The seeds for the rapid disintegration of Lex Greensill’s empire were sown eight months ago, when a little-known Australian insurer called Bond and Credit Company decided not to renew insurance policies covering $4.6 billion in corporate loans backed by the financier’s firm.

The policies were due to lapse on March 1, prompting a last-ditch effort from Greensill’s supply-chain firm to take the insurer to court in Australia, warning that losing insurance coverage for its 40 or so clients could spark defaults and put 50,000 jobs at risk. But late on Monday a judge in Sydney struck down Greensill’s injunction, triggering a series of events that have since reverberated around the world.

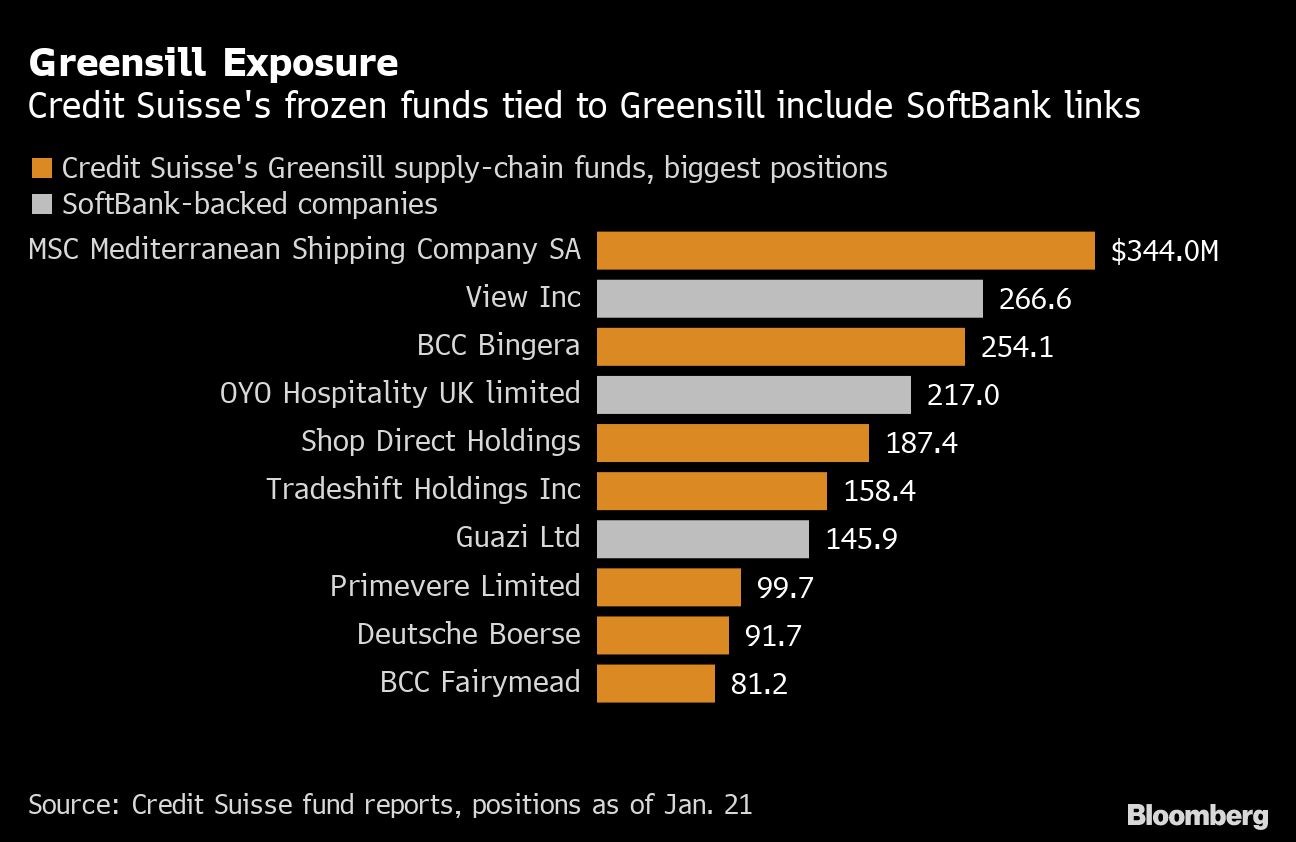

Hours later in Zurich, Credit Suisse Group AG suspended a $10 billion family of funds that invested in debt arranged by Greensill Capital, choking off a key source of funding that’s left the tycoon’s namesake firm struggling for survival. Germany’s financial regulator BaFin has also stepped in, taking oversight of a German bank run by Greensill as it considers freezing payments in and out of the lender.

