After years of warnings that the Florida property insurance market was heading towards an availability crisis, many in the industry say the moment of reckoning has arrived. They blame unchecked claims litigation from non-catastrophe water losses and rising reinsurance rates that have severely strained the financials of Florida insurers.

The situation has gone from bad to worse for Florida domestic insurance carriers this year, which together cover most of the state’s homeowners market.

Nearly 60 carriers suffered a combined $701 million in losses and $351 million in negative income for all of 2019, according to Guy Carpenter. In just the first half of 2020, the companies lost more than a half billion ($501 million) in underwriting losses and $227 million of negative net income. Third quarter results are expected to show further deterioration. Guy Carpenter’s data cited an average net combined ratio for 2019 of 111 percent that climbed to 129 percent in the second quarter of 2020 for these companies.

“If we’re not in a crisis, I don’t know what we’re in,” said Kyle Ulrich, president and CEO of the Florida Association of Insurance Agents. “Those numbers … just simply are not sustainable.”

As a result, carriers have been steadily raising rates this year and this trend isn’t expected to slow down any time soon. Companies are requesting and the Florida regulator is approving substantial rate increases – some over 30% – along with taking steps to limit their exposures and protect their books of business.

The vast majority of Florida insurers have filed multiple rate increases this year for just under the 15% threshold that requires a rate hearing by the Florida Office of Insurance Regulation. Since August, four companies – Capitol Preferred Insurance Co., Southern Fidelity Insurance Co., First Community Insurance Co. and Centauri Specialty Insurance Co. – have participated in rate hearings for rate increase requests ranging from 25% to just below 40%.

John Rollins, former principal and consulting actuary with Milliman and now chief financial officer at Olympus Insurance, told the Colodny Fass/Aon Florida Insurance Summit in September that Florida homeowners insurers filed at least 79 rate increases through the second and third quarter of 2020.

The cumulative impact of these filings averages a 9.3% increase equaling $7.4 billion in homeowners premium, not including dwelling fire, Rollins said. The total premium base in Florida is about $11 billion, Rollins noted, “so essentially you’ve had 70 percent of the market go to the well in the last five and a half months and take a rate increase of 9.3%.”

“Consumers are feeling this pain and as the renewal cycles roll in over the next 12 months, these 79-plus [insurer] rate filings … are really going to hit,” Rollins said.

How did the market get to this point? Over the last several years, insurers have consistently cited evidence of excessive first- and third-party litigation from non-catastrophe water damage losses across the state. While the state also experienced a number of major catastrophes, the industry says the frequency and severity of lawsuits on non-cat losses has been unprecedented.

Barry Gilway, president and CEO of Florida’s Citizens Property Insurance Corp., said litigation for the state-run insurer of last resort has increased in some parts of Florida by 500% in the last four years.

“Litigation is out of control in the state and until we do something about the overall litigation issues and the firms drumming up litigation, then rates are not going to stabilize,” Gilway said at the Colodny Fass/Aon event.

Overall litigation rates for third party assignment of benefits (AOB) lawsuits have dropped from what they were a few years ago thanks to reforms passed in 2019, but carriers say they are still being hit by a considerable amount of first party litigation and excessive attorney fees. They point the finger at the state’s one-way attorney fee statute and the contingency fee multiplier for incentivizing inflated lawsuits against insurers.

“We have seen a continued increase in litigation whereas specific AOB claims have decreased slightly,” Jesse Rehburg, actuarial manager for Capitol Preferred, told OIR regulators at an August rate hearing for its filing for a 26.2% increase on nearly 30,000 policies. It also sought a 31.1% increase on more than 46,000 policies for its Southern Fidelity Insurance affiliate.

Capitol Preferred said non-catastrophe water loss claims and litigation show no signs of slowing. Rehberg noted 30% of its filed claims are represented by attorneys, and costs of represented claims are more than 100% higher than non-represented claims.

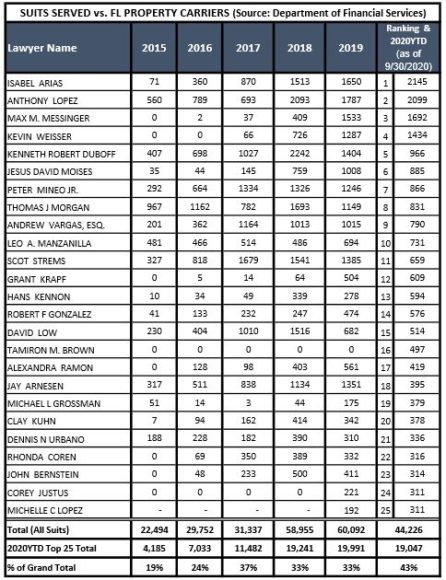

In analyzing data from the Florida Department of Financial Services, industry consultant and president of Johnson Strategies Scott Johnson noted in a recent blog that 25 attorneys have filed nearly 20,000 lawsuits against insurers through the first six months of 2020, accounting for 43% of the state’s total property lawsuits so far this year. The total number of suits filed against 56 property carriers since 2015 totals 246,856.

