In a quiet commercial strip in an upscale suburb of Nashville, there’s a single-story brick building housing a company that may determine whether another billion-dollar taxpayer bailout of the coal industry is needed.

It is the main office of Indemnity National Insurance Co., a specialty insurer whose health underpins the financing for the cleanup of almost one-fifth of the US coal mining industry.

Coal mines can do a great deal of damage while they’re operating—and after they shut down. They can leave behind huge pits and leveled mountain tops. They can poison streams. That is why, since 1977, federal law compels mining companies to return the land to the way it was, a process known as reclamation that can include replanting the land and treating polluted waters. But an investigation by Bloomberg News and NPR has shown that big coal companies have often avoided this expensive responsibility by transferring mining permits to smaller companies that don’t always have the resources to fulfill their obligations.

Standing between taxpayers and the potential mess is insurance.

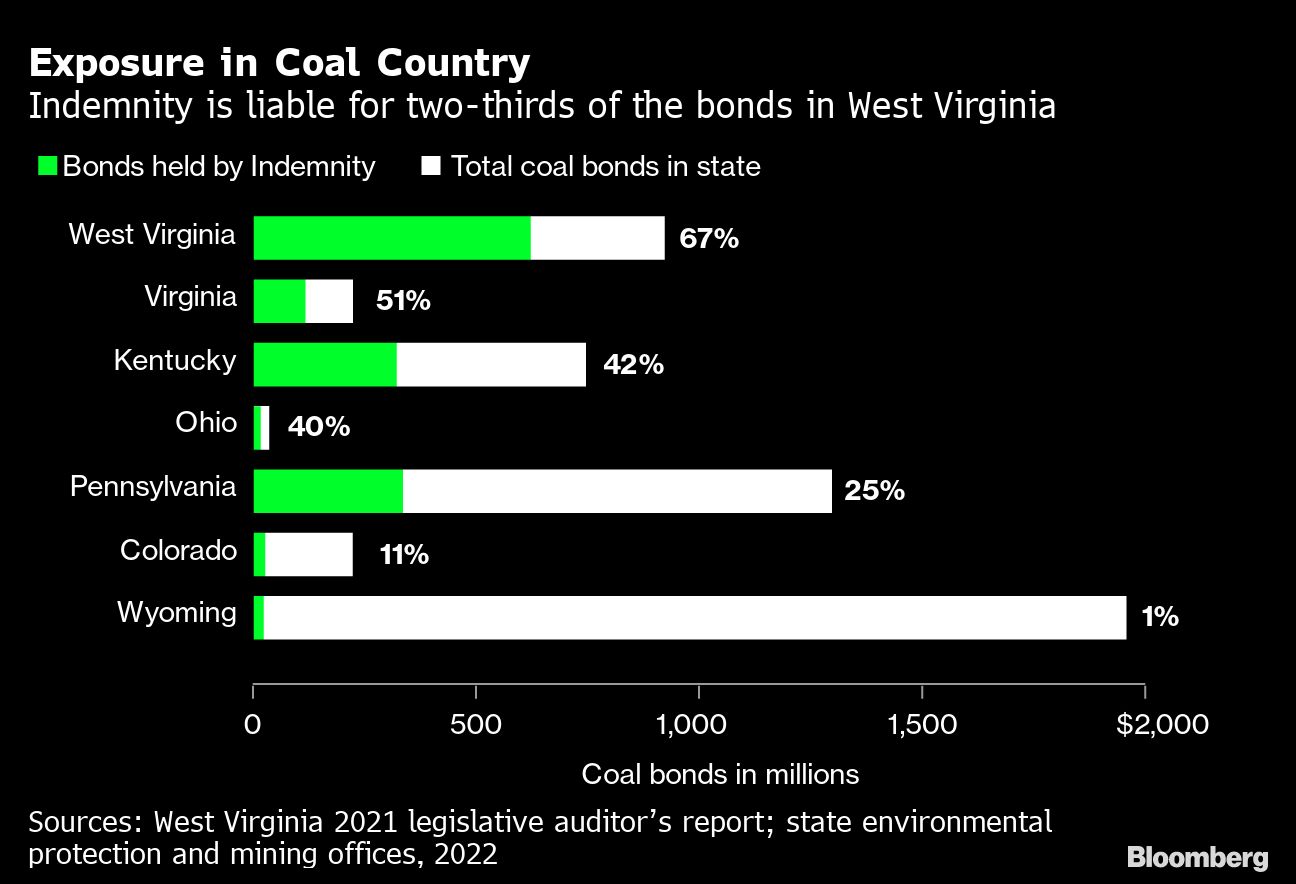

The 1977 law required mining companies to purchase bonds guaranteeing some of the cost of reclamation as a condition for getting a permit to start digging. As of 2017, there were $10.2 billion in coal bonds across the country, according to a 2018 report by the US Government Accountability Office. The vast majority of these are purchased through third-party insurers and are known as a surety bonds. Premiums from surety bonds can be attractive, but they come with serious obligations. If a mining company cannot afford to clean up a site, the state can “call the bond”—forcing the insurer to either give them money or complete the reclamation itself. Indemnity is underwriting at least $2 billion of those surety bonds, public records in top coal-producing states show. In West Virginia alone, the company holds 67% of the total, or $620 million, according to a report published by the state legislature’s auditor in June 2021.

The aggregation of all that potential liability into one coal-heavy portfolio has caught the attention of environmental groups such as the Sierra Club and Appalachian Voices, as well as that of state officials, researchers and academics who warn of danger ahead. Concerns about climate change have altered the equation about coal investing, they say.

Erin Savage, a scientist with Appalachian Voices, a Boone, North Carolina-based organization dealing with the long tail of coal mining pollution, has made it a pet project to research Indemnity’s holdings in states beyond West Virginia and was shocked by what she found. “I was totally surprised to see just how widespread Indemnity is at this point. Common sense is that this is incredibly risky under the current market conditions.”

