Maybe it’s the result of a softer market.

Or maybe deliberate carrier investments in agency relationships are paying off.

First Connect Chief Executive Officer Aviad Pinkovezky tossed out the two possibilities to explain the markedly improved picture of agents’ ability to find capacity, understand carrier appetites, and receive timely quotes this year in an introduction to First Connect’s “2026 State of the Industry Report.”

According to the report, published in late June:

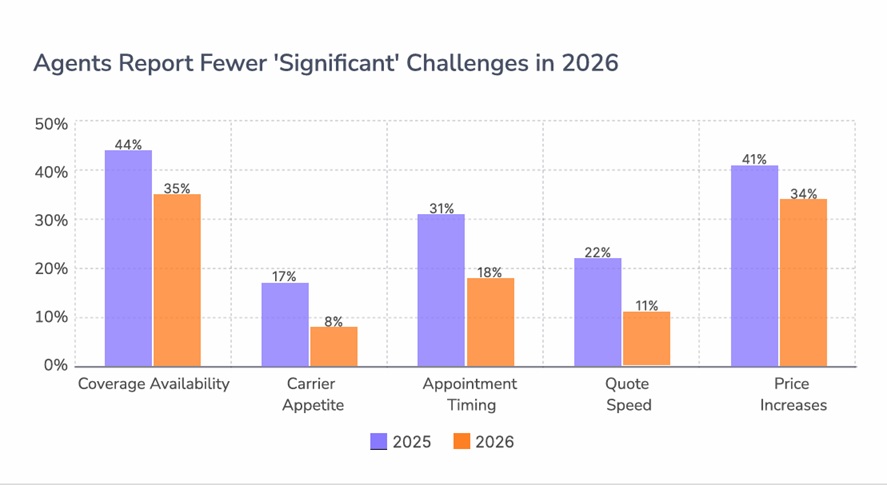

- Roughly one-third of agents surveyed (35%) reported “significant challenges” with coverage availability in 2026.

- Only 8% report “significant” struggles to understand carrier appetites.

- Just 11% said quote speed is a “significant” challenge.

Contrast that to First Connect’s prior “2025 State of the Industry Report,” when 86% of agents said they had faced product availability challenges—with 44% reporting “significant” availability challenges—and 17% reporting “significant” problems with carrier appetite clarity.

Related 2025 article: Agents Struggle to Find Capacity, Meet Customer Timing Expectations: Survey

“These are not marginal shifts. They are the strongest signal we have seen that the relationship between agents and carriers is moving away from transitional friction toward operational partnership,” Pinkovezky wrote in his message introducing the report, referring to survey results indicating that reports of “significant” challenges dropped by 50% or more.

First Connect is an insurance marketplace helping independent agencies compete more effectively. The company connects agents with more than 150 insurance carriers and MGAs across home, auto, commercial, and life from a single platform. The 238 agents surveyed for the State of the Industry report are all from First Connect agencies. First Connect also surveyed 44 of its carrier and MGA partners for the report.

“Much is due to the softening of the market, where we’re seeing carriers writing more and appointing more agents. But this broadening appetite is sustained by recent leaps in coverage and technology,” Pinkovezky wrote introducing the improved survey results. “Agents have new tools. Carriers have new posture. The two sides are starting to meet in the middle.”

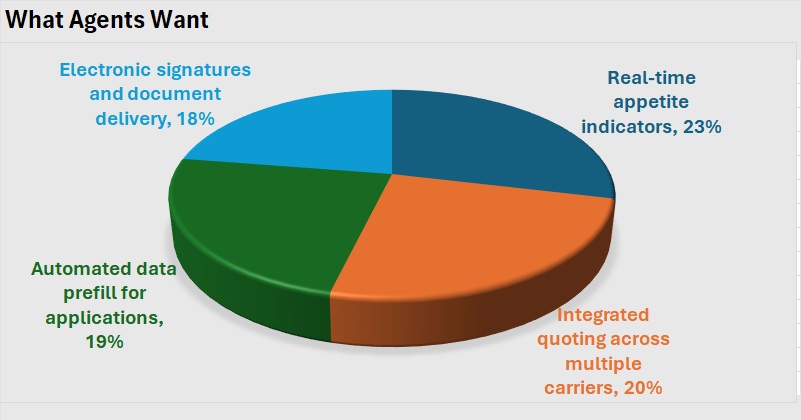

One survey question First Connect posed to agents reveals agents’ wish lists concerning technology that would most strengthen their abilities to serve customers. The responses, summarized in the chart below, haven’t moved much since 2025, First Connect reports, listing real-time appetite indicators, integrated quoting across multiple carriers, automated prefill for applications, and electronic signatures and document delivery as the agents’ top four priorities.

