The number of insurance agency mergers and acquisitions in the first half of 2016 ranked as second-most-active six-month period since 2008.

According to a new report on agency merger acivity by Chicago-based investment banking and consulting firm OPTIS Partners, which began tracking transactions in 2008, there were 232 announced deals over the period, one fewer than the 233 done in the first half of 2015.

The OPTIS database covers U.S. and Canadian agencies selling primarily property/casualty insurance, agencies selling both P/C insurance and employee benefits, and those selling only employee benefits.

“Buyers and sellers continued to feed their hearty appetites for deals and push up the M&A activity trend line,” said Timothy J. Cunningham, managing director of OPTIS.

Agency M&A activity has climbed steadily over the past four years, other than the spike at the end of 2012 and related drop in early 2013 related to the tax-law change, he added.

“We anticipate the recent strong industry-consolidation trend will continue for the near term as acquisitions are an important growth strategy for many firms, especially those backed by private-equity capital,” Cunningham said.

Agency Valuations Near Peak

Strong buyer interest is pushing up prices.

“If you’re an agency owner thinking about the best time to put your agency in play, consider taking action sooner than later,” said Daniel P. Menzer, CPA, partner with OPTIS. “Interest from buyers is high and agency valuations are near their peak.”

But buyers need to crunch the numbers and do due diligence, he cautioned.

“A premium price paid for acquisition can have significant adverse implications on the long-term viability of your agency,” he added. “If the agency you buy does not perform up to snuff and you do not have the capital base to absorb the shortfalls, you can get in a lot of trouble.”

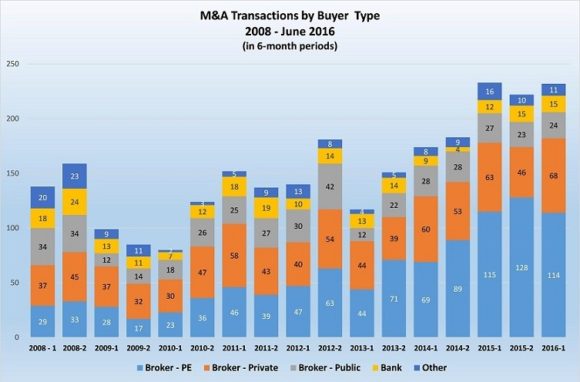

The OPTIS report breaks down buyers into five groups: private-equity backed brokers, privately held brokers, publicly held brokers, banks, and all others.

Private-equity backed buyers continued to lead the charge with 114 transactions. Privately-owned brokers were the second-most active group of buyers with 68 deals—or 29 percent of the total, up from 24 percent during the year-earlier period. Publicly-traded brokers announced 24 deals, down three deals from last year’s first-half count.

Banks announced 15 transactions, three more deals than during last year’s first half. Insurance companies and other buyers also were less active this year compared to the first six months of 2015 and remain relatively inactive.

Agency acquisitions continue to focus on P/C shops (124 announced transactions) and P&C/benefits brokers (40 deals). There were 43 employee benefits agency sales.

Topics Mergers & Acquisitions Agencies Property Casualty Employee Benefits

Was this article valuable?

Here are more articles you may enjoy.

Viewpoint: The AI Ransomware That Couldn’t Get Paid

Viewpoint: The AI Ransomware That Couldn’t Get Paid  Air Taxi Service Across Parts of Florida Moving Closer to Reality

Air Taxi Service Across Parts of Florida Moving Closer to Reality  One Weather Firm Warns New England Could See Big Hurricane This Season

One Weather Firm Warns New England Could See Big Hurricane This Season  Tropical Storm Watches Posted Across Florida’s Panhandle Region

Tropical Storm Watches Posted Across Florida’s Panhandle Region