While lawmakers in most states have introduced measures in their current legislative sessions that address gun control and gun liability issues, their approaches vary widely, largely depending on the area of the country in which their states are located.

Legislation introduced in many states in the East would strengthen gun controls and/or require gun owner liability insurance.

Bills introduced in states across the nation’s midsection for the most part would strengthen the rights of gun owners. One exception is Illinois, where a bill that would require mandatory gun owner liability insurance was proposed but failed to progress.

In the West, California lawmakers have introduced bills to require gun owner liability insurance, raise taxes on the sale of ammunition and allow more local control of gun laws.

Bills requiring firearm liability insurance for gun owners have been introduced in several Northeast states as part of larger, comprehensive gun control packages. But it appears many of these proposals are facing an uphill battle.

Gun liability insurance bills have been filed in Massachusetts, New York, Connecticut, Maryland, Pennsylvania, and Washington, D.C. Many of these bills contain similar languages, though some are more detailed than others.

The New York, Washington, D.C. and Pennsylvania bills specify that liability policies should cover damages resulting from any negligent or willful acts. The bills also authorize state insurance departments to promulgate more detailed rules and regulations as needed going forward.

The idea of adopting compulsory liability insurance for gun owners as a mechanism to reduce gun violence and compensate victims is not new. But legislatives efforts have not been successful. In fact, according to the National Council of State Legislatures, some 20 such bills have been turned down at the state level during the past decade.

This year, in March, proposals from two Northeast states have stalled. In Connecticut, the measure was apparently stopped following a public hearing in which most of the speakers criticized the measure as flawed, according to a media report. A proposed bill in Maryland also died.

Critics say there aren’t any products in the standard market that would provide coverage described in proposed bills and that enacting such bills would not automatically entice insurers to develop an appetite for offering such coverage. That means states might have to step in and create residual markets or pooling or assigned risk plans.

There have also been concerns over some provision languages that require coverage for “willful acts” and what that might entail.

Currently, standard homeowners insurance policies typically cover accidental discharge of a firearm that results in injury or property damage, according to Ellen Melchionni, president of the New York Insurance Association.

Homeowners liability limits are commonly $100,000, but higher limits are available.

Liability policies can be purchased at a variety of different levels, and excess personal liability for firearms owners is generally only available through firearms associations, such as the National Rifle Association’s excess personal liability insurance of up to $250,000. Losses from self defense can be covered while malicious, intentional acts are not.

Massachusetts

In the Massachusetts House of Representatives, State Rep. David Linsky (D-Natick) sponsored House Bill 3253 (An Act to reduce gun violence and to protect the citizens of the Commonwealth), which contains gun liability requirements along with several other provisions for regulating the licensing, sale and possession of firearms.

HB 3253 proposes that “whoever possess, carries, or owns a firearm, rifle or shotgun without a liability policy or bond or deposit required by the provisions of this chapter which has not been provided and maintained in accordance therewith shall be punished by a fine of not less than $500 nor more than $5,000 or by imprisonment for not more than one year in a house of correction, or both such fine and imprisonment.”

The insurance requirements would not apply to a person who possesses a firearm on a temporary basis while on the premises of a licensed gun club. The provision proposes that the insurance commissioner shall promulgate regulations set forth for the minimum terms of liability insurance policies. The bill remains pending with no action yet taken, according to the Massachusetts Insurance Federation.

New York

In New York, Assemblyman Felix Ortiz (D-Brooklyn) introduced Assembly Bill 3908 (An Act to amend the insurance law, in relation to requiring owners of firearms to obtain liability insurance) in January. It proposes to amend the insurance law, so that anyone, excluding any peace officer, “who shall own a firearm shall, prior to such ownership, obtain and continuously maintain a policy of liability insurance in an amount not less than $1 million specifically covering any damages resulting from any negligent or willful acts involving the use of such firearm while it is owned by such person.”

Under the bill, failure to maintain such insurance would result in the revocation of the owner’s registration, license and any other privilege to own a firearm.

The insurance policy will ensure that “innocent victims of gun-related accidents and violence will be compensated for the medical care for their injuries,” according to the bill memo. “This insurance policy will also serve as an incentive for firearm owners to implement safety measures in order to conduct the activity as safely as possible and only when necessary.”

AB 3098 was referred to the Insurance Committee in January.

Connecticut

In the Connecticut House of Representatives, House Bill 6656 proposed that any person who possesses or owns a firearm shall “procure and maintain (1) excess personal liability insurance that provides coverage for bodily injury or property damage caused by the use of a firearm, and (2) self defense insurance that provides coverage for civil and criminal defense costs and provides for reimbursement of criminal defense costs if such person uses a firearm in self defense.”

Failure to maintain the required insurance would be “Class A” misdemeanor. The provisions would not apply to those who possess a firearm on a temporary basis while on the premises of a gun club.

