At the start of the 2022 Atlantic hurricane season, Insurance Journal spoke with Karen Clark, founder of two catastrophe modeling firms and now CEO of Karen Clark & Company (KCC). August 24, 2022 is the 30th anniversary of Hurricane Andrew – a storm that validated the industry she helped create.

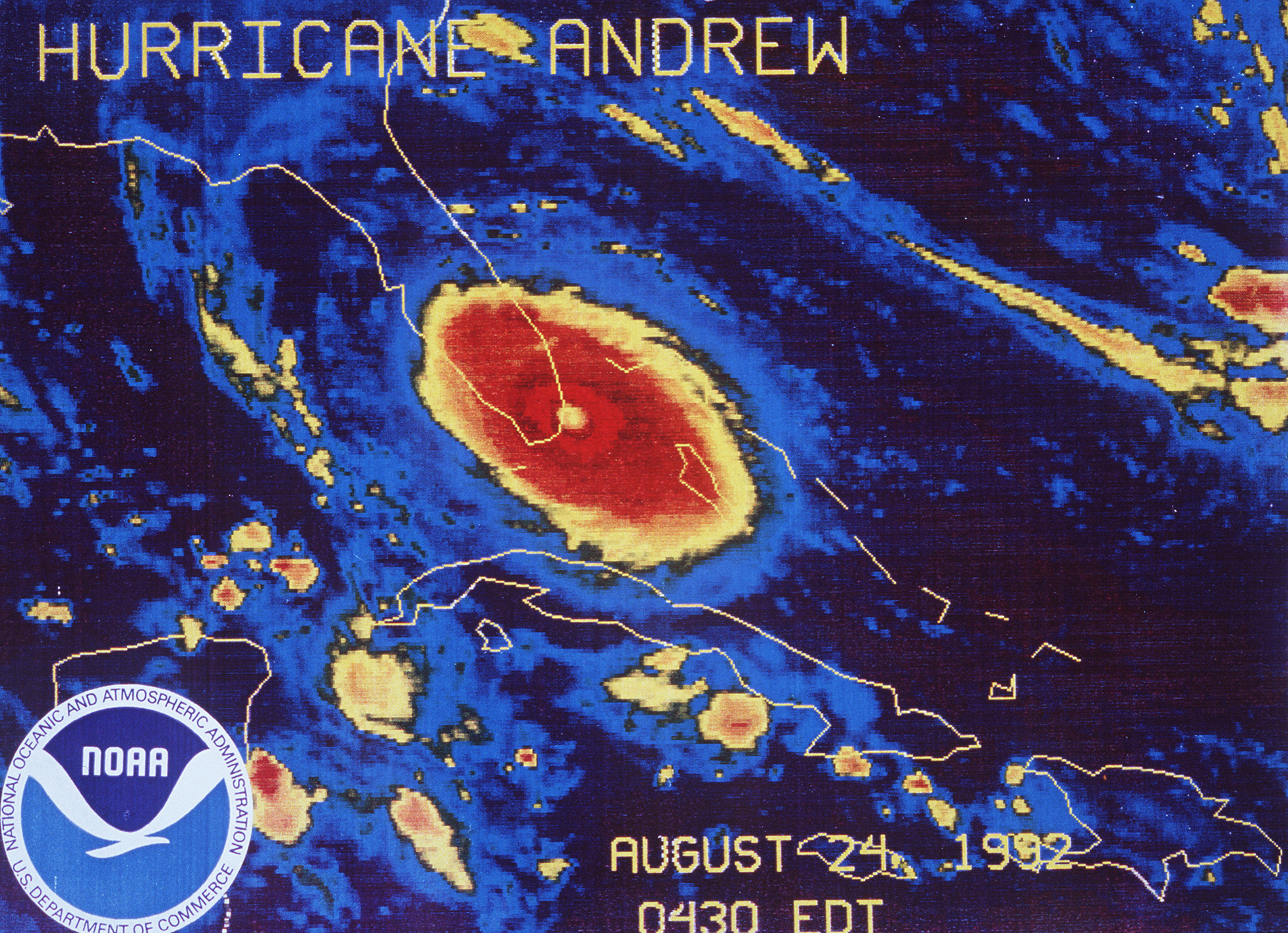

Shortly after Hurricane Andrew barreled to shore just south of Miami with winds of 165mph on the morning of Aug. 24, 1992, the catastrophe modeling company Karen Clark had established – Applied Insurance Research, later AIR Worldwide – ran the data through the model.

