The U.S. homeowners insurance segment posted its worst underwriting results in over a decade in 2023, according to an analysis by S&P Global Market Intelligence.

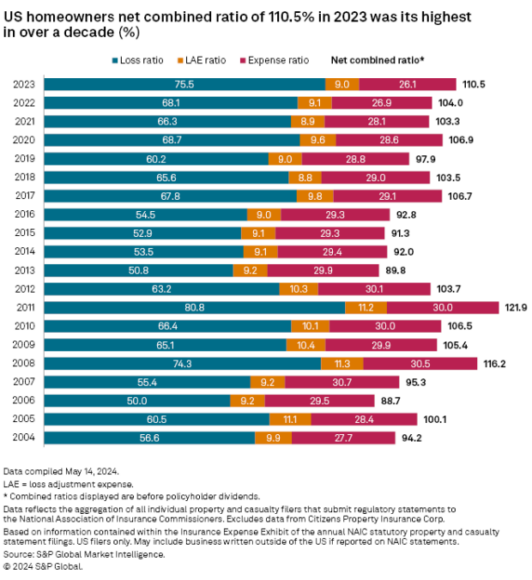

The net combined ratio for the homeowners business, excluding policyholders’ dividends, was 110.5 in 2023, the highest since 2011 (121.9).

S&P said inflationary pressures, the devastating wildfire in Hawaii and a record-breaking number of billion-dollar loss events from convective storms weighed on the industry’s results.

Despite boosting rates across the U.S., homeowners insurers saw net underwriting losses of about $15 billion in 2023, compared to about $5.9 billion during the previous year, excluding state-backed insurers of last resort, S&P said in its market analysis.

U.S. homeowners insurers saw their net losses and loss adjustments expenses jump to about $101.3 billion in 2023, a year-over-year increase of 21.3%, while net premiums earned grew by 10.8% to about $119.9 billion. Other underwriting expenses equaled $33.4 billion during the year compared to $30.6 billion during 2022, according to the analysis.

Among the 20 largest U.S. homeowners insurers, only Chubb Ltd. and Amica Mutual Insurance Co. saw combined ratios under 100 in 2023. Chubb’s net combined ratio was 89.6 in 2023, while Amica posted a combined ratio of 97.4.

Florida’s Citizens Property Insurance Corp. became one of the 10 largest U.S. homeowners underwriters in 2023, knocking Progressive into the No. 11 spot. Citizens reported direct premiums written of about $3.2 billion—up 42.2% percent year-over-year.

In aggregate, the P/C homeowners industry recorded $152.5 billion in direct premiums written during the most recent year compared to $133.8 billion in 2022.

See the full S&P Global Market Intelligence report for more information.

Topics USA Carriers Homeowners

Was this article valuable?

Here are more articles you may enjoy.

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026  American Family to Acquire Bowhead Specialty in $1.2B Cash Deal

American Family to Acquire Bowhead Specialty in $1.2B Cash Deal  Great American Escapes Coverage for Grocery’s Opioid Litigation Settlement

Great American Escapes Coverage for Grocery’s Opioid Litigation Settlement  FTC Sues Hims & Hers for Sending User Health Info to Meta, Snap

FTC Sues Hims & Hers for Sending User Health Info to Meta, Snap