Under the measure, the state’s insurance commissioner would adopt regulations to implement the provisions, including minimum coverage amounts of such insurance policies, form and filing requirements and any permissible exclusions.

The bill, however, died in the Insurance Committee after a public hearing on March 19, The Connecticut Post reported. Some 30 people testified at the hearing, almost all of whom criticized the proposal as flawed. Some also questioned the constitutionality of the proposal, suggesting that even if the bill were to pass, it may get struck down as unconstitutional by a court of law.

The Connecticut Insurance Department said it offered no testimony on HB 6656 and declined to comment further.

Maryland

In Maryland, Senate Bill 577 (Public Safety – Firearms – Liability Insurance Requirement) was introduced by State Senators Jamie Raskin (D-Montgomery County) and Bill Ferguson (D-Baltimore City) in February. The bill, however, has died, the Office of Sen. Raskin told Insurance Journal.

The bill had proposed that a person that possesses a firearm shall maintain liability insurance that provides coverage of at least $250,000 for accidental injuries caused by the firearm. A fine not exceeding $1,000 could be assessed for those found in violation of the insurance requirement. Under the measure, anyone who sells, rents or transfers firearms were to check insurance coverage for their potential customers.

The Maryland Insurance Administration said it did not submit testimony and offered no further comment on the proposal.

Pennsylvania

In the Pennsylvania House of Representatives, House Bill 521 (Amending Title 18, Crimes and Offenses, of the Pennsylvania Consolidated Statutes, in firearms and other dangerous articles, further providing for licenses.) was introduced in February, with State Rep. Ronald Waters (D-191) as its prime sponsor.

In a memo for House Bill 521, Rep. Waters remarked that “individuals are currently required to purchase auto insurance in Pennsylvania, and firearm insurance would be in a similar risk management category.”

Individuals who are injured as a result of a firearm would have their medical bills covered under the firearms’ liability insurance. The liability insurance would also cover any civil judgments against the gun owner that may arise out of the use of a firearm.

The bill specifically requires individuals to obtain firearm liability insurance if they possess a license to carry a firearm. The policy would be in an amount of at least $1 million and satisfy any judgment for “personal injuries or property damages arising out of negligent or willful acts involving the use of an insured firearm.”

The policy would not cover unlawful acts committed with the firearm.

The Pennsylvania bill was referred to the state’s House Judiciary Committee in February.

“We have not taken a position on that particular bill, nor have we queried the industry regarding its potential impact,” Pennsylvania insurance department spokesperson Rosanne Placey said.

“However,” she added, “mandating any coverage does not automatically create an appetite for insurers to provide that coverage. Regarding anything new, it does take the industry time to do the proper risk assessments.”

Washington, D.C.

In the Council of the District of Columbia, Councilmember Mary Cheh (D-Ward 3) introduced “Firearm Insurance Amendment Act of 2013” in March, as a way to compensate gunshot victims for injuries and also help promote firearm safety.

The bill proposes that anyone in the District who owns a firearm shall maintain liability insurance in an amount of no less than $250,000. It also requires that the policy specifically cover “any damages resulting from negligent acts, or willful acts that are not undertaken in self-defense, involving the use of the insured firearm while it is owned by the policyholder.”

Failure to maintain an insurance policy as required would result in the immediate revocation of a firearm owner’s registration and license.

The bill has been referred to the Committee on the Judiciary and Public Safety to schedule a future hearing.

Illinois

Most of the weapons-related measures introduced in state legislatures in the country’s middle section this year would expand the rights of lawful gun owners. One exception is Illinois, which according to the Law Center to Prevent Gun Violence, has some of the strongest gun laws in the country, and certainly the strongest of all the Middle America states. Illinois does not allow the carrying of concealed handguns in public.

In addition to HB 1155, which was rejected by the House, State Rep. Kenneth Dunkin introduced HB 2589, which would amend the Firearm Owners Identification Card Act to require any firearm owner in the state to maintain a liability insurance policy with a minimum limit of $1 million to cover “any damages resulting from negligent or willful acts involving the use of the firearm while it is owned by that person.”

After being heard by the firearms committee, however, HB 2589 was returned to the rules committee on March 22, where it remains.

California

Keeping track of gun laws is a difficult prospect. In a state like California, for example, if you type in the word “gun” in a search for state legislation you’ll get roughly 20 bills, many of those aimed in one way or another at curbing gun violence, making it harder to obtain firearms, or imposing new taxes or liabilities on gun and gun shop owners.

On the insurance side, Assemblyman Philip Y. Ting, D–San Francisco, and Assemblyman Jimmy Gomez, D–Los Angeles, introduced Assembly Bill 231, which would require gun owners to purchase liability insurance to cover the cost of damages caused by the weapon.

