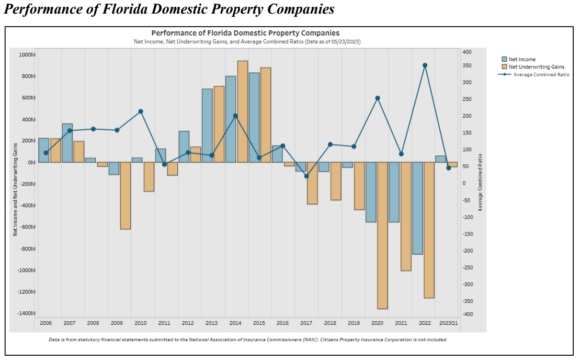

Florida’s beleaguered insurance industry may have turned a corner in 2023, with net income in the black for the first time since 2016 and much smaller underwriting losses than in recent years, according to state regulators’ latest market stability report.

But the data from the Office of Insurance Regulation also show that claims litigation, which dropped significantly late last year, has spiked again. And 2022 loss reserve development, showing the actual cost of claims compared to initial estimates, was $772 million higher than expected at the two-year look-back mark.

“These numbers reflect the high degree of uncertainty which exists in the property insurance market, which in turn impacts reinsurance capacity and reinsurance rates for insurers,” the July 1 report reads.

The latest report notes that loss reserves will rarely equal the ultimate cost of claims, but added that “it is also not expected that the ultimate cost of claims will be double or triple the estimated loss reserve.”

“It’s still a very treacherous market,” said Mark Friedlander, director of communications for the Insurance Information Institute. “We’re still seeing a lot of volatility.”

The OIR is required by law to collect data from insurers and other sources and produce the stability analysis every six months. The 23-page July report provided several insights into the state of Florida’s market, which has been considered distressed for the past several years but has been salved by a series of recent legislative actions designed to limit the staggering cost of claims litigation.

Who’s in Trouble?

Of Florida’s 110 or so property insurers, 18 were referred to OIR’s stability unit in the first half of 2023 and two were deemed shaky enough to warrant “enhanced monitoring.” The office declined to name the carriers on the watch list, noting that the names are protected by law. Otherwise, it could would be unfair to the insurers and could create a “run on the bank” scenario, former Florida regulator Lisa Miller said.

The numbers suggest a slight improvement in the industry’s overall health. In late 2022, 24 carriers were referred to OIR and six were designated for enhanced monitoring. A more telling picture may emerge in the next few weeks, when rating agencies, including Demotech, release new financial stability ratings for Florida-based insurers, Friedlander said.

A market conduct examination, required by Senate Bill 2A that was approved in December, found no insurers that were guilty of unfair trade practices, such as forcing policyholders to participate in the appraisal process before a claim can be settled.

Premium Increases Not so Steep?

While some recent news reports have said that Florida homeowners pay the highest premiums in the country – as much as $6,000 a year on average – the OIR collected data from Florida insurers that show the average annual premium is about $2,850 as of March 2023. That’s about $230 more than last year’s average.

But Friedlander pointed out that the OIR report shows average premium per county. Some counties include far fewer policies and fewer high-end properties than others. When the county averages are averaged together, that view may not provide an accurate snapshot for the state. The OIR data also include premiums paid by policyholders of the state-backed Citizens Property Insurance Corp., which has the largest market share but offers premiums far below many market-based insurers. The Insurance Information Institute’s recent premium estimate, based on polling of carriers and agents, does not include Citizens’ rates.

Still, the OIR report gives an indication of the relative cost of HO premiums. The highest average premiums were paid by residents in five south Florida counties, including Monroe County, home to the vulnerable Florida Keys, where the average premium in early 2023 reached almost $7,600. When those south Florida counties are left out of the tally, the average statewide premium falls to just $1,662, the OIR data indicate.

Claims, Policies

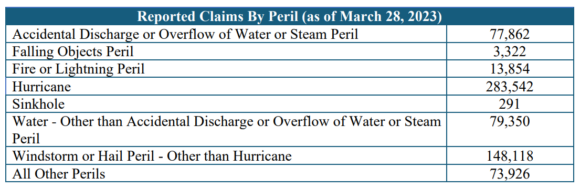

For the first time, the OIR report compiled claims for the year, per legislation approved in 2022. For the year 2022, Florida  insurers saw 678,986 personal and commercial claims. Almost 42% of those were hurricane claims. The second-highest category was non-hurricane windstorm or hail, at 22%.

insurers saw 678,986 personal and commercial claims. Almost 42% of those were hurricane claims. The second-highest category was non-hurricane windstorm or hail, at 22%.

The average indemnity on claims was $15,331 and the average loss adjustment expense was $2,156.

“As this is the first collection of the data, OIR continues clarify data with companies to ensure all other fields within the data call are consistent,” the report noted.

The number of homeowner policies in Florida for the first quarter of 2023 stood at just over 4 million. Citizens policies made up about 18% of those and continue to grow.

Litigation

The OIR’s January stability report caused some eyes to pop when it found that in 2021, Florida insurers paid more than $3 billion in defense cost and containment expenses, based on data from the National Association of Insurance Commissioners. In 2022, that figured dropped only slightly, to $2.95 billion.

Another indicator of the litigation burden is the number of lawsuits. The number of services of process, given when insureds file suit, dropped considerably after Senate Bill 76 took effect in 2021, the report found. That bill required plaintiffs to give advance notice of legal action, in hopes of allowing insurers to settle or avoid litigation. But in recent months, the numbers rose sharply, perhaps as plaintiff firms around the state rushed to file claims lawsuits before House Bill 837, the sweeping tort-reform measure, took effect.

Profits

Net income for Florida insurers, not including Citizens, rose to about $60 million for Q1 2023, a far cry from the industry’s net losses reported for all of 2022. That may be due in part to investment gains, but the combined ratio als dropped to less than zero for the first time since 2017. Underwriting losses shrank to about $50 million, compared to almost $340 million in losses for all of 2022.

Reinsurance

Based on a data call with carriers, the cost of reinsurance purchased for 2022 jumped by 52% over 2021 rates. Figures for 2023 won’t be finalized until August, the OIR said. But other industry reports have indicated that reinsurance prices climbed by another 50% at the June and July renewal dates this summer.

“In the simplest of terms, the greater the uncertainty that exists on future claims, the more reinsurers will tend to hedge their willingness to offer capacity, and the capacity that is available will cost more as a result,” the report noted, referring to loss reserve development.

Up Next

The OIR said it will continue to monitor the temperature of Florida-admitted insurance carriers, with the next stability report due out in January.

“As we continue to monitor the financial condition and operating results of regulated entities, OIR remains committed to ensuring consumers have access to a stable and competitive insurance market and utilizing the full extent of our regulatory authority to ensure policyholders are protected,” OIR Communications Director Samantha Bequer said in an email.

Topics Carriers Florida Profit Loss

Was this article valuable?

Here are more articles you may enjoy.

London Broker Howden Plots Giant Capital Raise on IPO Path

London Broker Howden Plots Giant Capital Raise on IPO Path  Q2 Global Commercial Insurance Rates Keep Dropping, Except for US Casualty

Q2 Global Commercial Insurance Rates Keep Dropping, Except for US Casualty  Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver  Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal

Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal