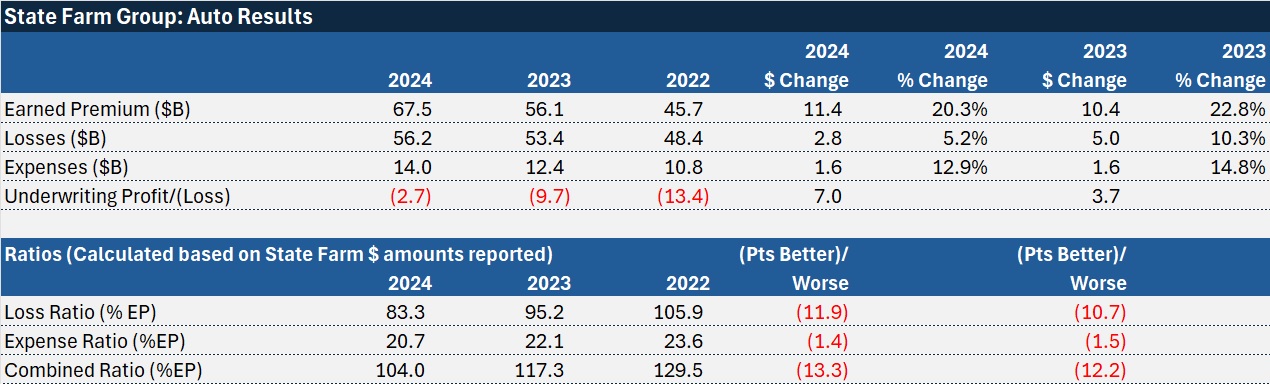

After reporting underwriting losses of $13 billion in 2022 and $14 billion in 2023, State Farm recorded another underwriting loss for 2024—but narrowed it thanks to its auto insurance results.

State Farm reported a 2024 net income of $5.3 billion compared to a net loss of $6.3 billion in 2023. The reported net income for 2024 includes the impact of $3 billion of realized capital gains, net of tax.

With an underwriting loss of just over $6 billion for 2024, State Farm’s auto results drove the improvement. Though auto earned premiums jumped 20% to $67.5 billion, auto underwriting results were still written in red ink, but the underwriting loss was $2.7 billion in 2024—$7 billion less than the $9.7 billion auto underwriting loss recorded in 2023.

Translated to a combined ratio, that’s about a 104 for 2024—more than 13 points better than 2023’s auto combined ratio of roughly 117.

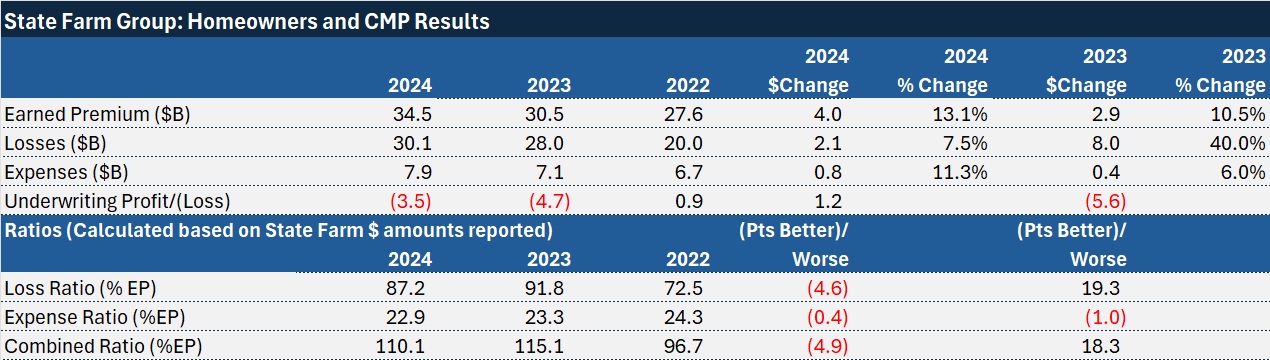

For property lines, earned premiums rose 13.1% to $34.5 billion, but underwriting losses improved by only $1.2 billion, coming in at $3.5 billion for 2024.

