For U.S. property/casualty insurers, net written premium still grew in 2015, but the rate of expansion is slowing, and the industry’s collective combined ratio worsened slightly, according to a new report from ISO and the Property Casualty Insurers Association of America.

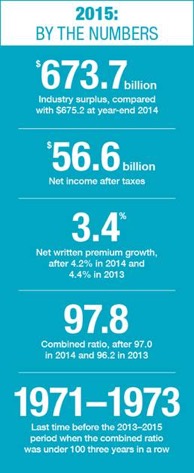

Net written premium grew by 3.4 percent in 2015 versus a 4.2 percent hike in the previous year, and net income after taxes expanded to $56.6 billion, up 1.3 percent from $55.9 billion in 2014.

The combined ratio grew to 97.8 from 97 in 2014. In 2013, the figure was at 96.2. As the ISO/PCI report points out, this is the first time the combined ratio was under 100 three years in a row since 1971-1973.

Insurers managed to stay profitable with an 8.4 percent return on average policyholders’ surplus, essentially the same as 2014.

While it is too early to tell whether deterioration of underwriting results in 2015 reflects a trend, loss ratios are worsening for both personal and commercial auto liability, said Beth Fitzgerald, president of ISO solutions, a Verisk Analytics business.

“Likely factors behind the loss ratio increases for automobile insurance include economic growth and low gas prices, which are putting more drivers on the roads, and increases in automobile costs,” Fitzgerald said in prepared remarks.

She added that the broader trend could be ominous.

“The slowdown of written premium growth for the entire industry could indicate an even more challenging environment for insurers in the near future. Only those insurers best equipped for underwriting will likely see success in the future,” Fitzgerald said.

Robert Hartwig, president of the Insurance Information Institute, said that the results could very well reflect a “new normal” for the industry.

“The industry’s performance in 2015 could be characterized as its ‘new normal,’ neither as profitable as in 2013 nor as affected by catastrophes as in 2011 and 2012. Indeed, in many respects, 2015 looked a lot like 2014,” Hartwig said in an I.I.I. website posting he co-wrote with Steven Weisbart, I.I.I. senior vice president and chief economist.

Additional details:

- Underwriting gains were at $8.7 billion for 2015 versus $12.2 billion in 2014.

- Net investment income grew to $47.2 billion for the year from $46.4 billion in 2014.

- Industry surplus landed at $673.7 billion in 2015, down from $675.2 billion at year-end 2014. The ISO/PCI report blames $38.1 billion in stockholder dividends and $19.7 billion in unrealized capital losses.

- Net earned premiums grew 3.7 percent to $505.8 billion in 2015.

- For the 2015 fourth quarter, the property/casualty insurance industry’s consolidated net income after taxes fell to $12.6 billion from $18.1 billion in the 2014 fourth quarter.

- Net written premiums in Q4 2015 came in at $121.3 billion, a 1.3 percent increase compared to $119.7 billion in the 2014 fourth quarter.

- The Q4 2015 combined ratio was at 100.5, up from 94.9 in the 2014 fourth quarter.

Source: ISO/Verisk Analytics, Property Casualty Insurers Association of America

Topics Trends Carriers Profit Loss Pricing Trends Property Casualty

Was this article valuable?

Here are more articles you may enjoy.

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?  Troubled Alabama City Loses its Liability Insurance Coverage

Troubled Alabama City Loses its Liability Insurance Coverage  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers

Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers