While competition in personal auto insurance is rising to levels high enough to dent customer retention at GEICO, a giant mutual insurer and a reciprocal exchange have both tapped into a customer-friendly option unavailable to large stock insurers.

State Farm and USAA recently announced multibillion-dollar policyholder dividends that are “historically large” for the industry and the companies, S&P GMI noted in a research note this week. “These dividends, unique to mutual and reciprocal exchange business models, aim to enhance customer retention amid rising competition,” S&P GMI said.

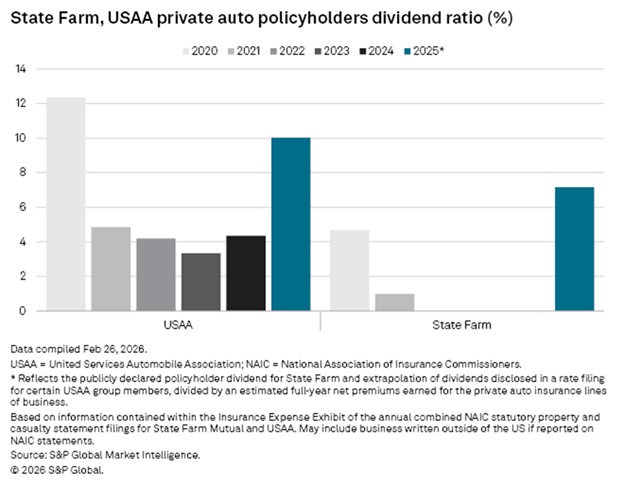

State Farm is set to return $5 billion to policyholders via dividends, the insurer announced last week. That represents 7.2% of State Farm’s estimated 2025 private auto net premiums earned of $69.4 billion.

At USAA, roughly $4 billion of dividends going out to members in 2025 represented a higher percentage of the military insurer’s auto earned premiums—nearly 10%, according to S&P GMI’s calculations.

At 7.2% of premiums, State Farm’s latest dividend marks a significant increase from the 4.7% dividend rate in 2020, S&P GMI said, offering a graph (shown above) that shows little or no dividends in the intervening years, when State Farm suffered large underwriting losses. The 2020 amount included COVID-19-related refunds, S&P GMI said.

USAA announced financial rewards of about $3.8 billion in 2025, with specific allocations detailed in a filing with the New York State Department of Financial Services, S&P GMI said, noting that this included dividends from USAA Casualty Insurance Co., Garrison Property & Casualty Insurance Co., and USAA General Indemnity Co.

The graph accompanying the S&P GMI report (and shown above) reveals that USAA’s dividends, on a percentage of premiums basis, exceeded the 10% of 2025 back in 2020 while remaining below 6% for 2021-2024.

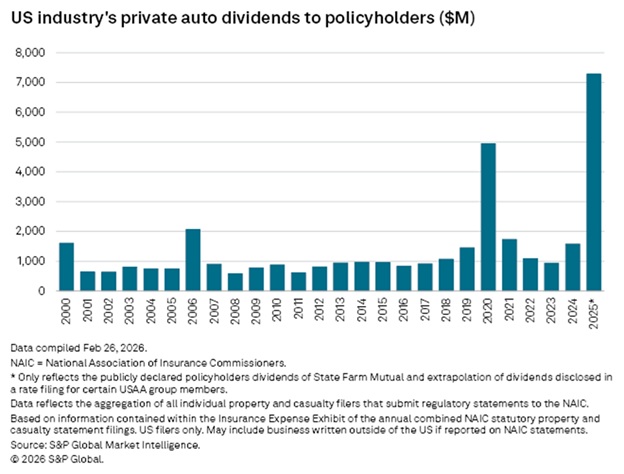

Together, the two companies’ dividends put the dollar-level of industry dividends at a record high for this century, S&P GMI showed in the graph below.

“This record amount in financial rewards is possible because of USAA’s financial discipline, which ensures the Association remains financially sound while continuing to deliver value to members. It is also a result of proactive steps USAA and members have taken to prevent losses,” USAA said in a December statement.

“Ensuring our members benefit from our financial strength is critical,” USAA Chief Executive Officer Juan Andrade said in the same statement, which revealed that USAA has also implemented auto insurance rate changes that “have been lower on average than competitors and the broader industry.” According to USAA, members saved an average of $100 annually per policy.

“Rates are expected to continue to stabilize in 2026,” USAA said, noting, however, the variation in rates that can occur as a result of claims trends, state trends and a members’ driving record.

Since last week, when State Farm announced $1.5 billion in underwriting profit across all lines for 2025, and the $5 billion dividend, the top of the largest auto insurer’s website has featured a banner announcing the dividend news with an exclamation point in white type on a black background. The website banner also reports that distributions of one-time cash payments to qualifying customers of more than 49 million insured State Farm Mutual vehicles will start this summer.

“The good news comes on the heels of an average of 10% lower auto rates in most states in 2025,” the banner says.

More specifically, “downward trending auto repair costs and frequency of collisions in 2025 have allowed State Farm Mutual to lower auto rates in 40 states in recent months,” State Farm said in a media statement, noting that the 10% average drop in those states represented aggregate premium savings of $4.6 billion for State Farm customers.