The push to decarbonize has made the dirtiest fossil fuel a pariah. Coal prices are booming this year, largely the result of the war in Ukraine, but that comes after a precipitous decline in which the industry closed more than half of its production since the peak in 2008.

The industry’s future remains bleak. Earlier this year, President Joe Biden signed the Inflation Reduction Act, with incentives for more renewable energy. Rhodium Group LLC, an independent research and analytics company, estimates the law should cut coal production in the US by at least half again by 2030. That means more coal mines will close.

Multiple mine bankruptcies at the same time could overwhelm Indemnity. A top regulator in West Virginia testified in a court case in 2020 that a group of troubled mines there had already placed Indemnity at risk of going bankrupt, potentially putting taxpayers on the hook.

Dan Cohn, a researcher at the nonpartisan Institute for Energy Economics and Financial Analysis, hasn’t studied Indemnity specifically but has looked at fossil fuels and says it’s a well-worn playbook. “We’ve seen that again and again in the extractive industries,” he says, “where companies pass the buck to undercapitalized operators, who then quietly slip away in the night, and the states are left with the cost of cleaning up.”

David Wiley, chief executive officer of Indemnity’s parent company, Kewa Financial Inc., disagrees. He says he knows the history of the coal industry and why there might be concern, but he’s confident this time things will be different. “The days of the coal barons are gone,” he says. “These are big corporate companies. They have shareholders and employees and regulatory bodies that they’re obligated to satisfy.”

Wiley, 53, is an odd mix of elusive and confiding. It takes months of cajoling to have him schedule an on-the-record discussion about his company. When he finally gets on the phone, he quickly volunteers that he is at a weight-loss program in Florida and that his ex-wife died in a tragic boating accident. He answers some questions on the phone, but for others he insists on replying by email.

Then, in October, he agreed to another interview. “The price is going up,” he says, referring to coal. “Our clients are phenomenal, phenomenal people whose credit quality has just gone parabolic.”

Public information about Wiley is scarce. He’s been an owner or executive of small energy or energy-consulting companies for two decades, according to his LinkedIn profile. From 2004 to 2010, he was president and CEO of Phoenix Coal Inc., but he left when the company sold its coal assets and shifted to other kinds of mining. In April, he bought an $11 million home in Naples, Florida, according to public records.

Wiley says his experience enables him to run a coal bonding company that is astute at managing risk. “Like any insurer, we employ traditional underwriting, claims and actuarial expertise,” he says. “We conduct regular inspections of the mines we bond and calculate risk on the ground that is based on the actual cost to reclaim.”

It’s been a profitable few years for Indemnity. The company wrote $61.6 million in gross premiums last year, up from $11.3 million in 2017, according to annual filings required by regulators. It had a net loss ratio—a key metric of health that calculates incurred losses against collected premiums—of 8.9% last year, down from almost 20% in 2019. The lower the ratio the better, and surety providers across all industries typically have loss ratios of 10% to 20%, according to JD Weisbrot, president and chief underwriting officer of JW Surety Bonds, which bills itself as the biggest US surety company.

Indemnity has used these fat years to reward investors, financial statements show. It had net income of $17.1 million last year and paid $5 million, almost 30% of that, in dividends, twice what it paid out in 2020—leaving less money on hand bank for mine cleanup in the event of a downturn. That’s a lot of dividends, especially for a company that made a strategic shift to go deep into coal sureties a few years ago, says Weisbrot. “A newer surety should be banking their reserves as much as possible,” he says.

When Congress wrote the Surface Mining Control and Reclamation Act in 1977, it gave states a fair bit of leeway on how to mandate mine cleanup. Some states, including West Virginia, formed their own reclamation funds with taxes on coal. These funds serve as backup if mine owners go broke and their bonds aren’t sufficient.

But neither Congress nor the states foresaw at the time that the US would one day have to stop burning coal to save the planet from the worst effects of climate change. Cheap natural gas replaced coal for power production, and then pressure increased to switch to renewables. Coal companies went bankrupt and walked away from billions of dollars of liabilities for pension funds and black lung benefits. In 2021, a bipartisan infrastructure bill included $11.3 billion from taxpayers to pay for the cleanup of mines dug before 1977.

As the coal industry contracted, climate activists spread their sights beyond mine owners to coal financiers, pressuring them to get fossil fuels out of their portfolios. Big insurers such as Liberty Mutual Group Inc. and Zurich Insurance Group AG, announced they were restricting new coal business.

There are many reasons for the pullback, including rules that make coal bonds particularly onerous. But climate concerns dominate. Weisbrot says he has been steadily getting out of coal, which now makes up less than 1% of his portfolio. “I would not want to own a surety that has a concentration almost purely in a hazardous obligation on an industry that’s on the way out the door,” he says.

The retreat of larger insurers left a hole in the market. In 2017, after a run of coal bankruptcies, Wiley bought Indemnity, then a small independent firm, and began rushing into the gap. In addition to two-thirds of the coal bonds in West Virginia, Indemnity now has more than 40% in Kentucky, according to state records. It has significant holdings in Pennsylvania, Virginia and Ohio as well.

It’s not just that Indemnity is growing in absolute holdings, it is also picking up some of the riskiest assets, according to the auditor for the West Virginia legislature. His report found that all but six of the coal companies with mining operations in the state and a minimum of $4 million of Indemnity bonds had had past bankruptcies.

Another major shortcoming: Those risks are not part of a diverse portfolio whose profits in another sector could offset losses in coal.

Wiley acknowledges that a significant portion of his business is in coal sureties, but he sees this as a strength rather than a weakness. “It is the bread and butter of our business and the thing we know best,” he says. “We’ve gotten to know our clients really, really well, and they are good people doing good jobs. They are really strong.”

Joshua Macey, a University of Chicago Law School professor who has studied coal reclamation, sees it differently. “We are very worried about insurers that are completely exposed to a single industry,” he says. “There is good reason to think small companies that are not not diversified will not be able to perform reclamation obligations.”

Wiley has shown himself capable of biting off more than he can chew. In 2018, he went into business with Tom Clarke, a Virginia entrepreneur who saw potential in troubled fossil-fuel extraction companies. Indemnity had agreed to secure the bonds on most of the old coal mines acquired by Clarke’s company, ERP Environmental Fund Inc.

Then Wiley and Clarke each took a 50% stake in Epic Cos., which provides repair and decommissioning services for offshore oil wells. The company expanded wildly, taking on more than $100 million of debt. A year later it was in bankruptcy.

One of its creditors, Offshore Technical Solutions, a Houma, Louisiana-based provider of services for offshore oil rigs, is owed more than $277,000. Richard Burgo, the company’s general manager, says he doesn’t expect to ever get it back. “It was a significant amount for us,” Burgo says. “We’re a small company. This is my livelihood.”

Wiley declined to answer questions about Epic. Clarke didn’t respond to numerous requests for comment.

