Casualty claims are becoming more expensive at a faster rate, but medical professional liability stands out as one casualty line where compounding factors are turning severity deterioration into a heightened risk.

According to an S&P Global Market Intelligence report, written by Husain Rupawala, Tim Zawacki and Jason Woleben, medical professional liability “stands out as the most severity-pressured line in casualty insurance, with the highest figure across all lines.”

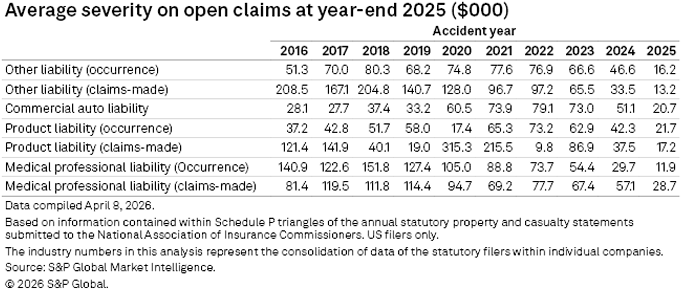

While severity steps down as claims mature and paid amounts reduce outstanding balances, the authors note such “moderation in newer years” primarily reflects claim immaturity rather than genuine improvement in underlying loss costs.

Medical professional liability occurrence reached $151,768 per open claim in accident year 2018, which represents the highest severity figure across all casualty insurance lines before moderating in more recent years, a typical trend for newer claims where cost pressures continue to emerge and mature.

The report’s authors also state that the drivers behind medical professional liability’s severity trend can differ from other lines of casualty.

“Third-party litigation funding has imposed substantial and rising cost burdens on insurers by lengthening litigation timelines and raising settlement targets, while attorney advertising has further intensified the environment and nuclear verdict benchmarks have increased, with median awards for major cases more than doubling in 2025,” the report said.

The report analyzed data from the National Practitioner Data bank, which found that payments of $500,000 or more accounted for 36.5% of total medical malpractice payments in 2024 when measured in real 2025 dollars, marking a new high for the line.

Medical professional liability claim severity varies significantly by state due to legal environments and the presence or absence of caps on noneconomic damages with New Mexico being one of the most difficult markets, the report noted. New Mexico posted 2025 direct incurred loss and defense and cost containment expense ratio of 128.8%, versus a US aggregate of 75.9%. Other high-stress jurisdictions include Utah at 143.8% and South Carolina at 125.7%, the report said.

Overall, S&P estimates that the medical professional liability business generated a calendar-year combined ratio excluding policyholder dividends in excess of 105% in 2025 for the fifth time in the past eight years.

Topics Trends

Was this article valuable?

Here are more articles you may enjoy.

Viewpoint: The AI Ransomware That Couldn’t Get Paid

Viewpoint: The AI Ransomware That Couldn’t Get Paid  Rhine Rises After Rain, but Low Levels Continue to Hinder Shipping

Rhine Rises After Rain, but Low Levels Continue to Hinder Shipping  One Weather Firm Warns New England Could See Big Hurricane This Season

One Weather Firm Warns New England Could See Big Hurricane This Season  FDA Walks Back Positive Lab Test in Lettuce Cyclospora Outbreak

FDA Walks Back Positive Lab Test in Lettuce Cyclospora Outbreak