Its acquisition of Fireman’s Fund’s business in April, 2015 provided ACE Ltd. with an idea of what’s involved in integrating two leading high net worth insurance businesses.

Frances D. O’Brien is now using those corporate insights along others she has garnered from 36 years in the business as she heads the integration of ACE Private Risk Services with that of its former competitor, Chubb Personal Insurance, to create the new Chubb’s high net worth business unit for the U.S. and Canada.

According to the division president for North American personal risk services for the new Chubb, the Fireman’s Fund experience along with the time between the July announcement and the mid-January closing on the ACE-Chubb deal provided a safety net of sorts, supplying guidance and time to plan the integration of $5 billion in wealth insurance accounts and more than three decades of history and relationships.

“So we’re bringing together three great companies,” O’Brien said in a recent interview with Insurance Journal, adding that the new entity gets to benefit from the best that each one of them has to offer. “We’ve had time to plan.”

To gauge the extent of the endeavor, Insurance Journal asked O’Brien how many people are involved in the integration strategy. “Who’s not involved?” she quipped.

“There’s actually some excitement, particularly with our staff, about the merger because it just brings about the possibility of learning from each other, and collecting all the best practices across the three companies, and being able to bring something even better to our agents. You have to keep in mind that the three portfolios have been around for about 35 years now,” she said.

No Disruption

As for the integration process, the goal is for there “to be as little disruption as possible” for everyone, O’Brien said.

Early on in the acquisition process, CEO Evan Greenberg praised the Chubb agency culture. “We’re going to preserve the agency culture. We’re going to preserve the agency distribution. We’re going to preserve the branch system,” said Greenberg.

Thus preservation of good relations with the combined firm’s 3,500 agents is high on O’Brien’s to-do list.

Chubb

“On this goal of non-disruption to our agents, we’ve come out of the box very strong to make sure they know what is happening. We’re getting very good feedback from our agents on the communication that we’ve done with them,” O’Brien told Insurance Journal. “They haven’t felt any concern that they don’t know who to call or how to do business with the new Chubb. We’ve been very specific about how we’re going to be moving forward.”

Agents are able to deal with the same underwriters they worked with before the merger. “We basically buddied up the underwriters by agent from the Chubb legacy and ACE. We were able to tell the agents pre‑close that they would continue to have those relationships,” she said.

Communications Effort

The communications effort around the integration has been multi-faceted. It began with written communications posted online because “these days communication has to be on-demand,” O’Brien said. They were conscious of the fact that their agents are trying to do business with their customers and need access to the information in that moment to get things done. Sending a newsletter or even visiting, while part of the plan, are not sufficient.

“We spent a lot of time crafting communications to explain, ‘This is how we’re going to do business with you going forward. Here are your contacts. Here are your frequently asked questions.'”

After the closing, the company kicked off a plan to visit or call every branch office and agencies within the first 60 days for the purpose of listening to them and asking, “Are you having any issues? Is there anything that we didn’t anticipate that we need to cover for you? Are there things that we need to be doing differently than how we’re currently working in the marketplace?”

O’Brien said the new Chubb has maintained its relationships with the agencies that did business with Chubb, ACE or Fireman’s Fund.

“We are continuing to do business with agents that currently have an agreement and business with one of the three companies,” she said.

In addition to the pre-close communications and the post-close calls and visits, O’Brien’s team also created what she calls “rapid response” desks where agents could bring any policy, service or underwriting issue that needed to be escalated or resolved promptly.

These rapid response teams have authority to respond to agents as quickly as possible.

“We’ve been tracking the issues that come to those desks. There hasn’t been anything that’s been a big miss or a big issue,” she said.

One of the first things agents want to know following a merger is how their commissions will be affected. O’Brien said the company is maintaining the guaranteed supplemental commission structure agents had under Chubb. “Our intent is not to in any way have a negative impact on our agents,” she said.

She projects it will “take a good part of a year” to complete the processes, the workflows, and bring together everything. That should please CEO Greenberg, who has said he thinks it could take two years before everything is settled.

Thus far O’Brien is pleased.

