This article is part of a sponsored series by Right Street.

Legislation to break up North Carolina’s rate bureau cartel and bring the state’s auto insurance market into the 21st Century has now been introduced in both houses of the General Assembly. This past week, Rep. Jeff Collins, R-Nash, introduced H.B. 265, a companion to Senate legislation introduced late last month by Sen. Wesley Meredith, R-Fayetteville.

Both bills would allow auto insurers to opt out of the North Carolina Rate Bureau, a legally mandated, but privately run organization through which insurers currently set rates collectively. Companies who do opt out would be permitted to consider any rating and underwriting factors they deem appropriate, so long as rates are sufficient and not excessive or discriminatory. There would be a 12 percent “flex band” in which rate increases would be presumed to be appropriate, although even those could be challenged by the Department of Insurance, so long as they provide justification.

The changes would bring North Carolina in line with the competitive markets that are found in most states today, in which insurers have incentive to develop new products and offer competitive discounts to attract business. Predictably, vested interests in the Tar Heel state – both economic and political – are pushing back hard against reform, and it unfortunately appears some of the state’s leading newspapers have taken to regurgitating the old guard’s talking points.

Perhaps the biggest misconception – repeated in recent editorials in both The Charlotte Observer and The Pilot (from rural Moore County) – has to do with the insurance reform record of neighboring South Carolina. Both papers (presumably repeating a “fact” slipped to them by the opposition, which includes the insurance commissioner and the insurer with the largest market share) allege that following passage of reform legislation in 1999, auto insurance rates in South Carolina rose by 25 percent.

Neither paper cites a source for this claim, nor a time frame over which this purported rate hike was observed. Which is unfortunate, because the claim is flatly untrue.

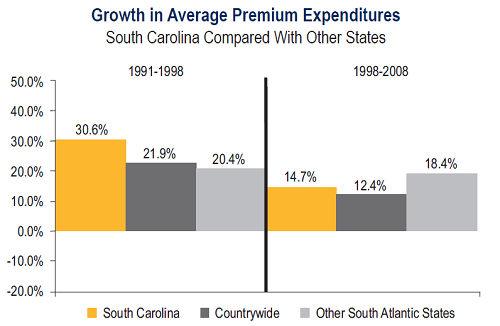

As this chart from the Insurance Research Council shows, while it is true that average auto insurance premiums have risen in South  Carolina in the decade since the state passed reform legislation, that’s because they rose everywhere else too. From 1998 to 2008, South Carolina saw auto insurance expenditures grow by 14.7 percent (not 25 percent), which was slightly higher than the 12.4 percent national average, but still notably lower than 18.4 percent average across all the South Atlantic states.

Carolina in the decade since the state passed reform legislation, that’s because they rose everywhere else too. From 1998 to 2008, South Carolina saw auto insurance expenditures grow by 14.7 percent (not 25 percent), which was slightly higher than the 12.4 percent national average, but still notably lower than 18.4 percent average across all the South Atlantic states.

More importantly, what the North Carolina papers do not note is that in the eight years before reform passed, South Carolina’s rates spiked by a whopping 30.6 percent, compared to 21.9 percent nationally and 20.4 percent in the region. Reform clearly slowed, not accelerated, the rate increases. The IRC estimates South Carolina’s rates today are 4.8 percent lower than they would have been if reform hadn’t been adopted.

The Observer‘s editorial adds:

The bill is supported by at least 14 insurers, including State Farm, Allstate, Geico and Progressive. They argue that a free-market approach would force companies to compete aggressively on price, letting drivers shop around for the best deal. But insurers already compete on price. The rate bureau method sets a ceiling, not a floor; insurers are free to charge less to attract customers, and often do.

This is wrong on at least two counts.

For one, it sets a remarkably low bar on what counts as “competition.” Imagine if the market for autos worked the way North Carolina’s market for auto insurance does. Ford, Chrysler and General Motors, along with Toyota, Volkswagen, and the whole panoply of foreign car makers, would get together and define what their product – a “car” – should be. They would determine how big it can be, how fast it can go, what color it should be, even how many cup-holders it can have. They’d then come up with a joint recommendation for how much it should cost and send that off to the auto commissioner, who would either give a thumbs up or a thumbs down.

And with that, the market’s terms would be set. Now, how many folks would define that market as “competitive,” simply because the manufacturers would have the option, if they wanted, to knock a few dollars off the MSRP sticker price every now and again?

