For private U.S. property/casualty insurers, the first nine months of 2016 were markedly worse than the same period in 2015, due to higher catastrophe losses and less favorable reserve development.

The period produced a $1.7 billion net underwriting loss versus a $7.3 billion underwriting gain from January through September 2015, according to ISO, a Verisk Analytics business, and the Property Casualty Insurers Association of America.

Similarly, insurers’ combined ratio came in at 99.5, worse than the 96.9 figure from the first nine months of 2015. Net premium growth slowed to 2.8 percent from 4.1 percent a year earlier, and net investment income dropped to $33 billion from nearly $35 billion over the first three quarters of 2015.

Robert Gordon, PCI’s senior vice president for policy development and research, said that auto lines have presented one of the industry’s bigger problems over the last year.

“Some of the poor performance is a result of increasing loss ratios in the auto lines, which were affected by rising accident frequency and severity,” Gordon noted in prepared remarks.

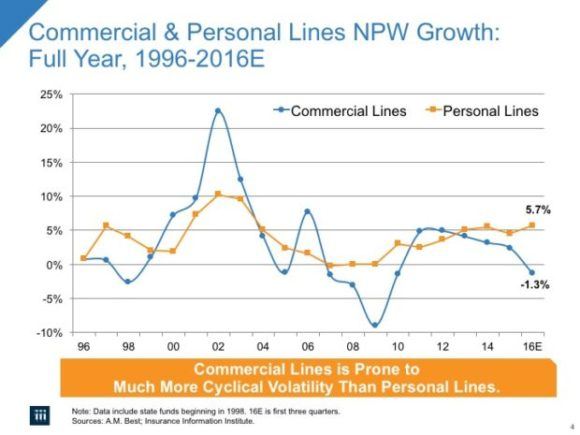

The combined ratio for personal lines insurers worsened to 102.9 over the first nine months of 2016 due to personal auto loss ratio hikes, and commercial loss ratios also increased—factors that will need to be addressed, Gordon said.

“As we move forward, it’s important for all the stakeholders — including consumers, insurers and policymakers — to take significant steps to reduce the growth of auto losses,” Gordon said.

Steven Weisbart, Insurance Information Institute chief economist, noted in an analysis of the report findings that the current climate of super-low interest rates puts added pressure on insurers to maintain healthy combined ratios.

“These days, with investment income below levels that would be produced if interest rates were at higher levels, P/C companies generally need to maintain combined ratios below 95 in order to earn their cost of capital in a still-challenging interest rate environment,” Weisbart wrote.

Beth Fitzgerald, president of ISO solutions, said that the market is showing promising signs, despite the challenges.

“Policyholders’ surplus continued to grow and reached a record high of $688.3 billion. The Federal Reserve raised interest rates in December 2016 and is expected to increase rates further in 2017,” Fitzgerald said, also in prepared remarks. “Still, it will take time for insurers’ investment yields to improve.”

Fitzgerald said that insurers will succeed in today’s market by focusing on their underwriting and incorporating “robust data and analytics” into the process.

Other report results from the first nine months of 2016:

- Earned premiums came in at $390.7 billion, a 3.6 percent spike over the previous year.

- Net written premiums landed at $403.8 billion compared to nearly $393 billion over the same nine-month period in 2015.

- Insurers’ realized capital gains dropped to $5.6 billion from $8.8 billion in 2015.

- Net investment gains came in at $38.6 billion compared to $43.7 billion over the same period in 2015.

Source: ISO/Verisk, PCI

Was this article valuable?

Here are more articles you may enjoy.

Zurich CEO Says Staff Let Go as Regulator Finma Imposes Partial Sales Ban

Zurich CEO Says Staff Let Go as Regulator Finma Imposes Partial Sales Ban  Former Insurance Agent Sentenced to Jail for Fraud, Again

Former Insurance Agent Sentenced to Jail for Fraud, Again  Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver  Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026