“This dividend is possible due to State Farm Mutual’s financial strength and a stronger-than-expected underwriting performance, which has been reported industrywide,” State Farm said in a media statement about the dividend. “As a mutual company, State Farm is uniquely positioned to provide value directly to customers rather than shareholders,” the statement said, also indicating that average dividend payments would be $100 per vehicle (varying by state and premiums paid).

“As a mutual company with a customer-first focus, State Farm Mutual is able to provide value directly to our customers while maintaining financial strength to keep our promises in the future, said Jon Farney, State Farm Mutual President and CEO.

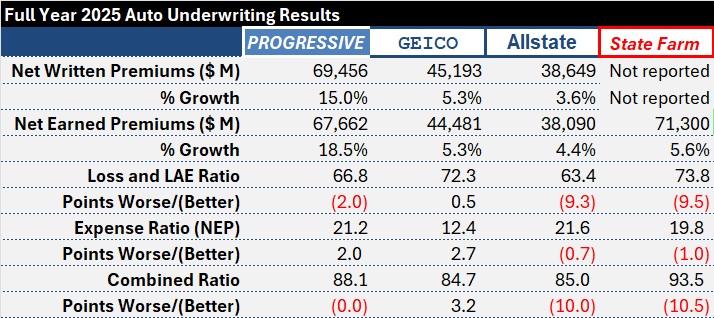

For the full year, the pre-dividend 2025 auto combined ratio of roughly 94 was more than 10 points lower than State Farm’s 2024 auto combined ratio of 104.

At Berkshire Hathaway, GEICO’s 2025 combined ratio was nearly 10 points better than State Farm’s, but also 3 points worse than GEICO’s 2024 combined ratio,

CEO Greg Abel had more sobering news about auto insurance for shareholders in a letter he penned for the conglomerate’s annual report. “GEICO’s broad rate increases in recent years have restored margins but come at the cost of lower retention,” Abel wrote in one of his introductory remarks on P/C insurance performance.

“Competitors’ rate reductions may extend that pressure into 2026.”

“The GEICO team remains focused on pricing risks correctly for both existing and new customers. Restoring retention while maintaining underwriting discipline will take time,” he advised.

Separately, Jess Merten, President, Property-Liability of competitor Allstate, also addressed competitive conditions during a presentation at the Raymond James 47th Annual Institutional Investors Conference on Monday. Merten also described a customer retention effort at his company known as the SAVE program.

“Certainly, the environment has gotten more competitive. And I think every [auto insurer] is looking to lower rates in one way or another,” he stated.

“We started last year with our SAVE program, which again saved millions of customers more than 5%. And we’re continuing to do that into 2026,” Merten said.

“We all have record profits,” he said, referring to the broader auto insurance landscape. “And, we are able to then reinvest those into affordability initiatives,” he added, referring to Allstate in particular.

(Editor’s Note: Unlike competitors in the auto insurance sector, Kemper reported worse underwriting results in 2025. Kemper executives explained the results with reference to the insurer’s high concentration in California where minimum liability insurance limits significanly increased last year.)

Earlier in the presentation, Merten said that Allstate reduced premium for 7.8 million customers through SAVE, which stands for Show Allstate Customers Value Everyday and essentially refers to a program of enhanced renewal reviews with customers aimed at adjusting coverages, identifying available discounts and ensuring customers are matched with the most cost-effective protection. “These targeted adjustments reduced premium by an average of 17% for customers who participated in 2025,” he said, also describing a new set of affordable products—referred to as ASC or “Affordable, Simple and Connected”—for which Allstate reduced auto insurance rates by an average of 9% in 32 states last year.

Related: Allstate: How Can You Save on Auto Insurance?; Allstate CEO Wilson Takes on Affordability Issue During Earnings Call

Merten also reported that declines in the underlying drivers of auto insurance loss costs have been declining, fueling a more competitive environment.

“In general, I think you find that it’s a competitive environment, more so than it’s been in recent years…It’s not like this is a new situation.” Auto and home insurance always have periods of competition. “Competitors come. Competitors go,” he said.

Merten believes Allstate is well-positioned to compete with broad distribution (through Allstate agents, independent agents and direct) and covering a risk spectrum that goes all the way from high-risk drivers to standard and preferred.

Last year, Allstate reported a combined ratio of 85 for auto insurance, 10 points better than 2024. The improvement was similar to the improvement reported by State Farm, but State Farm started at a much higher level—seeing its combined ratio come down to 94 in 2025 from 104 in 2024.

Like State Farm and GEICO, Allstate reported single-digit premium growth last year. Another publicly traded stock insurer, Progressive reported double-digit premium growth and a combined ratio of 88 for the year.

Was this article valuable?

Here are more articles you may enjoy.

Company at Center of Cyclospora Outbreak Complained to White House, Source Says

Company at Center of Cyclospora Outbreak Complained to White House, Source Says  Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers

Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers  NYC Halts Construction at 222 Broadway Office-to-Residence Tower

NYC Halts Construction at 222 Broadway Office-to-Residence Tower  CBIZ Brokerage to Be Spun Off, Backed by Private Equity, After $5B Grant Thornton Deal

CBIZ Brokerage to Be Spun Off, Backed by Private Equity, After $5B Grant Thornton Deal