Transportation Network Companies like Uber, Lyft and Sidecar should bear the insurance burden when they encourage drivers to use their personal vehicles to transport passengers for a profit, according to recommendations made Wednesday from California Insurance Commissioner Dave Jones.

Jones’ recommendations were made to the California Public Utilities Commission, which oversees TNCs in California. His recommendations stem from a recent Department of Insurance investigative hearing in which insurers and TNC operators squared off over how auto insurance should be handled.

Jones’ recommendations were greeted with enthusiasm from insurer groups like the Property Casualty Insurers Association of America, which has been pushing for TNCs to provide primary commercial coverage for their drivers and not rely on personal auto insurance.

“It’s very good. I think he came down on the side of what is right, and what is safe for consumers and for drivers,” said Nicole Mahrt Ganley, a spokeswoman for PCI. “I think that he’s being responsible.”

TNCs have become a high profile topic in the last few months, and even former San Francisco Mayor Willie Brown has joined the debate. The TNC issue has gained public attention in part thanks to a perceived gap in insurance coverage, and a New Year’s Even incident during which a TNC driver under contract with Uber struck and killed 6-year-old Sofia Liu. Her family has filed a lawsuit against Uber. Uber issued a statement saying the driver, 57-year-old Syed Muzzafar, was not responding to a fare and didn’t have a passenger in his car when he struck Liu.

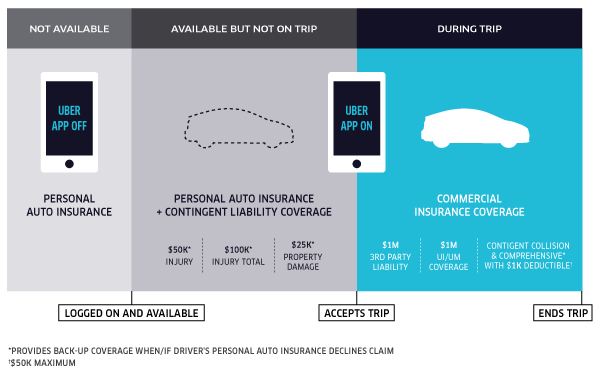

Since then the debate over TNCs has grown. The sticking point in the debate, which has taken on a triangular battle between TNCs, the insurance industry and taxi and limo providers, has been over a gap in insurance coverage during the period when TNC drivers have their smartphone app on but have not been matched with a ride.

“Our position has been that when the app is on and until the app is off the TNCs should provide their drivers with coverage and the personal auto policy should not be on the hook for that,” Ganley said.

In arguing that TNCs should provide commercial coverage, insurers noted that most personal auto policies have livery exclusions that will deny coverage if a person is carrying a passenger for hire.

In a statement announcing his recommendations Jones called attention to those gaps in insurance during TNC actives, and said: “As long as TNCs are encouraging non-professional drivers to use their personal vehicles to drive passengers for a profit, a risk which personal automobile insurance simply does not cover, TNCs should bear the burden of making sure that insurance is provided. Our recommendations will ensure there is insurance protection for passengers, drivers and pedestrians.”

TNCs were already required to have a $1 million commercial policy on drivers when giving rides or going to pick up a ride, but it was assumed that during this gap that TNC drivers’ personal policies would be in effect.

Jones has already recommended TNCs be required to carry insurance to cover this gap, and large players in the market like Uber and Lyft have already purchased excess commercial policies to cover this period.

However, among Jones’ recommendations on Wednesday was that TNCs be required provide $1 million commercial liability insurance as the primary policy for drivers.

Chris Shultz, a California deputy insurance commissioner, told Insurance Journal the policies held by Uber and Lyft would not be sufficient under Jones’ latest recommendation.

“Their coverage is excess, not primary,” Shultz said. “Our recommendation is that it be primary.”

The excess policy presumes a TNC driver’s insurance is in the first position, and the excess is in second position, he said, adding that in such a scenario, “every fender-bender is going to turn into a coverage dispute between the personal auto insurer and the commercial insurance for the TNC.”

Sultz said the other option to ensure coverage would be to require each TNC driver to purchase a commercial policy ranging from $5,000 to $10,000, which wouldn’t be feasible or available.