Florida-based litigation management and analytics software company CaseGlide’s data showed that around 4,000 lawsuits per month were filed against the top 15 to 20 Florida property carriers during June, July and August of this year. The company attributed some of that to the rush to get claims in before the September three-year deadline for Hurricane Irma. Litigated claims increased again in September to nearly 5,000, up 7% from August and 28% from September 2019.

Reinsurers have responded to the Florida market’s increasing losses and exposure with the highest spike in renewal rates since 2006, Rollins said. Reinsurance rate increases on this year’s renewals averaged 25% to 30% with some companies seeing as much as a 50% increase.

The reinsurance increases have put Florida insurers in the position where they simply can’t take on more risk, Ulrich said.

“Given what their re-insurance allows them to do and write, based on some storms this summer and the exposure that they have seen in claims, they just don’t have the ability to write any more business,” he said.

Agents have reported “pretty restrictive” new underwriting guidelines by carriers, including limits on new business to homes 2010 and newer, Ulrich said. Several carriers have told their agents that they will no longer accept any new business and instead will just quote renewals.

“They will be renewing the business that’s on the books, and agents can buy business that has already been quoted,” Ulrich said. “But, going forward, they’re not writing any new business.”

At Citizens June board of governors meeting, Gilway said decreased reinsurance capacity has forced companies to restructure their portfolios. Six major companies publicly announced they were shutting down of all new business in Tri-County, Central Western Counties, and more recently, the SOLO counties of Seminole, Orange, Lake and Osceola.

“These measures are harmful and significantly impactful to consumers in the form of higher insurance rates, reduced coverage and lack of availability,” Florida Insurance Consumer Advocate Tasha Carter said in an e-mail to Insurance Journal. “As policies are restructured to include tighter underwriting measures, consumers are paying higher insurance premiums for reduced coverage. Essentially, consumers are paying more for less and that’s problematic.”

Losses so far in 2020 are not going to help the situation, noted Robert Warren, client services manager for Demotech, at the Colodny Fass/Aon event. Demotech, which rates more than 40 Florida domestics and threatened downgrades to a dozen early this year before affirming them, projects a $730 million underwriting loss for those companies – almost double the amount of 2019 – based on data it has seen of weather losses, reinsurance costs and the investment in the replacement of capital the companies will need to make before the end of the year.

That figure does not include losses to carriers from Hurricane Delta, he said, which despite being a mainly Louisiana event could still impact Florida insurers that have diversified and expanded into other states.

“It’s been a significant year for storm events – this is a frequency issue as well as severity,” Warren said.

Companies are already taking steps to replace lost capital, Warren said, but doing so could be problematic for those that do so by taking on debt.

“[Demotech] need[s] to be very aware of what that capital source is,” he said.

Warren said Demotech believes carriers are “doing the right things at the right time for the right reasons,” and expects those that need capital to keep their financial stability rating (FSR) from Demotech will be able to get it.

“Right now, Demotech’s expectation is they will meet our requirements to maintain or be considered to maintain the current FSR,” Warren said.

Ulrich warned, however, that outside capital that has consistently invested in Florida-based carriers, may be close to the end of financing Florida’s domestic homeowners’ market.

“When we get to that point where folks that have invested in this market make the decision that they’re no longer willing to invest in this market, and it becomes more difficult for companies to find and attract capital, and their surplus is going down at the rate that it is now, that becomes a crisis situation,” he said.

Market Impact – The Growth of Citizens

With rates spiking statewide and companies pulling back capacity, many insureds have had no other choice but to turn to the insurer of last resort, Citizens. Its rates are capped on a glide path of 10% per year, meaning the company cannot raise them more than that, thus making the residual insurer a competitive alternative to the current private market.

Citizens’ policyholder count stood at approximately 443,000 policies earlier this year with about $110 billion in exposure. At the September Citizens Board of Governors meeting, Gilway said Citizens is growing by 2,500 to 3,000 new customers per week on a net basis. Its new business increased from 7,770 policyholders to 17,691 per month over the past 12 months. Gilway said the increase in new business, combined with a significantly higher renewal rate of 90% this year compared to 83% last year, puts the company at an estimated policy count of 540,000 for year end 2020 and up to well over 640,000 next year.

“We grow and we shrink depending upon the overall profitability of the private market,” Gilway said at the Florida Insurance Summit. “When the private market is doing extremely well then Citizens shrinks. When the private market is really succumbing to some of the problems that we’re seeing … obviously we start to grow.”

