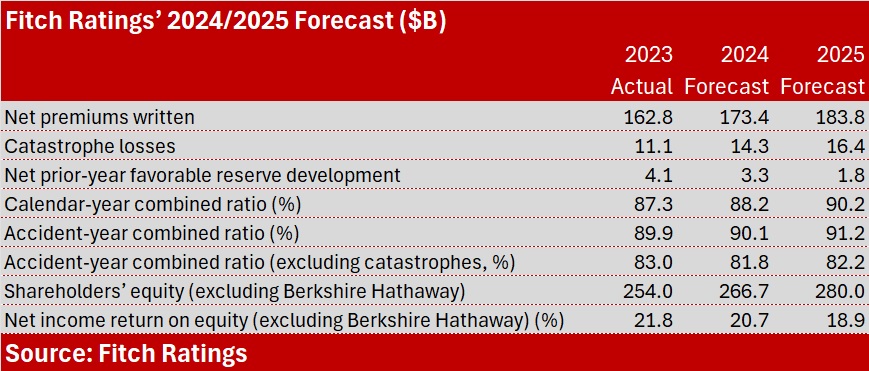

Fitch Ratings announced that it shifted its outlook on the global reinsurance sector to neutral yesterday but the downward shift came with an expectation of continued profitability—and a forecasted combined ratio around 90 in 2025.

The revision—from a prior outlook of “improving”—reflects Fitch’s view that the pricing cycle is likely past its peak.

Related: Global Non-Life Reinsurer’s Profits to Peak in 2024: Fitch Rating’s Midyear Analysis

“Currently, the sector is in very good shape with very strong capitalization and record financial performance by historical standards,” said Manuel Arrivé, Fitch Ratings’ director and head of EMEA Reinsurance. “We expect both balance sheets and profitability to remain resilient in 2025, but further improvements in fundamentals from this point are less likely,” he said, during a webinar yesterday.

Essentially, he said, the neutral outlook means that Fitch expects the main credit drivers for the sector will remain broadly stable over the next 12 months.

Arrivé outlined positive and negative factors driving the outlook change. On the positive side, persistent underwriting discipline, along with comfortable capital buffers that were bolstered with record profits in 2023 and first-half 2024, both position reinsurers well for a decline in prices—even as claim costs, and catastrophe losses in particular, continue to rise.

On the negative side, Arrivé said the reinsurance market has in fact started to soften.

“Capital has been growing faster than demand and that has closed the gap in property-cat, for instance—and that also has a stabilizing effect on pricing at renewals,” he said.

The sector’s abundance of capital, he said, is expected to drive “a moderately softer and more competitive market in 2025.”

Giving a high-level view of reinsurance price changes achieved throughout 2024, referenced from various broker reports, Arrivé said that property rates were flat to down for cat loss-free business, up only slightly for loss-hit business, and up 10-15 percent for casualty (with loss-affected accounts priced at the higher end and no-loss accounts at the low end).

“Looking forward, our base case for property-cat is for a moderate and gradual softening. But rates should remain adequate—and [the] tighter terms and conditions obtained last year should hold.

“Of course, reinsurers would like higher rates for longer, but they’re more open, we believe, to negotiation on prices than structure because maintaining the current reinsurance structures are more meaningful for them than prices in terms of profitability.”

Arrivé said it’s Fitch’s view that current favorable market conditions “will not end abruptly even if the loss experience remains benign for the rest of the year.”

“That said, the market remains nervous and could harden again if there is a high-magnitude industry event in the second half of the year,” he said.

Putting the softer property pricing together with expectations for casualty reinsurance rates—varying by subline, but projected to rise for U.S. casualty in order to keep pace with social inflation— Arrivé summarized the impact on profit margins.

“We expect underwriting margins to have peaked in 2023, 2024. And we expect market conditions next year to remain supportive of strong returns even if prices soften again.”

While Fitch forecasts flattening-to-declining profit margins in 2025, “we are still at very attractive levels of combined ratio of around 90, with stable investment income contributions. That would translate into a very strong sector return on equity of close to 20 percent, which is in sharp contrast with what we’ve seen in the soft market years 2020, 2022 where ROEs were around 5 percent,” Arrivé said.

While the report does not specifically mention whether combined ratio forecasts include the impact of discounting for reinsurers reporting under the IFRS 17 accounting standard, the 87.3 actual combined ratio figure does include the discounting impact, according to a Fitch report on midyear reinsurance results published last week.

Separately, this week, Standard & Poor’s Global Ratings published a report with actual prior-year profit margins and forecasts based on a cohort of 19 global reinsurers—putting the undiscounted 2023 combined ratio at 91.5, and forecasts for 2024 and 2025 in the 92-96 range. While S&P is maintaining a stable outlook on the sector, S&P’s ROE forecast drops more quickly than Fitch’s—from 21.4 percent in 2023 down to mid-to-low teens levels in 2024 and 2025.

In contrast to both S&P and Fitch, Moody’s Investors Service revised its outlook for the global reinsurance sector to positive from stable earlier this week. Structural changes in property reinsurance programs are among the key drivers of the outlook change highlighted in Moody’s outlook report. “Property reinsurers have raised the loss thresholds where reinsurance cover is triggered, and have reduced their exposure to high frequency, low-to-medium severity natural catastrophes such as severe convective storms.”

“Persistently high losses have prompted reinsurers to underwrite less of this risk, leaving primary insurers to bear a higher share of it,” Moody’s analysts wrote in the report. The report displays a side-by-side graphical comparison of primary insurer and reinsurer ROEs, with reinsurer ROEs spiking to nearly double the median return on equity for insurers in 2023, as the primary players absorbed a majority of that year’s high frequency weather losses.

According to the report, increased reinsurance premiums, beneficial risk/return ratios and robust investment earnings also factored into the outlook change.

“With only limited new capital entering the market, this will drive continued strong profitability over the next year, assuming no large catastrophes,” said Brandan Holmes, Vice President-Senior Credit Officer at Moody’s Ratings, in a statement about the changed outlook.

Rating agency AM Best also shifted its rating outlook for the global reinsurance sector up to positive from stable in June.

Related: AM Best Ups Reinsurance Outlook to Positive

Topics Trends

Was this article valuable?

Here are more articles you may enjoy.

Law Restricts Her From Reducing ‘Excessive’ $91M Injured Worker Award, Judge Finds

Law Restricts Her From Reducing ‘Excessive’ $91M Injured Worker Award, Judge Finds  Troubled Alabama City Loses its Liability Insurance Coverage

Troubled Alabama City Loses its Liability Insurance Coverage  American Family to Acquire Bowhead Specialty in $1.2B Cash Deal

American Family to Acquire Bowhead Specialty in $1.2B Cash Deal