Greensill Capital is now seeking a last-minute rescue with talks to sell its operating business to Athene Holding Ltd., an annuity seller part-owned by New York-based private equity firm Apollo Global Management, even as it starts insolvency proceedings in the UK.

The series of events underscore a key element that underpinned Greensill’s strategy: insurance policies. The Credit Suisse funds invested in loans that were originated by Greensill Capital, which provides a type of loosely regulated short-term funding to help companies pay their bills on time. In a twist that’s peculiar to these types of vehicles, the funds were able to garner the third-highest rating from Moody’s Investors Service — based in part on the credit score of the insurers that backed the underlying debt.

Insurance Policy

In addition to the role of the insurers, the episode also highlights the ongoing mismatch between high ratings and the risks posed by underlying assets, more than a decade after ratings companies were criticized and investigated for assigning triple-A labels to subprime debt that later turned out to be worthless.

A Greensill spokesman declined to comment, as did representatives for Bond and Credit Company. A representative for Moody’s didn’t immediately have any comment.

The insurance arrangements gave firms like Greensill’s the flexibility to court smaller borrowers that wouldn’t otherwise be able to get investment-grade ratings, with a measure of security that an insurance policy brings. The impeccable credentials also allowed Credit Suisse to sell funds to investors such as pensions and corporate treasurers seeking suitable assets to help boost returns.

But the model hinges on the insurers renewing their policies as long as the underlying debt is still held in the fund. Credit Suisse decided to suspend the group of funds after credit insurance offered by Bond and Credit Company, a unit of Japanese behemoth Tokio Marine Holding, ended Monday on some of the loans Greensill made, according to people briefed on the matter. That left some debt no longer valued on the strength of the insurer but rather on the underlying borrower, triggering questions on the valuations of the assets.

It’s not clear why Bond and Credit Company allowed the policies to lapse. In denying Greensill’s injunction to force the insurer to renew the contracts, the Australian judge noted that “despite the fact that the underwriters’ position was made clear eight months ago, apparently Greensill only sought legal advice about its position” in the last week of February.

There have been signs of pain at several companies that borrowed through Greensill amid the market turmoil induced by the pandemic. Some companies backed by the firm also collapsed last year amid suspected accounting issues, including hospital operator NMC Health Plc and commodity trader Agritrade International.

Loans tied to a single UK entrepreneur, Sanjeev Gupta, have also emerged as a focus at Germany’s financial regulator. BaFin has been pressuring Greensill Bank to reduce the concentration of assets linked to Gupta, Bloomberg reported in August. The bank had been seeking to raise money and cut its exposure to companies linked to Gupta, people familiar with the matter previously said.

Greensill rose from working on his family’s sweet potato and sugar cane farm in Australia. He carved a niche for himself in the fast-growing supply-chain finance world, building a business at Morgan Stanley in London financing corporate supply chains, and then worked at Citigroup Inc. He started his own company in 2011, attracting backers like SoftBank Group Corp. and wooing advisers such as former UK Prime Minister David Cameron.

This week marks a dramatic fall for Greensill’s firm, which in October had been considering a capital raising that would have valued it at $7 billion. One of its earliest backers, SoftBank’s Vision Fund, had already substantially written down its $1.5 billion holding in Greensill, and was considering dropping the valuation to close to zero, people familiar with the matter said Monday.

Greensill Capital lost another longtime ally after Swiss money manager GAM Holding AG said it’s ending dealings with the firm and unwinding an $842 million fund that invested in Greensill-linked companies.

–With assistance from Jack Farchy.

Topics Carriers

Was this article valuable?

Here are more articles you may enjoy.

Gallagher’s RPS Acquires W.N. Tuscano Agency, a Pennsylvania MGA

Gallagher’s RPS Acquires W.N. Tuscano Agency, a Pennsylvania MGA  Two Years in, Ortiz Steps Down as CEO of Florida Re

Two Years in, Ortiz Steps Down as CEO of Florida Re  Tropical Storm Watches Posted Across Florida’s Panhandle Region

Tropical Storm Watches Posted Across Florida’s Panhandle Region  New Jersey E-Bike Registration, Insurance Requirements Now in Effect

New Jersey E-Bike Registration, Insurance Requirements Now in Effect