The repopulation of Citizens could mean added costs for all Florida consumers. Florida law requires that Citizens levy assessments on most Florida policyholders if it experiences a deficit in its reserves in the wake of a major storm or series of storms. At its peak in 2011, Citizens had 1.5 million policies on its books – 23 percent of the Florida market – with exposure that topped $512 billion. In the event of a 1-in-100-year storm, Floridians were on the hook for $11.6 billion in assessments.

Thanks to depopulation efforts, the reinsurance market and catastrophe bonds, Citizens was able to eliminate assessments for Florida consumers in 2015.

“The growth of Citizens impacts the private market and shifts Citizens farther away from being the residual market carrier it was intended to be,” said Insurance Consumer Advocate Carter.

Florida State Senator Jeff Brandes, who sits on the Banking & Insurance Committee, said one of his primary legislative goals over the next two years “is to put the Florida insurance market on a sustainable path.”

To that end, Brandes worked with Citizens to commission an exposure reduction study on how the insurer could reduce its overall exposure and financial impact on the state. That study is currently being performed by analysts at Florida State University and is expected to be complete by December. Brandes said he requested the study because “the writing was on the wall.”

“Anybody who is shocked that Citizens is starting to grow hasn’t been paying attention because we’ve been telling them for frankly months, likely years,” Brandes said in an interview. “We recognize that Citizens is required to only raise rates 10% a year. And often they’re losing money in certain markets and they’re being subsidized, those homeowners are being subsidized by taxpayers.”

Gilway said Citizens hopes the FSU Study will provide insight as to why litigation is increasing, why severity is increasing, and into the roles of public adjusters and loss consultants, and more. He said he expects there will also be legislative recommendations along with changes in the Citizens plan of operations.

Brandes has other ideas for how to keep Citizens a residual market, including transitioning its rate structure to what he calls a “vintage model.” That would involve bringing in new policies at an actuarially indicated rate while allowing existing customers to stay at the current rate cap. When policyholders renew, they would stay at the 10% glide path and new policyholders would reset for that vintage, he said.

Brandes asked Gilway in June to request the board consider implementing this change.

“Application of actuarially sound rates for new Citizens customers will bring Citizens into compliance with the statutory directive that its rates be actuarially sound and maintain Citizens as the insurer of last resort,” he wrote in a letter to Gilway.

The action is slated to be discussed at the December board meeting, Brandes said. A Citizens spokesperson said actuaries will present information to the board in response to Brandes’ letter but it is unclear if any action will be taken at that time.

“That seems to be the only sustainable model that will work for Citizens for the long term, given the challenge of adjusting the rate cap in the political environment,” Brandes said.

Gilway said he thinks much of the business coming into Citizens right now has more to do with capacity in the market than rates. “No one’s quoting. Period,” he said at the Colodny Fass/Aon event.

But in studies comparing Citizens to the private market, Citizens rate cap makes it too competitive with the private market, and that’s a problem long term, Gilway said.

“The more we get out of whack with the private market … I believe it will be the reason more growth comes into Citizens and that’s not what we want,” he said. “Our goal is to find a policyholder the best coverage at the best price in the private marketplace and get Citizens back down to the point where we have a reasonable residual market position.”

This is the first article in a two-part series examining the Florida insurance market. Read Part Two: Florida Property Insurance Market Inches Closer to Crisis – Part 2

Related:

- Hurricane Irma’s ‘Last Gasp’: 3-Year Claims Deadline Put to the Test

- Judge Finds Strems Guilty of Misconduct; Advises 2-Year Suspension, Probation

- Florida Supreme Court Suspends Attorney Behind Thousands of Insurer Lawsuits

- How Florida’s Strained Insurance Market is Facing COVID-19, Hurricane Season

- Florida Market Study Will Evaluate Exposures, Strategies for Citizens Property Insurance

- Demotech Reveals Florida Insurer Ratings, Says Market ‘Most Difficult’ in U.S.

- Demotech Affirms Ratings of 37 Florida Insurers; Still Reviewing Others

- Florida Carriers Seek Staggering Rate Increases Amid Market Turmoil

- HCI to Acquire Policies of Florida’s Anchor P&C; Weston to Acquire Anchor Specialty

- More Than a Dozen Florida Insurers Facing Ratings Downgrades

Topics Lawsuits Trends Catastrophe Carriers Florida Agencies Claims Profit Loss Property Reinsurance Homeowners Aon Market

Was this article valuable?

Here are more articles you may enjoy.

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed  Bill to Curb Staged Accidents Introduced in Senate

Bill to Curb Staged Accidents Introduced in Senate  As US Residential Solar Industry Craters, Florida Bucks Trend

As US Residential Solar Industry Craters, Florida Bucks Trend  London Broker Howden Plots Giant Capital Raise on IPO Path

London Broker Howden Plots Giant Capital Raise on IPO Path