“We’re getting a lot of good feedback from our agents on how this is going really well and how they enjoy having easy access to our folks through visits over the phone,” she said.

High Net Worth Market

According to O’Brien, the merged ACE-Chubb-Fireman’s Fund entity has a unique perspective on the high net worth market.

“We have an unparalleled knowledge and expertise about the high net worth customer. We’ve had a couple of million claims that we’ve settled across the three companies so we understand better than anybody else what can go wrong for our customers, and how it could be prevented. There’s a lot of excitement about the future, I think both internally and externally,” she said.

Different insurers have different definitions and estimates of the high net worth market.

Different insurers have different definitions and estimates of the high net worth market.

Estimates range from $27 billion to as high as $80 billion. Definitions vary but tend to come down to those with high-valued homes who are likely to have additional valuable assets and be interested in buying additional insurance coverages. For example, Nationwide’s Crestbrook defines the market as those with primary homes that would require between $500,000 and $5 million to replace and who are interested in buying additional coverages and risk services. Crestbrook sees a potential $60 billion market under its definition.

Others like O’Brien define the market as beginning with those with residences valued at $1 million or more. O’Brien’s team estimates the high net worth personal insurance market in North America to be worth about $40 billion in premium. These are people with multi‑million dollar homes; collections of jewelry, fine art, antiques, or other collectables; multiple newer and higher‑valued cars; and a need for higher limits of personal liability insurance. Some also need workers’ compensation for domestic workers and directors and officers protection if they serve on not-for-profit boards.

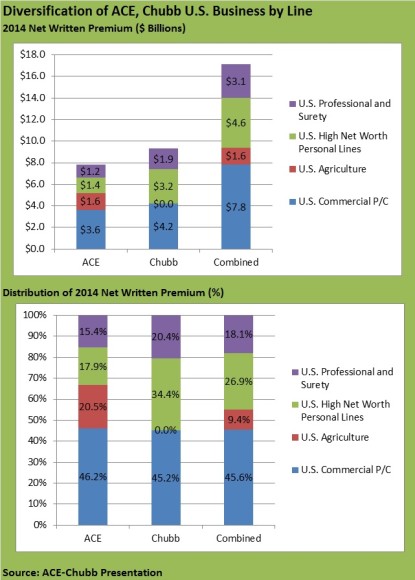

While $40 billion represents the potential in Chubb’s view, only about $7 billion of that is currently insured — $5 billion by the new Chubb.

That leaves about $2 billion insured by others including AIG, Privilege Underwriters PURE Group (recently recapitalized and now with backing from XL), Nationwide (Crestbrook), Allstate, Cincinnati Financial, USAA, State Farm and others.

Or put another way, using Chubb’s market estimate, there is $33 billion uninsured market waiting to be captured. “There’s a lot of opportunity, and part of the relationship with working with our agents and brokers is to work with them to access that opportunity,” O’Brien said.

Market Potential

The potential on this market is clearly one of the reasons ACE pursued the Chubb deal. “Oh, definitely, definitely,” said O’Brien.

Upon announcing the Fireman’s Fund deal, ACE Private Risk Services touted the “powerful combination” of the two organizations, claiming it would take high net worth insurance “to new heights.” With Chubb, ACE is adding the company that says it created the market more than three decades ago.

O’Brien cites a Barclays wealth market report that there has been an increase in investing in tangible property such as fine art, jewelry and real estate — a trend that “aligns very nicely” with Chubb’s products and services.

In addition to insurance coverages, Chubb offers a consulting service that offers advice on how to mitigate any damage. “As you can imagine, our customers are much more interested in prevention than in having a loss and having to deal with all the inconvenience of a loss,” O’Brien said.

Chubb risk consultants will visit a customer’s property and advise on how to prevent losses, such as recommending devices to prevent water damage from burst pipes, which she said happens to be the most frequent claim.

In the event there is a claim, Chubb prides itself on its claim service that can come in very quickly, set up drying machines, and help mitigate any damage.

