New information from Florida’s insurance regulator paints a stark picture of the extent of litigation facing the state’s domestic insurers. The information comes as numerous stakeholders push for legislative reforms to address the litigation issue they blame for fueling the current insurance market crisis.

According to National Association of Insurance Commissioners (NAIC) data mined by the Florida Office of Insurance Regulation, while Florida homeowners insurance claims accounted for just over 8% of all homeowners claims opened by U.S. insurers in 2019, homeowners insurance lawsuits in Florida accounted for more than 76% of all litigation against insurers nationwide.

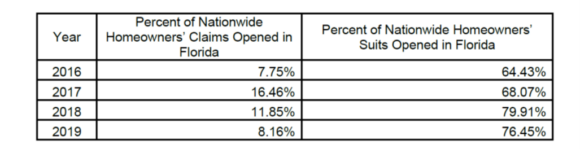

And those results are not an anomaly just for that year, the report says.

Florida Insurance Commissioner David Altmaier alerted Florida House Commerce Committee Chair Blaise Ingoglia to the new data gathered by his office from the NAIC in a letter last week.

“Litigation trends in Florida have been consistently many times higher than any other state,” Altmaier wrote, citing NAIC data that shows Florida lawsuits rose steadily from 64.4% of all nationwide homeowners lawsuits in 2016, to 68% in 2017, to 79.9% in 2018 and 76.4% in 2019 (see chart).

OIR pulled the information from NAIC’s Market Conduct Annual Statement (MCAS) Data Call to further provide information to lawmakers on litigation trends in the Florida insurance market. MCAS is a regulatory tool developed in 2002 by state insurance regulators to collect information from insurers regarding claims and underwriting. In 2019, over 750 homeowners’ insurance companies reported data via MCAS using uniform definitions and reporting requirements across all states.

Altmaier, who also currently serves as NAIC president, said OIR included MCAS data of Florida’s ratio of suits opened to total claims closed and a ratio of suits opened to claims closed without payment as well, to allow OIR to “observe trends in the context of other states.”

For 2019, Florida trended with the national average when comparing the number of claims closed without payment to total claims closed. However, Altmaier noted, Florida’s ratio of suits opened to claims closed without payment was eight times higher at nearly 28% than the next highest state, Connecticut, which had a ratio of 3.4% of suits opened to claims closed without payment.

OIR analyzed the data between Florida and the other states to examine the disparity and validity of its methodology and results with MCAS staff at the NAIC, Altmaier said. It also analyzed the litigation to claims ratio of insurers operating in Florida – because the state’s insurance market is so heavily reliant on domestic companies – and other states to see if there was a pattern of these insurers experiencing litigation higher than their peers in other states, which he said could be an indicator of claims handling issues. But, Atlmaier noted, OIR did not detect any such systemic pattern that would explain the disparity.

“While we continue to explore these and other possibilities to explain the disparity, OIR does not have a readily available explanation for Florida’s outlier status other than to simply state that Florida is experiencing far more claims-related litigation than the other 47 reporting states,” Altmaier wrote.

In light of the new data, he urged the legislature to consider additional reform measures to help the state’s property market challenges, including:

- Reforming the state’s one-way attorney’s fee statute in a way that still allows policyholders to still file suit against their insurance company but removes the incentive for attorneys to file illegitimate claims. Altmaier said reforms like what were enacted in the 2019 AOB legislation “preserves important consumer protections, while providing a framework to ensure litigation brought against insurance companies is legitimate.”

- Addressing the ramifications of the decision regarding contingency fee multipliers by the Florida Supreme Court in the Joyce vs. FedNat (2017) case, which separates Florida from federal standards. Instead, legislation that codifies the adoption of “rare and exceptional” framework so contingency fee multipliers are only used in such cases could be effective at reducing the filing of meritless cases to receive a large attorney fee payout.

- Addressing the ramifications of the Sebo vs. American Home Assurance (2016) Florida Supreme Court decision regarding concurrent causation that OIR says has incentivized roof claim solicitations. Statutory language that specifically excludes “wear and tear” from concurrent causation could provide a disincentive for this behavior, while allowing consumers to keep replacement cost coverage for legitimate roof issues.

- Including provisions from legislation enacted in Texas in 2017 that broadens pre-suit notice and inspection requirements for property claims and addresses attorney’s fees.

“These solutions could substantially reduce the litigation associated with claims, bringing more certainty into Florida’s property insurance market,” Altmaier concluded. “Ultimately this will provide more stability in the market and more rate stability for consumers.”

Florida carriers lost more than $1.6 billion in 2020 thanks in part to excessive litigation, reinsurance costs and natural catastrophes. Companies are taking extreme steps to reduce their exposure in areas where there is high litigation rates or high reinsurance costs, including enacting coverage restrictions and increasing rates. OIR approved 105 rate changes, 90 of which were for rate increases, over the last year, with 55 of those for rate increases of more than 10%. Stakeholders have warned that without legislative reforms, rates will continue to increase and consumers may be unable to find coverage in the private market.

Altmaier’s letter to the Florida House Commerce Committee chair came days before the committee’s planned meeting today, April 14, where it will debate House Bill 305. That bill was formerly the companion bill of Senate Bill 76 that passed by the Florida Senate last week. The Senate bill is backed by the industry because they say it tackles many of the issues blamed for the current problems in the market, including excessive litigation and roofing claims.

However, HB 305 has changed drastically since it was introduced at the beginning of the current legislative session and many in the industry and others say it doesn’t go far enough in addressing the property market’s issues. Lawmakers will have to reach a compromise before either bill can become law.

Related:

- Citizens’ CEO: Florida Property Insurance Market is Shutting Down

- Florida Senate Passes Property Insurance Reform Bill

- Fate of Florida Insurance Reforms Uncertain as Lawmakers Weigh Industry-Backed Bills

- Insurance Agents on the Front Line of Florida’s Mounting Property Market Problems

- ‘Desperate’ Times: Stakeholders Urge Florida Lawmakers to Enact Insurance Reform

- Florida Legislative Session 2021: Insurance Bills to Watch

- Florida’s Property Insurance Market Is ‘Spiraling Towards Collapse’ Due to Litigation: Report

- Florida Legislature Weighs Options to Address Rising Homeowners Insurance Costs

- Florida Market Stabilization Critical to Reducing Citizens’ Exposure: Study

- Hurricane Irma’s ‘Last Gasp’: 3-Year Claims Deadline Put to the Test

- Florida Supreme Court Suspends Attorney Behind Thousands of Insurer Lawsuits

Was this article valuable?

Here are more articles you may enjoy.

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks  Majority of Small Business Are Underinsured as Other Expenses Prioritized

Majority of Small Business Are Underinsured as Other Expenses Prioritized  Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent  Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver