The head of one of the largest private flood insurance writers this week questioned an AM Best report that said private flood companies are failing to make significant inroads in America’s troubled flood market.

“From 2020 through 2022, private insurers wrote a growing portion of the overall flood market, but that growth stalled in 2023,” said AM Best in the report.

The market share for private flood writers has stagnated in the face of greater opportunities, the financial rating firm noted.

“Private flood insurers, which predominantly have written coverage for commercial insureds, have shown some willingness to accept flood risk, but the increase in take-up to date has been minimal.”

The growth of the private flood market is becoming increasingly important as parts of the country, particularly Florida and other Southeastern states, see more frequent hurricanes, the National Flood Insurance Program faces mounting debt levels, and some in Washington rattle sabers about cutting out the NFIP altogether, the report noted.

“However, without the NFIP, there would be a large void in the flood insurance market, which private flood insurers do not appear eager to fill at this moment,” reads the report, authored by Best analysts Christopher Graham, David Blades and Sridhar Manyem.

But Trevor Burgess, CEO of Neptune Flood, a managing general underwriter that writes on the paper of four carriers, took issue with the Best report’s assertions.

“The conclusions reached don’t reflect our experience as the industry leader,” Burgess said Monday in an email.

He noted that Neptune, based in St. Petersburg, Florida, has seen huge growth in recent years, from about 50,000 flood policies at the end of 2020 to more than 205,000 policies today.

It’s not clear if Burgess and AM Best are looking at the same data. A spokesman for AM Best said late Monday that the rating firm’s data on private flood insurance came from insurers’ annual statements filed with the NAIC, not from an National Association of Insurance Commissioners supplemental data call that Burgess may have been referring to. The data is considered accurate, AM Best noted.

Burgess argued that information reported by carriers to the NAIC in a data call has been the subject of some confusion..

The NAIC data call asked only for information on admitted private flood carriers, but most private flood is from excess and surplus lines, including coverage written through Neptune, Burgess said. Also, the NAIC data call asked insurers to exclude NFIP policies but “we can tell that some carriers” responded with NFIP policy information, he said.

Officials with Wright Flood, another significant writer of private flood policies in the U.S., declined to comment about AM Best’s report, as the company was preparing for the impact of Hurricane Milton in Florida.

The Best report gives other insight into the current state of flood insurance, just as thousands of homes and businesses in Florida, North Carolina and Tennessee struggle to recover from Hurricane Helene, which hit the region late last month with catastrophic amounts of rainfall. Most property owners had not purchased flood insurance before the storm.

The NFIP policy count has, in fact, declined in the last two years, partly due to higher premiums resulting from Risk Rating 2.0, a new federal approach designed to price risk more accurately, the report claims. Despite a statutory glidepath that caps NFIP premium increases to no more than 18% per year, “the initial pricing increases have been too much for some policyholders to bear,” the Best report said.

As NFIP premiums rise, however, that should make private flood carriers’ rates more competitive. But it’s uncertain if private insurers have an appetite for additional flood risk, even as risks accelerate.

Helene and now Hurricane Milton, expected to hit the west coast of Florida Wednesday night, could exacerbate NFIP’s $21 billion debt, the report noted. Historically, the federal flood program has been effective at covering losses from river flooding, but has seen heavy losses from coastal storm surge and from flash flooding, the Best report noted.

Last month, the NFIP was temporarily reauthorized by Congress, through Dec. 20, likely setting up another debate about the wisdom of keeping the program. The Heritage Foundation’s Project 2025 has called for an end to the federal flood program if Donald Trump takes the presidency in January. It’s a blueprint that many in the insurance industry have opposed.

“Full NFIP reauthorization would present Congress with an opportunity to improve the program by minimizing its complexity while strengthening its financial framework…,” the Best report said. “In either case the private market would need to take more risk, something it may not be willing to do without significant price increases.”

The report noted that the percentage of flood insurance premiums written by private insurers grew significantly from 2016 to 2022, when the private share peaked at 32%. In 2023, the percentage dropped slightly.

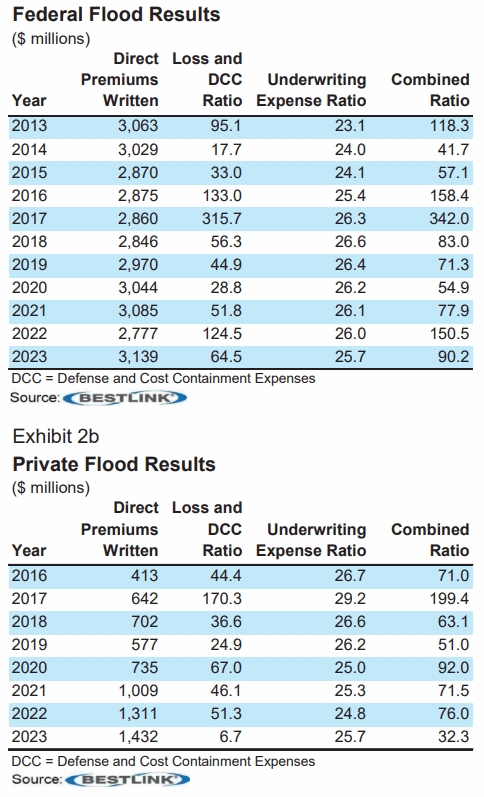

The lack of market development by private flood writers, if accurate, comes despite the fact that flood lines are quite profitable, the report noted. The combined ratio for private flood insurers has dropped, from a painful 199.4 in 2017 to a remarkably healthy 32.3 in 2023. That compares to a 90.2 combined ratio for the federal flood program in 2023, the report said.

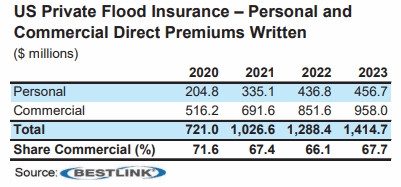

Most private flood policies are for commercial properties. Direct premiums written in 2023 were almost $1 billion, compared with $456 million for personal coverage, the report noted. The reasons for that are several: Commercial properties often need higher policy limits than what NFIP can offer, businesses may have large loans that require more flood coverage, and commercial enterprises need to cover inventory, while residential policyholders may choose to avoid coverage on contents.

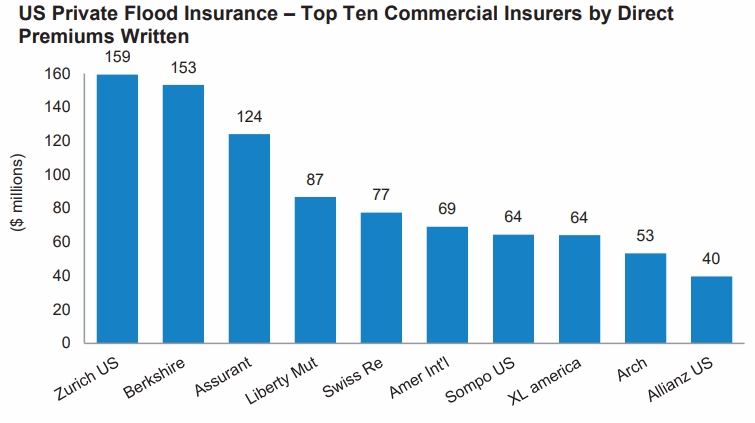

The largest private flood carriers for commercial coverage, as determined by direct premiums written, are Zurich US, Berkshire Hathaway, Assurant, and Liberty Mutual, the report said.

Some in the Florida insurance industry have suggested that private flood insurance has not grown as much as it could have partly because many insurance agents don’t push it. Commissions paid by the NFIP can be significant, while some private flood writers pay smaller commissions.

Some in the Florida insurance industry have suggested that private flood insurance has not grown as much as it could have partly because many insurance agents don’t push it. Commissions paid by the NFIP can be significant, while some private flood writers pay smaller commissions.

Neptune officials said last month that the company pays “competitive commission rates and agents appreciate the speed and ease of use of our system which allows them to greatly increase their earnings per hour of work vs. the NFIP.”

Most private flood insurers also offer much higher policy limits, which means higher premiums and relatively higher commission dollar amounts.

One idea in Congress could potentially improve the take-up rate on flood insurance – federal and private. U.S. Sen. Rick Scott, R-Fla., has introduced a bill that would allow a federal income tax break for homeowners’ insurance premiums. If the measure becomes law, it could reduce the pain of property insurance bills, freeing some policyholders to buy more flood insurance.

Top photo: Anne Schneider, right, hugs her friend Eddy Sampson as they survey damage left in the wake of Hurricane Helene, in Marshall, North Carolina. (AP Photo/Jeff Roberson)

Update: This article has been updated to include more information from AM Best, about the data covered by the report.

Topics Flood

Was this article valuable?

Here are more articles you may enjoy.

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed  CBIZ Brokerage to Be Spun Off, Backed by Private Equity, After $5B Grant Thornton Deal

CBIZ Brokerage to Be Spun Off, Backed by Private Equity, After $5B Grant Thornton Deal  AM Best Calls $1.54 Billion Mapfre-Safety Marriage ‘Strategically Compelling’

AM Best Calls $1.54 Billion Mapfre-Safety Marriage ‘Strategically Compelling’  Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026

Brown & Brown Estimates Cost of Howden-Driven Talent War Could Hit $60M in 2026