reserve cover structure options to consider. This example contains sample pricing for an LPT, an “in-the-money” ADC (attachment below subject reserves) and an “at-the-money” ADC (attachment at the subject reserves). Deciding on the objective of each reserve cover is vital before considering alternative structures.

The interplay between the time value discount and the LPT risk load can be seen where these structures have the same point of exhaustion. The full effect of the discount is available in an LPT structure and can offset the risk load cost. In this illustration, the LPT result is a book value gain as the discount more than covers the risk load, whereas the risk load outpaces the discount in the two ADC structures.

What’s Ahead?

Exposures included in reserve covers have moved beyond just asbestos, environmental and workers comp portfolios. Recent transactions have included commercial auto, construction defect, medical malpractice, professional liability and discontinued program business. Down the road, exposures could include claims from sports injuries, mold, talc, sexual harassment and the opioid crisis.

Meanwhile, the legacy market has become attractive for both sides of the table. Buyers benefit by unstacking long-tail liabilities, releasing capital and allowing executives to refocus their attention on go-forward strategies. Sellers, on the other side, have been able to expand their offerings with the aid of outside investors and an influx of new capital, as shown in Chart 3.

Well-executed legacy deals for runoff acquirers of scale are believed to be offering investors double-digit returns, which measure up well against the broader financial markets and live insurance. However, it is important to remember that the dynamics in the legacy sector are distinct from those in the live market. There is a mounting sense that overcapitalization and an increasing number of bidders could reduce returns.

Today, legacy risk transfers are running at a pace similar to last year. Barring any unforeseen disruptions to the market, LPTs and ADCs will remain valuable tools for insurers planning for the future.

This article was originally published in Wells Media Group’s Carrier Management, the magazine for property/casualty insurance carrier executives.

Topics Trends Carriers Reinsurance

Was this article valuable?

Here are more articles you may enjoy.

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026  Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks  Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?  eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million

eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million