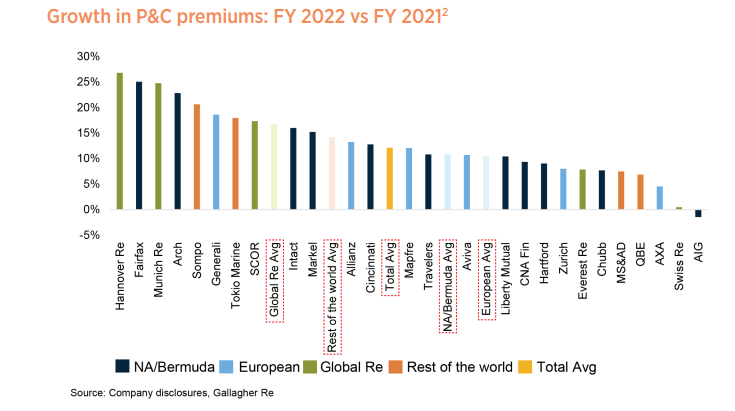

Reinsurers’ premium growth averaged 12.1% for full-year 2022 and 10.2% for the fourth quarter, which was driven by improved pricing for commercial lines and reinsurance business, according to Gallagher Re.

However, the strongest FY 2022 increase of 16.7%-plus came from the global reinsurers analyzed by Gallagher Re: Hannover Re, Munich Re, SCOR, Everest Re and Swiss Re.

“The double-digit growth in premiums on both a quarterly and annual basis continues to be supported by not only price increases but also higher policy retention and organic growth,” said the Gallagher Re report, titled Global reinsurers’ financial results for full year 2022.

(Editor’s note: Gallagher Re said it tracks the largest reinsurers globally who have meaningful commercial lines or reinsurance operations. In other words, a Gallagher representative explained that the report does not only analyze assumed reinsurance figures. For reinsurance-only growth, see the category, “Global Re Avg,” in the chart below).

Inflation hit a 40-year high in many global economies in 2022 and continues to have an impact on industry premium trends.

Apart from AIG, all companies Gallagher Re tracks reported a year-on-year increase in premium. “Sixteen of the 26 companies in our data set reported double digit premium growth and of those, five reported increases over 20%.”

“Although rate increases continue to moderate, some management teams expect overall margin expansion for their commercial lines business in 2023,” the report said.

“Margin trends varied by commercial line of business with workers’ compensation and professional liability lines (e.g., D&O) being viewed as challenged while commercial property pricing has benefited from rising reinsurance costs,” it continued.

While personal lines profits continued to be challenged in 2022, management teams are optimistic about improvements in 2023 as a result of recent rate increases, Gallagher Re said, noting that insurers generally expect strong premium growth to continue throughout 2023.

P&C segment gross premium written, for AXA premiums are gross revenues; for Sompo & Tokio Marine, domestic and international re-calendarised figures are taken. For MS&AD

domestic and MS Amlin, re-calendarised figures are taken. Growth in P&C net premiums for Q4 2022 versus Q4 2021 excludes QBE

Additional themes identified by Gallagher Re from full-year and Q4 reinsurance results include:

- The average combined ratio deteriorated marginally to 95.7% (FY 2021: 94.7%), mainly due to an inflation-driven increase in the attritional loss ratio.

- Investment losses weighed on the average full-year ROE, which dropped to 10% (FY 2021: 12.6%).

- Shareholders’ equity decreased by an average of 27% in FY 2022, driven by unrealised losses on investments and to a lesser extent capital return (both dividends and buybacks).

- Despite declining shareholders’ equity, European solvency remained robust at 235% (FY 2021: 225%), supported by higher risk-free interest rates and retained profits.

- The total average consensus 2023 earnings per share (EPS) estimate was virtually unchanged following FY 2022 results.

The report analyzed the following companies: AIG, Allianz, Arch, Aviva, AXA, Chubb, Cincinnati, CNA Financial, Everest Re, Fairfax, Generali, Hannover Re, Hartford, Intact, Liberty Mutual, Mapfre, Markel, MS&AD, Munich Re, QBE, SCOR, Sompo, Swiss Re, Tokio Marine, Travelers and Zurich.

Source: Gallagher Re

Was this article valuable?

Here are more articles you may enjoy.

Law Restricts Her From Reducing ‘Excessive’ $91M Injured Worker Award, Judge Finds

Law Restricts Her From Reducing ‘Excessive’ $91M Injured Worker Award, Judge Finds  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  Chipwich Maker Withdraws Lawsuit Against Insurance Agency

Chipwich Maker Withdraws Lawsuit Against Insurance Agency