With a loss estimate in hand, she headed to the fax machine to send clients the news.

“I remember the day like it was yesterday,” Clark told Insurance Journal. “Our clients couldn’t believe it. The phones started ringing right away.”

Of the 30 or so mostly London-based reinsurance-company clients AIR had, Clark recalled one betting her 5 quid Andrew wouldn’t cost the insurance industry more than $6 billion.

AIR’s model projected Andrew could cost more than twice that – $13 billion. The model she built to start the catastrophe modeling industry in 1987 with AIR, was on point. Andrew’s cost to insurers was about $15.5 billion in 1992.

The skepticism as the model’s estimates were distributed may have been somewhat warranted. Prior to Andrew, the largest insured loss from a hurricane was $4 billion in 1989 from Hurricane Hugo, which struck South Carolina.

“People weren’t tabulating property values,” Clark explained. “There hadn’t been a hurricane like Andrew in such a populated area. Even though it missed Miami, the property values were still much more than South Carolina.”

In fact, 1992’s Andrew could have been much worse. If the storm struck Florida 50 miles or so north, Miami would have been impacted and insured losses would have been closer to $60 billion, Clark added. Today, Andrew would cause about $70 billion in losses and a hit to Miami would cause over $200 billion in losses, she said.

Still, Clark admitted that as the fax machine made its distinctive sounds and the papers were scanned 30 years ago, “We were not 100% confident. We were questioning ourselves.

“But it’s what the model told us, and we did the work to make it as accurate as possible. We felt like we needed to give it to clients.”

The insurance industry realized the model was a tool it could use to do what it struggled to achieve – better estimate loss potential and price insurance products. Following Andrew and the model’s validation, the first class of Bermuda reinsurers was spawned in 1993. Then catastrophe bonds and insurance-linked securities followed to supply capacity. Today, catastrophe models like the ones from Clark’s KCC, are the global standard technology for risk assessment. (Clark sold AIR to Insurance Services Office, now a subsidiary of Verisk Analytics, in 2002 and founded Karen Clark & Company in 2007.)

Interestingly, the industry’s reliance and/or confidence in catastrophe models has ebbed and flowed. Over the last several years, reinsurers in particular have become more skeptical after years of arguably, Clark said, leaning on the models too much. Recent cynicism has led to the application of adjustment factors – crude multiples on top of the traditional model loss estimates.

“We noticed that and asked ourselves how we can make the models better,” Clark said. “One way is to put our models out there when there’s an actual event – as we always have. Clients can see and run their own estimates. When their actual claims start coming in, they share the data with us. This creates an ecosystem that allows us to continually refine the KCC models.”

Clark described the model as an infrastructure, such as a highway system, that can be customized for clients’ vehicles and traffic, metaphorically speaking, to be more reflective of specific policyholder and claims data.

With the rapid evolution of technology, data from satellite images, aerial photography, and machine learning can be imported into the model to improve it.

“The goal is always to enhance accuracy and therefore the level of confidence in models,” Clark said. “There’s always work to be done. The value is the infrastructure and transparency. You can apply modeled events to your own book of business and drill down.”

Looking ahead, Clark said her company developed a catalogue of scenarios to give views 5, 10 and even 25 years into the future of how storms might evolve and cause damage, considering the scientific community has predicted an increase in the severity of hurricanes due to changes in climate.

“There are some uncertainties, such as with efforts to curtail greenhouse gases, but now clients can confidently tell investors and regulators that they are on top of climate change,” Clark said.

Top photo: In this Aug. 25, 1992 file photo, Hurricane Andrew-damaged houses sit between Homestead and Florida City, Florida. (AP Photo/Mark Foley, File)

Was this article valuable?

Here are more articles you may enjoy.

Company at Center of Cyclospora Outbreak Complained to White House, Source Says

Company at Center of Cyclospora Outbreak Complained to White House, Source Says  AM Best Calls $1.54 Billion Mapfre-Safety Marriage ‘Strategically Compelling’

AM Best Calls $1.54 Billion Mapfre-Safety Marriage ‘Strategically Compelling’  Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver  Trump’s Diversity Crackdown Reverberates Through US Boardrooms

Trump’s Diversity Crackdown Reverberates Through US Boardrooms