Representatives from Florida’s Citizens Property Insurance Corp. delved into and defended their rate filing for 2016, which included significant increases in many Florida regions, before the Florida Office of Insurance Regulation (FLOIR) on Aug. 25.

While the focus of the hearing was the reason behind the overall rate increases in the state, Citizens emphasized during its testimony that water damage losses in South Florida have been a driving factor for a rise in claims and rates.

Citizens’ CEO Barry Gilway said water damage claims, which the company described as not flood-related but instead a water loss as a result of a sudden or accidental discharge of water by a pipe or water-system issues, have increased by 50 percent in severity and frequency.

“I want to be crystal clear on this issue: water losses are the major reason Citizens is seeking rate hikes for the coming year, especially in South Florida. Were it not for water loss… 99 percent of South Floridians -Miami-Dade South Florida policyholders would be seeing rate decreases,” Gilway said.

Gilway described the rise in water damage in South Florida as “very disturbing.” He said two years ago the frequency of water loss damage was 8 percent and has since risen to 13 percent, with the company now seeing an average of about 1,000 water damage claims a month. The average water damage loss 2.5 years ago was $9,000 and today is closing in on $15,000, he said.

Water losses are accounting for 33 percent of every premium dollar of Citizens’ policyholders, according to the company.

Citizens is now focused on combating this problem, Gilway said. The company recently had a “water summit” where it brought together legal, underwriting and policy experts to develop strategies to counter the problem.

“We have to respond and have to respond aggressively,” Gilway said.

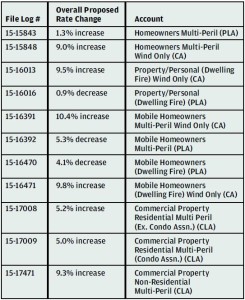

Citizens’ Requested Rate Changes

Citizens’ policies with proposed rate changes effective Feb. 1, 2016 include:

There were no rate changes proposed for sinkhole policies.

Insurance Commissioner Kevin McCarty opened up the hearing by emphasizing that Citizens is not under fire for its submitted rate proposal. “This is a fact finding hearing – it is not an adversarial hearing,” he said. “The office has not made a decision relating to the filing… the office is not advocating a position for or against Citizens in this rate request hearing. We are trying to get at the facts for the citizens of Florida.”

McCarty said FLOIR and Citizens have been in correspondence over the rates that were filed and Citizens has supplied FLOIR with all the necessary data to back up its rate filing. As a result, FLOIR questioned Citizens on the purchase of more reinsurance since 2014 while it has at the same time reduced its policy count and corresponding exposure; the necessity of Citizens purchase of more pre-event funding given the significant surplus it has accumulated over the years; and the increase of certain loss trends – Citizens alleged in filings that water losses in certain Florida counties have contributed to increased losses in these areas. FLOIR wanted to know what was behind such an increase and what other steps Citizens is taking to control those costs.

Citizens’ Depopulation Program

McCarty applauded Citizens’ policy count reduction by almost a million policies over the last several years, calling it a “Herculean effort” on the part of Floridians to remove billions of dollars of assessments that could be levied on all policyholders. The clearinghouse and takeout efforts have been successful in returning policyholders to the private sector, he said.

Gilway said this year there has been a 37 percent reduction in policy count with more expected as the remaining months of the year have historically seen the most reductions in policy count for the company.

However, while Citizens rate proposal lowers rates for 60 percent of its personal lines policyholders, Gilway said, the company is seeking an average 3.2 percent increase in statewide rates for personal lines customers, which reflects both longstanding disparities in wind-only rates and recent challenges relating to water losses, he said.

In the wind and coastal areas, Gilway said Citizens has become more of a residual market and though their policy count is the fewest it ever has been, the policies that remain with Citizens are those in high-risk areas.

“The remaining policies are the more difficult policies. The good policies as perceived by the insurance companies and private carriers are gone so what we are left with is a ‘residual’ book of business and frankly that’s our charge – to act as a residual mechanism.”

Gilway said the company is doing everything in its power to not let operational costs affect policyholders and embarked on an effort to streamline its operations and improve how Citizens does business.

Gilway highlighted the ways Citizens has tried to improve its efficiencies and cut overhead costs, including consolidating offices, updating legacy systems, and improving its investment portfolio.

“Taken together, the efforts have eliminated the assessment on Floridians in the event of a 1 in 100 year storm,” he said.

John Rollins, chief risk officer for Citizens, said they are recommending rate decreases for a majority of its personal lines account policyholders, who tend to be in the inland regions, but increases for the majority of its coastal account policyholders.

McCarty questioned why Citizens purchased so much reinsurance, one of the reasons cited for the rate increases for wind exposures, when the company’s business and exposure have decreased by 35 percent.

Rollins responded that Citizens has to be able to reinsure a 100 year event to avoid an assessment risk and he questioned if Citizens should reinsure itself like a private company which has to have its portfolio protected up to about 25 to 30 percent. If the answer is “yes,” Rollins said, then the company should have purchased more reinsurance. Rollins added that with reinsurance rates being so low at the moment it made sense for the company to take advantage and have a more secure risk transfer solution.

Water Damage Claims

Citizens said its efforts to deal with the water loss problem have included encouraging insureds to call Citizens before contacting an attorney or public adjuster, as well as focusing more efforts on fraud awareness in conjunction with the Department of Financial Services. Rollins said 90 percent of all the representative water claims come from Miami-Dade and 30 percent of those claims the company never gets to look at as they come from a public adjuster.

Citizens is also launching an emergency services and contract to repair program, which will initially be on a volunteer basis. The company stated it would like to work with FLOIR to have the right policy language to respond to those claims.

“This is an out of control situation similar to sinkhole [and it] may take policy and legislative changes to address this,” Gilway said. “We need to focus on solutions for this issue. Every time an attorney or public adjuster gets involved in these claims the costs sky rocket – that’s the bottom line.”

Rollins said the company is putting great effort into what is causing the water issues, but actuarially they have not been able to find a trend or cause for the increase. “This trajectory is not good for consumers,” he said.

A representative for FLOIR would not comment on how the hearing will impact the office’s decision, saying FLOIR cannot comment on a pending rate filing. A rate decision on the homeowners, mobile homeowners and dwelling fire filings is expected on Sept. 8 or 9. The other filing decisions will occur at a later date.

Topics Trends Florida Claims Profit Loss Reinsurance

Was this article valuable?

Here are more articles you may enjoy.

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed  Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks  Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers

Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers  Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal

Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal From This Issue