“The consistency year-over-year is itself the finding. When the priority list does not move, it tells us where the industry’s investment should concentrate,” the First Connect report says.

Asked about their use of AI for the first time this year, the 2026 survey revealed that while more than half of the agents said they are optimistic about the impact of AI on the insurance industry, just 35% of agents use AI on a daily basis—only trusting AI tools for collecting basic customer and risk information, scheduling appointments, and checking payment status or billing history.

“These are not marginal shifts. They are the strongest signal we have seen that the relationship between agents and carriers is moving away from transitional friction toward operational partnership.”

Aviad Pinkovezky, First Connect

“These are not marginal shifts. They are the strongest signal we have seen that the relationship between agents and carriers is moving away from transitional friction toward operational partnership.”

Aviad Pinkovezky, First Connect

In addition, there was no activity that more than 17% of agents said they would use AI to complete, the report says. Offering a perspective on agent’s caution with AI, the authors of the First Connect report called agents’ selectivity “rational.”

“Today’s AI tools still produce confident-but-incorrect outputs often enough that handing them customer-facing work carries real risk,” the report says.

As for the biggest challenge facing agents today, according to the report, it’s direct-to-consumer competition, not competition from other agents. Forty-three percent of agents identified D2C as the “single biggest factor reshaping [the agency] distribution channel today—up from 37% last year. “Although D2C is hardly a new concept, the increasing sophistication and capability of AI is increasing the breadth of coverage available to direct customers, which is no longer restricted to the simplest lines,” Pinkovezky wrote in his introductory comments.

While factors like “the shift to E&S” and “rising customer expectations for digital experiences” were cited less often as channel-altering factors (by 11% and 14% of agents surveyed, respectively), the percentage of agents identifying the “digital experiences” factor jumped up to 14% from just 8% last year.

Carriers, on the other hand, identified digital expectations as the No. 1 pressure on their market, with 30% selecting that factor among choices offered by First Connect (including the shift to E&S, selected by just 16%).

How to Grow: What Carriers Are Missing

The carrier part of the report also summarizes responses to questions about agency appointment time frames, strategies to partner with agents aligned with carrier business goals, tools that carriers have integrated into agency workflows and market intelligence. On the tools question, 38% of carriers indicated they’ve built automated underwriting guidance and 29%, real-time appetite indicators—the two most popular tools.

On the market intelligence question, the writers of the First Connect are critical of carriers, highlighting a disconnect between the percentage of carriers indicating they have a “very good” or “excellent” understanding of the market (roughly two-thirds) and those that look beyond internal metrics to understand the market (only about one-quarter).

First Connect notes that while internal metrics like conversion rates, loss ratios and premium growth “reveal what’s happening inside a carrier’s own book of business,” they don’t show “where agents are placing business elsewhere, how competitive dynamics are shifting across channels, or where new growth opportunities are emerging before someone else finds them first.”

“The most common misconception in our industry is that commission flow is the most important data a carrier has on its distribution… Commission tells you what was placed [not] what should have been placed, didn’t get placed because of friction, or where the agent’s effective book is actually shifting,” Pinkovezky wrote, advocating carrier use of third-party market intelligence.

Unsurprisingly, he specifically referred to the nuances of First Connect’s “privileged view of the marketplace,” which he said gives a full picture of agent behavior across the ecosystem, including data points like which carriers an agent quotes first and what agents are writing beyond a carrier’s product.

“The carriers who grow most consistently are not the ones with the largest appetite or the most aggressive pricing. They are the ones who respond fastest to agent signal,” the report text says.

Was this article valuable?

Here are more articles you may enjoy.

Walmart Removes Four Taylor Farms Salads as Recalls Spread

Walmart Removes Four Taylor Farms Salads as Recalls Spread  US P/C Industry Books Best Result in a Decade but Not All Lines Enjoy Success

US P/C Industry Books Best Result in a Decade but Not All Lines Enjoy Success  Lloyd’s of London Says Former CEO Neal Breached Compliance Rules

Lloyd’s of London Says Former CEO Neal Breached Compliance Rules  Husband and Wife Insurance Brokers Sentenced for Fraud Scheme

Husband and Wife Insurance Brokers Sentenced for Fraud Scheme