“We don’t’ think that you can buy commercial insurance that covers livery use on a personal vehicle,” Shultz said. “There isn’t yet a product that offers a personal endorsement or a rider that covers this use.”

While there had been talk that such insurance products may be in the works, no one has filed with the department to offer anything like what would be needed to cover TNC drivers using their personal vehicles for hire, he said.

Jones’ list of recommendations include:

- Requiring TNCs to provide $1 million commercial liability insurance that begins the moment a driver switches on the app;

- Requiring TNCs to provide $1 million uninsured/underinsured coverage to protect the driver and passenger;

- Requiring TNCs to provide insurance policy information to TNC drivers to carry in their cars;

- Requiring TNCs to disclose to drivers that their personal auto insurance coverages may not apply while they drive for the TNC;

- Requiring TNCs to provide comprehensive and collision coverage for the driver’s auto if the driver has those coverages on the driver’s own policy;

- Legislature should revisit the ridesharing and casual carpooling laws to allow for apps that match not-for-profit drivers with casual riders.

There are three bills pending in the state Legislature dealing with some aspect of TNC operations, and Shultz said he believes it’s likely that one of the authors of those bills may decide to include language in the bill make it so that TNC drivers’ personal auto insurance doesn’t get canceled or non-renewed by their personal auto insurer.

“We’re seeing where companies have canceled drivers after people have told them they are doing TNC services,” he said.

Lyft and Sidecard spokespersons didn’t immediately respond to requests for comment for this article.

Uber spokesman Lane Kasselman provided this written response, as well as the hyperlinks, via email:

“Uber’s ridesharing insurance policies lead the industry and ensure safety and coverage for riders and drivers. On top of the $1million commercial policy during trips, Uber was the first to add $1million of uninsured/underinsured motorists’ coverage during trips and to put contingent coverage in place to cover the time that a driver is available to receive requests but between trips. As a recipient of a TNC permit from the California PUC, having clearly met all CPUC requirements, we are proud to be the standard-bearer on this issue.”

Kasselman did not respond to follow up questions regarding Uber’s contingent, or excess, coverage.

Geoff Mathieux, founder of Wingz, a planned rideshare provider that focuses on trips to the airport, was encouraged by Jones’ recommendation that the Legislature revisit laws pertaining to ridesharing, but thinks any such law should pertain to for-profit activities.

He’d like to see the Legislature create laws that enable drivers to purchase optional coverage for their for-profit ridesharing activities, particularly since many TNC drivers use multiple ridesharing apps.

“We’re seeking to recommend to the California Legislature to create a law to allow citizens to purchase optional coverage for any paid or for-profit activities they may engage in in their personal vehicles,” Mathieux said.

Mathieux has as his legal representation Willie Brown Jr., San Francisco’s former mayor and former speaker of the Assembly.

Brown, who Mathieux said is a part owner in Wingz, submitted written comments to CPUC to encourage the group to consider creating a legislative vehicle providing for such optional coverage.

“Californians need the option to purchase additional personal insurance for their ridesharing activities, regardless of what method they use to find riders,” Brown wrote. “The requirement for automobile insurance should be on the driver, not on the website company.”

In his comments Brown noted that Craiglist, Meetup.com, 511.org, and various university websites offer similar paid ridesharing matchups but have no commercial insurance.

Mathieux said a new law from Legislature that enables such coverage would eliminate confusion around which insurance is responsible.

“If you continue a system where we’re the ones who have to have the insurance and there’s accidents, people are going to point the fingers at multiple companies,” Mathieux said. “It’s going to continue the climate of litigations that is currently surrounding this whole thing.”

The commissioner’s letter and complete recommendations to the CPUC can be found on the department’s website.

Topics California Auto Excess Surplus Personal Auto Sharing Economy Ridesharing

Was this article valuable?

Here are more articles you may enjoy.

Pritzker Signs Bills Giving Insurance Department Power to Overturn Rate Changes

Pritzker Signs Bills Giving Insurance Department Power to Overturn Rate Changes  Trump’s Latest Tariffs Hit With New Lawsuit by 25 States

Trump’s Latest Tariffs Hit With New Lawsuit by 25 States  NYC Mayor Mamdani’s Rent Freeze Heaps Pressure on a Teetering CMBS Deal

NYC Mayor Mamdani’s Rent Freeze Heaps Pressure on a Teetering CMBS Deal