It also offers a wildfire defense service in drought areas that protects a property by clearing it of any fuel that might be around the house, setting up sprinklers and, if necessary, putting a fire retardant on the house so that it will not catch if the embers from the wildfire fly onto the house.

Changing Market

O’Brien has been around long enough to know that Chubb will face competition as it sets about trying to capture an even bigger slice of the high net worth pie.

“I’ve been in this business for 36 years so I’ve seen many rounds of companies coming and going. There always seems to be a time when there are a lot of companies interested, but eventually they leave the market, so then there’s less companies,” she said.

“Since legacy ACE and Chubb have become one, now there’s one less company and I suspect that there’ll be competitors coming, seeing this as an opportunity, and entering the market.”

The barriers to entry to this marketplace are not huge. It’s what needs to be done after entering that separates the winners from the losers.

“Given the way that they personal insurance market works in the U.S, your product is pretty easy to copy. Policies are publicly available. You can just photocopy the insurance contract and you’re in business. The difficulty is being able to have the services built around it and to really understand the customer,” she said.

“Given the length of years we’ve been in this market and the amount of customers we’ve served, there is nobody that knows what Chubb knows about high-net worth customers’ exposures, how to service them, and how to underwrite them,” she said.

Today’s high net worth market customers are inquisitive and risk management-sensitive.

“When I look back to when Chubb first started to focus on the high net worth market, we had customers that were very open to having their agents and brokers get them the broadest coverage out there, the best service out there, and saying, ‘Cover everything, and I don’t have to worry about it.’

“What’s happened over the last 35 years is customers are significantly more interested in understanding what they need specifically, and understanding the choices that they have about building the right risk management programs for themselves. They really value advice but they want to be educated on that advice,” O’Brien said.

Today’s customers are also thinking more about the future, according to the Chubb executive.

“They want to make sure they have thought of all the emerging risks that may crop up,” she said. Thus providers have had to evolve from, “Here’s a fantastic product that covers everything,” to, “Here’s how we can provide solutions to your particular needs and give you choice and control.”

She cites cyber risk as an example of a risk that has evolved. “We have had for many years now an ID theft coverage that can help them. We work with a firm that helps give them advice on how they can protect themselves,” she said.

High net worth customers are also time-sensitive.

“Everybody now is so time poor. They want solutions available when they need them and they want advice when they need it. They want validation that they’ve made the right choices,” she said.

That suggests that technology will play a greater role, not only in the homes of their clientele but also in how Chubb delivers its services.

“People want to be more mobile, even high net worth people want to be more mobile. They don’t necessarily want to have to wait a business day in order to get information, change something on their policy, or request something,” she said.

She said Chubb is focused on helping its agents do business more efficiently, so that they have more time to spend working on their customers versus servicing policy transactions.

But technology will not do everything.

“What we know from our customers, and this has been pretty consistent for many, many years, is that they really value the advice of trusted advisors like our agents and brokers,” O’Brien said.

Related:

- ACE Private Risk Survey: High Net Worth Families Overpaying to be Underinsured

- How Agents and Carriers Can Find Gold in Personal Lines

- ACE to Keep Most Fireman’s Fund Personal Lines Staff: Andrade

- XL Buys Stake in High-Net Worth Insurer PURE

- AIG Insurance Results Down in Q2; CEO Sees Opportunity in ACE-Chubb

- Ironshore Establishes Private Client Group, Launches Coverage in Select States

Was this article valuable?

Here are more articles you may enjoy.

Helicopter Crash in Georgia Kills Groom, Pilot, Hours After Huge Wedding Celebration

Helicopter Crash in Georgia Kills Groom, Pilot, Hours After Huge Wedding Celebration  Warmer World Means Bigger Hail and More Damage, Study Finds

Warmer World Means Bigger Hail and More Damage, Study Finds  Sentry to Sponsor PGA Tournament at Torrey Pines

Sentry to Sponsor PGA Tournament at Torrey Pines  AI Savings Misses ‘Should Be Making Executives Uncomfortable,’ Bain Says

AI Savings Misses ‘Should Be Making Executives Uncomfortable,’ Bain Says