It’s almost time for March Madness, an event that brings joy to millions of North Carolinians every year. As this year’s games are played, it’d be useful to take notice of all the auto insurance products that are hawked during breaks in the action – policies with deductibles that drop the longer you avoid an accident, policies that offer discounts for drivers with good credit, policies that give regular rebate checks, policies that offer deep discounts to those who provide real-time driving data to their insurer – all of which remain unavailable in North Carolina because they just simply don’t fit the state’s one-size-fits-all auto insurance system.

But the Observer‘s observation gets it wrong in an even more fundamental sense. The rate bureau’s recommendation actually does not represent a ceiling on what insurers can charge for auto insurance. It instead represents a ceiling on what can be charged for a standard liability policy. But many people want more than just a liability policy — they want to insure their car for collision, theft and other damage.

Higher risk drivers who want collision and comprehensive physical damage coverage will generally find in the mail a letter from their carrier containing a “Consent to Rate Form.” This is, essentially, a request by the insurer to charge rates that exceed those recommended by the Rate Bureau. It is relatively common for consumers to consent to these requests, and in those cases, the ceiling doesn’t apply at all. In some ways, the flex band system proposed by the Meredith/Collins bills would be actually be more restrictive than the prices insurers can charge for CTR policies today.

For liability coverage, high risk drivers dumped into the North Carolina Reinsurance Facility, which does not offer physical damage coverage. The rest of the state’s auto insurance consumers get dinged by this system as well, as they are charged surcharges to support these so-called “clean risk” policies.

This is not a small problem. More than a fifth of all North Carolina drivers – some 1.54 million in total – cannot get a standard auto insurance policy. Indeed, while large residual markets used to be fairly common in the days before the use of credit information and advanced computerized underwriting allowed insurers a way to segment and price these higher risks, today, North Carolina drivers represent 81 percent of the 1.9 million residual market auto insurance policies written in the whole United States.

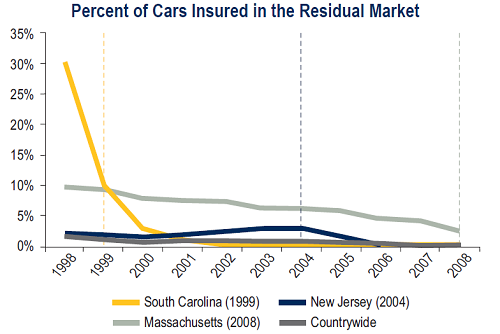

Returning to the South Carolina example, the rapid decline in the size of the residual market – which accounted for more than 30 percent  of the policies in 1998, but are now less than 1 percent of the market – is the most remarkable outcome of reform. As the accompanying IRC chart shows, other states that have opened their auto insurance markets to competition, like New Jersey and Massachusetts, have likewise seen steady reductions in residual market policies.

of the policies in 1998, but are now less than 1 percent of the market – is the most remarkable outcome of reform. As the accompanying IRC chart shows, other states that have opened their auto insurance markets to competition, like New Jersey and Massachusetts, have likewise seen steady reductions in residual market policies.

The bottom line is this: Auto insurance is now a highly competitive business in virtually every state but North Carolina. North Carolina drivers have been fortunate that, for a variety of reasons, the underlying costs of that drive auto insurance claims are relatively low. These include caps on tort damages, reasonably tight enforcement of vehicle safety standards, demographics, and relatively low traffic density. All of these factors combine to make auto insurance premiums relatively affordable.

But the fact that rates aren’t especially high doesn’t make the market competitive. The fact that a reasonably large number of insurers do business in the state, likewise, doesn’t automatically make the market competitive. Indeed, given that state law requires that the insurance commissioner guarantee that insurers earn a “reasonable rate of return,” why wouldn’t they want to do business there? Guaranteed profits are hard to turn down, in any industry.

When prices and terms of coverage are set collectively, when companies have no incentive to innovative or introduce new products, that is, by definition, an uncompetitive market. It is a cartel, and it is time for that cartel to come to an end.

Topics Auto North Carolina

Was this article valuable?

Here are more articles you may enjoy.

AIG Completes CEO Succession Plan With Anderson to Take Reins

AIG Completes CEO Succession Plan With Anderson to Take Reins  How Niche Insurance Shielded Bad Bunny From Bad Weather

How Niche Insurance Shielded Bad Bunny From Bad Weather  Trend of Fewer Insurance M&A Deals ‘Bottoming Out’: OPTIS

Trend of Fewer Insurance M&A Deals ‘Bottoming Out’: OPTIS  NFL’s Rooney Rule Meets Biggest Challenge in Trump’s DEI Crackdown

NFL’s Rooney Rule Meets Biggest Challenge in Trump’s DEI Crackdown