The real measure of Indemnity is how it would hold up if companies that own the mines that Indemnity bonds went bankrupt at once. That’s what almost happened in 2020. Clarke’s ERP, which owned dozens of defunct mines in four states but no productive ones, ran out of cash and couldn’t meet its cleanup obligations. State regulators could still tap $115 million in ERP surety bonds, but one company—Indemnity—had issued almost all of them.

So that March, Harold Ward, then the director of the Division of Mining and Reclamation at the West Virginia Department of Environmental Protection, told a state judge in an affidavit that if ERP were allowed to go bankrupt, it could result in “potentially bankrupting the Defendant’s principal surety.”

Instead, Ward persuaded the judge to place ERP in receivership, buying time to sell assets and delay a bankruptcy filing.

Wiley says his company would not have gone bankrupt. He maintains that state regulators are doing a good job but don’t necessarily understand his business. He said there were enough reserves, collateral from the mine owners and reinsurance that Indemnity would have made it through.

But Savage, the scientist with Appalachian Voices, says: “The fact that we have multiple state agencies working with Indemnity to avoid actually forfeiting the bonds means we have a problem.” In a report last year, Savage estimated the cost of reclaiming all of Appalachia’s coal mines at $8 billion to $10 billion, an amount way too large for state reclamation funds to cover.

The other possible danger, Savage says, is that “a lot of these mines won’t be cleaned up in a timely manner, and they will cause problems like water pollution, erosion, and earth instability for the people who live near them.”

Wiley says his company is working with the receiver and other mining companies and sureties to clean up the mess. He says so far he has reduced Indemnity’s exposure to ERP bonds by 43%. Some of that was accomplished by doing the reclamation work, but much of it was by transferring the mines—and the associated bonds—to other companies. The primary recipient, Blackhawk Mining LLC, is one of the biggest coal producers in the state.

Still, Indemnity’s work is hardly done. Public records show that at the time of the receivership in March 2020, ERP had 120 mining permits. West Virginia DEP spokesman Terry Fletcher says ERP currently holds 73 mining permits in the state, and Indemnity is the bonding institution for 69 of them.

It is difficult to know from public records just how much Indemnity has paid out for reclamation so far. Both the West Virginia DEP and the receiver appointed for the mines, R. Barry Doss, declined to give a figure.

Wiley says Indemnity has spent “a significant amount of money, but also time and effort and resources.” Asked if it was anything close to the $115 million face amount on the bonds for the ERP mines, he said, “No.”

Despite Wiley’s assurances, West Virginia lawmakers worry about Indemnity’s outsize role in the coal business. “If something happened in Alabama, Tennessee, Kentucky—even West Virginia—whoever is first at the trough will be able to get their resources to be able to do the mine reclamation,” says Craig Blair, president of the state Senate. “The rest of us will be left hanging out in the cold with that exposure up to $8 billion.”

Earlier this year, Blair led a campaign to create a mining insurance company funded by West Virginia that will be an alternative to the private market. It is essentially a recognition that if Indemnity fails, few others would be willing to underwrite those risky bonds.

That wouldn’t help fund cleanup of the mines that Indemnity bonded. West Virginia would still have to drain its state reclamation fund while battling it out with other states for what’s left of the company’s assets.

“The options now are both unpleasant,” says Macey, the law professor. “You could have a taxpayer-funded cleanup. But if local regulators don’t have the appetite to go to the state for more money, these mines might just sit there, abandoned, and leak toxic substances and make the water undrinkable and agriculture poisoned.”

—With Dave Mistich and Zachary R. Mider. This story was reported in collaboration with NPR, which aired several broadcasts on the subject.

Photo: Hopper cars laden with coal trail behind an eastbound Norfolk Southern Corp. freight train heading through Waddy, Kentucky, U.S. Photo credit: Photo credit: Luke Sharrett/Bloomberg.

Topics Carriers

Was this article valuable?

Here are more articles you may enjoy.

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns  State Farm to Begin Issuing Dividend Payments to Louisiana Drivers

State Farm to Begin Issuing Dividend Payments to Louisiana Drivers  OpenAI Finds Evidence Other AI Agents Escaped Containment as it Widens Probe

OpenAI Finds Evidence Other AI Agents Escaped Containment as it Widens Probe  Troubled Alabama City Loses its Liability Insurance Coverage

Troubled Alabama City Loses its Liability Insurance Coverage