The bill is currently awaiting a hearing in the Assembly Public Safety Committee.

Unintended Consequences

In crafting the gun liability bills, lawmakers in many cases are responding to mass shootings such as those that occurred at Sandy Hook Elementary in Newtown, Conn., and in an Aurora, Colo., movie theater last year.

Some industry observers said that while these bills are well-meaning, mandatory insurance may not be the best way to address the problem of gun-related violence.

“This whole debate about gun liability was triggered by the Sandy Hook event, also the event in Colorado,” said Insurance Information Institute President Dr. Robert P. Hartwig, “both of which were illegal and neither of which would be covered under any policy ever written in the history of the insurance industry.”

“I think you have a situation where legislators are casting about for what look like solutions, what might be solutions. I think some people are attracted to alternatives to direct government regulations of firearms,” said Robert Detlefsen, vice president of policy affairs at the National Association of Mutual Insurance Companies.

He said proponents of these bills often compare guns to automobiles – nearly every state requires drivers to carry auto liability insurance because cars can harm others if operated negligently or otherwise improperly.

Proponents of these measures say gun owners, like motorists, should also be required to purchase liability insurance. However, Detlefsen said, unlike driving a car, owning a gun is constitutionally protected – which means a law that conditions the exercise of a constitutional right on buying liability insurance probably would not survive judicial scrutiny.

Also, those with illegal guns are unlikely to comply with the insurance rules, making the law rather ineffective.

James Harrington, executive director at the Massachusetts Insurance Federation, also expressed concern.

“It appears to me that the feeling among those advocating mandatory gun ownership liability coverage is that if it was there, it would translate into more responsible behavior. We don’t necessarily agree with that premise,” he said. “In fact, we conclude that the potential may exist that it would unintentionally or inadvertently encourage poor behavior in terms of gun usage.”

Another potential problem is that anytime there is mandatory insurance legislation, if the government isn’t satisfied as to the pricing or the availability of the product, “then, more often than not, they look at creating a residual market.”

“We would be very fearful that any jurisdictions that enact mandatory, compulsory gun ownership liability insurance would seek to create some type of residual markets or pooling or assigned risk plans, which is another reason we strongly oppose any such provision,” Harrington said.

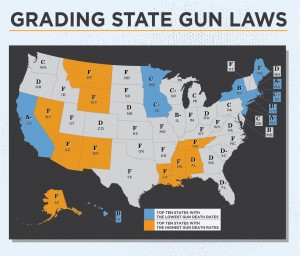

Grading States on Gun Control

According to the Law Center to Prevent Gun Violence, a group that advocates for stricter gun control, roughly 1,140 bills concerning guns have been introduced in the United States so far in 2013.

“We’ve seen a significant increase over last year, especially in bills to strengthen gun violence prevention,” said Benjamin Van Houten, managing attorney for the group.

The group estimates that the number of bills that would “strengthen gun violence protection,” 600 bills by its count, rose 63 percent over the same time last year. About 540 “weakening bills” have been introduced, according to the group.

Among the most popular bills introduced are: access to firearms by dangerously mentally ill (bills related to this have been introduced in 23 states); assault weapons (22 states); large capacity ammunition magazines (20 states); and background checks on some or all private sales (18 states), according to the Law Center.

Existing laws by state vary. The Law Center to Prevent Gun Violence has a state by state grading system.

The group gives California an “A-,” while Western states like Alaska, Arizona, Idaho, Nevada, Montana, New Mexico, Utah and Wyoming earned an “F.” Oregon and Colorado got a “D,” while Washington was given a “C,” and Hawaii was given a “B.”

The only other states to earn an “A-” were New Jersey and Massachusetts.

In the Midwest, Illinois rated a “B-.” Minnesota and Michigan received “C” grades, while Iowa and Wisconsin both got a “C-.”

All four South Central states – Arkansas, Louisiana, Oklahoma and Texas – received “F”s under the grading system.

Among the Southeast states, Tennessee and North Carolina received “F”s; “D”s were assigned to Alabama and Georgia.

Insurance Journal’s Stephanie K. Jones contributed to this report.

Topics California Legislation New York Washington Illinois Massachusetts Maryland Pennsylvania Connecticut

Was this article valuable?

Here are more articles you may enjoy.

eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million

eBay Settles Couple’s Harassment, Stalking Claims for $55.7 Million  Company at Center of Cyclospora Outbreak Complained to White House, Source Says

Company at Center of Cyclospora Outbreak Complained to White House, Source Says  Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers

Why El Niño’s Promise of Quieter Hurricane Season May Not Be Good News for Insurers  Trump’s Diversity Crackdown Reverberates Through US Boardrooms

Trump’s Diversity Crackdown Reverberates Through US Boardrooms