In total, State Farm said its property/casualty companies reported a combined underwriting loss of $6.1 billion on earned premium of $103.0 billion. The 2024 underwriting loss, combined with investment and other income of $6.0 billion, resulted in a P/C pre-tax operating loss of $111 million, compared to operating losses of more than $8 billion in the prior two years.

Total revenue, which includes premium revenue, earned investment income, and realized capital gains and losses was $123.0 billion for 2024, up 18% from $104.2 billion for 2023.

Auto Improvement vs. Competitors

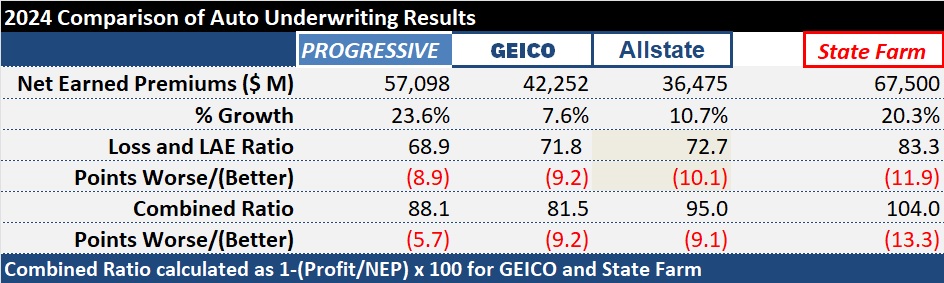

Focusing on just the most improved part of State Farm’s P/C businesses—the personal auto results—the nearly 11.9-point drop in its loss and loss adjustment ratio was larger than three competitors, Progressive, GEICO and Allstate.

All four carriers reported improved underwriting results, but State Farm’s personal auto loss and LAE ratio, at 83.3, remained higher than the 81.5 auto combined ratio of GEICO, which includes underwriting expenses for the direct writer, GEICO.

Progressive’s 2024 combined ratio, 88.1, was only five points higher than State Farm’s loss ratio.

According to figures compiled by Carrier Management from financial reports of all four carriers, State Farm also reported lower growth in auto earned premiums than Progressive in 2024, with Progressive’s earned premiums jumping nearly 24%, beating State Farm’s 20% jump in earned premiums.

Financial Strength and Parental Support

In a statement, State Farm stressed the financial strength of State Farm Mutual Automobile Insurance Company, noting the net worth for State Farm Mutual Auto ended the year at $145.2 billion compared to $134.8 billion at year-end 2023.

“The financial strength of State Farm Mutual Automobile Insurance Company and each of its affiliates is key to fulfilling our promises to customers in the future and expanding and enhancing the way we serve customers,” the nation’s largest insurance group said in a statement.

State Farm also gave an update of the impact from the January 2025 California wildfires. “As of February 26, we’ve received more than 11,750 total fire and auto claims related to the fires and have paid nearly $2.2 billion to our customers,” said Treasurer and Chief Financial Officer Mark Schwamberger.

He added, “The financial strength of each affiliate is critical to our ability to keep those promises, and we will continue to take a state-specific approach in the way in which we operate.”

The reference to the separate financial strength of each affiliate appeared again in a footnote of the media statement: “State Farm Mutual Automobile Insurance Company and each of its affiliates must meet solvency and regulatory requirements on an individual entity-by-entity basis without regard to the solvency or financial condition of any other affiliated entity.”

That footnote is not new. It was included at the bottom of prior financial reports from State Farm. But this year, it seemed to take on more significance, with the focus on one particular affiliated entity—State Farm’s California homeowners insurance company, State Farm General.

The question of whether State Farm’s parent company, State Farm Mutual Automobile Insurance Company, “would be willing or able to provide financial support to” State Farm General was raised by California Insurance Commissioner Ricardo Lara during a meeting to discuss State Farm General’s request for his approval of an emergency interim rate increase last week. The meeting, which involved representatives of State Farm General, the department of insurance and consumer group Consumer Watchdog, took place just two days before State Farm’s overall financial results were published.

Beyond written responses State Farm General executives sent to Commissioner Lara in a letter the day before the meeting, a transcript of the proceedings that Carrier Management located online shows executives again stressed the need for individual affiliates to remain financially viable but indicated that the approval of a 22% emergency rate increase would help them in taking a request for support to the parent company board.

Keesha-Lu Mitra, senior vice president and general counsel, noted the State Farm Mutual board is comprised of all external, independent directors except for the State Farm Mutual chief executive officer. “[T]heir fiduciary duties require them to exercise reasonable care, judgment, and diligence of what is in State Farm Mutual’s best interest as an entity and its policyholder group as a whole of State Farm,” she said, according to the transcript. The California company would expect the members of State Farm Mutual’s independent board to give “robust consideration” to any request that might be presented to them for potential assistance, she added.

Dan Krause, president and CEO of State Farm General, then noted he would be the one who would be tasked with making such a request. “There has to be some sort of positive sign that State Farm General would be able to sustain itself from a capital position to support its risk profile….That’s the purpose of the interim rate request. That would give us that type of a positive sign, both to the rating agencies and to any potential investors, including State Farm Mutual….

That’s the emergency basis of this—because it would help, at least, me [in] building a case to go to the Mutual board to ask for consideration,” Krause said.

Later Lara asked again to clarify his understanding: An approval would “help you potentially make a successful request to the parent company for additional support?”

Krause replied: “It would allow a positive sign that would show that this is a market that we can compete, generate a return in, and stay in—and give us a chance for consideration for the parent company. Yes.”

Exposure vs. Capital

When the commissioner asked the executives to comment on the idea he’s heard from some constituents suggesting there is no benefit to consumers—that the rate increase is just a step in a financial bailout of State Farm General—Schwamberger ultimately said, “The only other thing that we could do without rate and without the ability to increase capital, is to substantially reduce exposure.”

“Any other actions aren’t going to be enough…to prevent the unfortunate situation that could arise should we not have positive signs about the prospective ability to be self-sustaining,” the CFO told Lara.

“Meaning, you would continue to non-renew or have to cancel policies?” Lara asked.

“At the end of the day, yes, sir. To the degree you cannot be self-sustaining and you don’t have viability and the capital to stand behind promises, [then] we’re left with no other alternative,” Schwamberger responded.

Asked about the potential to pause non-renewals, Schwamberger said the “short-term answer to that is no,” explaining that it takes time to get rate and grow. “[G]iven our current exposure and where we are, we would not be in a position to fiscally and responsibly starting to regrow within the California market just because of this rate in the very near term,” he said, according to the transcript.

Both Schwamberger and Krause talked about State Farm’s desire to remain in California, however.

“We look forward to some of the reforms,” Schwamberger said, referring to the department’s “Sustainable Insurance Strategy” reforms, which include allowing insurers to include the cost of reinsurance and to use forward-looking catastrophe models for provisions included in rate filing indications.

“We’ve been here for almost 100 years,” added Kraise. “We want to be here for 100 more, but we’ve got to be able to have this—for State Farm General to survive.”

Topics Trends Auto Profit Loss Underwriting

Was this article valuable?

Here are more articles you may enjoy.

New Jersey E-Bike Registration, Insurance Requirements Now in Effect

New Jersey E-Bike Registration, Insurance Requirements Now in Effect  FDA Walks Back Positive Lab Test in Lettuce Cyclospora Outbreak

FDA Walks Back Positive Lab Test in Lettuce Cyclospora Outbreak  Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal

Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal