Independent agency owners spend their entire careers worrying about the risks and exposures of others. Managing the risks of their own agencies can take a backseat to helping their clients.

While agents appreciate the importance of errors and omissions (E&O) coverage and the need for a strong risk management approach, they are at times “a little like the childhood fable of the cobbler’s children having no shoes,” says Mark Angelucci, resident senior vice president and E&O segment leader, Utica National Insurance Group.

“They are so focused on their clients’ insurance needs that they can neglect their own,” Angelucci said.

Many agents treat their clients better than they do themselves.

Agents E&O is “vital to protecting the agency’s hard earned assets and reputation,” according to Sabrena Sally, senior vice president, Westport Insurance Corp., which serves as an underwriting carrier for the Big “I’s” Professional Liability Program.

“In the same way agencies recommend their customers periodically assess their risks, agencies too should review their E&O coverage versus their exposure,” Sally said.

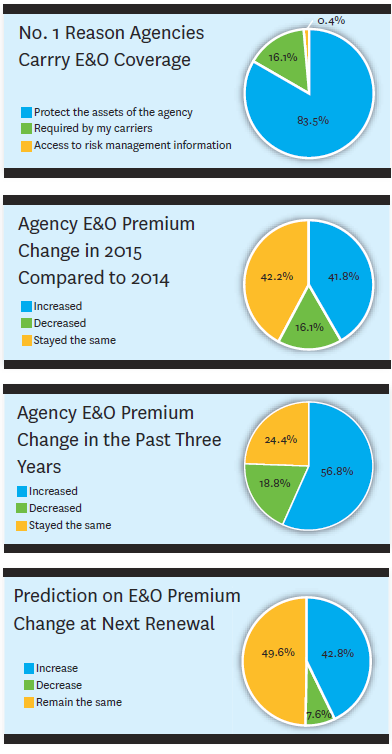

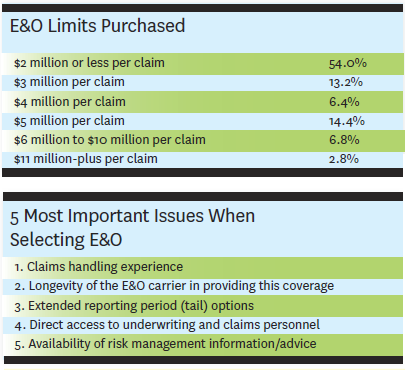

According to Insurance Journal‘s 2016 Agency E&O Survey, the majority (83.5 percent) of agency owners purchase E&O coverage to protect their agency’s assets.

Agents should be alert to many of the same issues they weigh when they are recommending coverages for their clients. “Coverage terms and limits relevant to the exposures of the agency’s operations, the experience of the carrier in the agent’s E&O space, the reputation of the carrier’s claims team, the longevity and stability of the association program through which the coverage is being purchased – all of these are important considerations when purchasing agency E&O,” Sally said.

According to Sally, there are certain questions agency owners should be asking at the time of purchasing insurance: “Has their agency experienced growth? Has their customer base changed to include insuring higher values and limits or customers with higher exposures? Has the ownership structure of the agency changed to one which might prefer higher limits?”

Also, has the agency moved from a sole proprietor to a partnership or incorporated with multiple owners?

Angelucci believes that a good relationship with their E&O underwriter can provide agents with additional coverage and limits options that might have been overlooked.

In addition to buying the right agency E&O coverage, agents must stay focused on risk management within their agencies — just as they tell their clients to implement workplace safety measures and adopt best practices.

Knowledge and Time

Coverage knowledge is one area where agencies can always strengthen themselves and their employees, says Chris Burand, founder and owner of Burand & Associates LLC, based in Pueblo, Colo., which provides agency management consulting services including agency E&O exposure reviews.

Agencies are still being sued for failure to provide the right coverage to insureds, and often this occurs with less experienced agency staff, he said. Some agents just don’t know their coverages well enough. “It’s not only that they don’t understand their coverages, they also don’t understand what coverages their clients often need,” Burand adds. “I see that a lot.”

Burand says that while continuing education is important, so is putting in the time and effort needed to properly address the needs of every client and eliminate this E&O exposure.

The best agents are good at thoroughly understanding what their clients’ needs are, he says, and they take the time – make the time – to find out what those needs are. “They really do a good job of searching the marketplace for the policies that fit those needs closest,” Burand says.

Westport’s Sally believes agencies are becoming more knowledgeable about the coverages available for their customers and are using technology to increase efficiency in providing that coverage. But in her view, where agencies struggle the most is in finding a consistent balance in their workload.

“The struggle remains in balancing the need to perform all transactions the same way every time, and to document each transaction, balancing that against being customer friendly, and managing the daily work flow,” she said. “For example, the ‘best’ documentation would consist of a detailed analysis of a commercial customer’s exposures, insurance options to address each one, with the customer signing off on declined coverages.”

In theory that approach is best, but Sally understands the real-world environment and that demands placed on today’s independent agents make that practice difficult. “In a business that is still relationship based, this is not always achievable,” she said. “In addition, we are human beings. The best processes and procedures are still prone to human error.”

Best Defenses

Proper documentation, consistent policies and procedures and coverage knowledge are an agent’s best defenses when it comes to E&O, the experts agree.

For years, the leading cause of claims against agents has been lack of coverage or inadequate coverage. “Failure to procure coverage, obtain coverage in adequate limits – it’s the knowledge-based errors that make up half of all the errors in an agency,” said Mark Wolf, vice president for Big “I” Advantage.

“You’ve got the general errors that people make. They just make mistakes. They don’t place the coverage. They don’t check to make sure an excess policy is follow form,” Wolf said. Mistakes happen and that’s why agency E&O coverage is there to respond.

Then, there are the knowledge-based errors, Wolf said, which can be avoided. The best way to combat these is to specialize, Wolf said.

“You really need to be a specialist in today’s world,” Wolf said. Specialists know the market, know the coverages available, and can potentially avoid knowledge-based errors, he adds.

“Specialists, especially in certain coverage areas, are definitely a much better risk,” he said. “People that dabble are going to have claims and if you’re dabbling in something that has high-severity risks, you’re going to be looking at very large claims.”

Mark D. Harris is president and CEO of Quadrant Insurance Managers, a national program administrator, managing general agency and wholesaler based in Westerville, Ohio, that has been writing agency E&O programs since 1989. Harris says larger agencies may face different E&O problems than their smaller counterparts.

“Small agents may struggle with obtaining and properly documenting coverage rejections from a client – for example, rejections of flood and excess flood insurance,” Harris said. “So there needs to be a procedure that demands client acceptance or rejection of the terms offered, as well as certain disclaimers and warranties on every proposal to protect themselves. It’s a tall order and for small agencies it will be really hard,” Harris admits. But those kinds of policies and procedures protect agencies from E&O claims, he said.

Harris says agencies that excel in E&O risk management have management that insists on excellence in product delivery and is always involved in the process, he says.

Staff stability is also important. “We have seen E&O losses follow staff turnover or when they experience difficulty replacing staff. Oftentimes, management focus is on something other than quality or client satisfaction, like driving revenue,” Harris said.

All agencies must drive revenue but not at the expense of agency E&O, he added.

Technology Helps

Technology makes E&O risk management easier today. If used properly, technology can also be an agency’s best defense in an E&O situation, Harris said.

Agency management systems allow agencies to more readily verify that policies and procedures are adhered to, according to Harris. But technology can also be a double-edged sword, offering a place to store documentation but also asking it obvious if an agency promises to do something and doesn’t fulfill that promise.

Technology can help if a claim ends up in E&O litigation, says Bob McCabe, partner at Houston-based law firm Thompson Coe, which specializes in agency E&O coverage litigation.

“Technology certainly makes it easier to track things when people are utilizing agency management systems,” McCabe said. Files are better managed than they were in years past, he said.

Agencies could improve their storing of emails to and from clients, making sure that these emails make it into the agency management systems, McCabe advised.

“I find a lot of times there may be a function where if you send me an email then I’ve got to get that email into the file once I receive it and a lot of people don’t and instead leave it in their inbox or delete it. Then we have to drag it out later,” he said.

The best E&O defense is about being able to document conversations and being able to show that documentation later, McCabe said.

“By and large most agents are doing a good job and are doing what they should do. But when someone has a claim that doesn’t get paid because of a policy exclusion or policy that expired or a piece of property wasn’t scheduled, or something else, the insured will oftentimes say they didn’t discuss that with their agent, or was told something else. Proper documentation and saving those email conversations will get agents away from the ‘he said, she said’ problem. “The more things I have in my favor to back up what the client (agent) said, the better chance I have to convince a jury,” McCabe added.

Signed Applications

Westport’s Sally warns about an increasing number of claims stemming from carriers’ use of online application processes that do not require an affirmative signature of the applicant prior to binding coverage. “Unless the agency takes steps to document their file regarding the application information represented by the customer, the agency may face a classic ‘he said, she said’ situation should an E&O claim arise and there is no signed application in the file,” Sally said.

Angelucci has seen court cases involving agent’s or insured’s material misrepresentations (from the carrier’s perspective) with the carrier bringing an action against the agent for the value of the claim.

“Obtaining signed applications, use of exposure checklists and being thorough in understanding a client’s operation are the best way to avoid these types of claims,” Angelucci said.

Technology Hurts

Technology can also contribute to E&O concerns. The 2016 Agency E&O survey respondents listed privacy and cyber-related exposure as areas where they feel most vulnerable to an E&O claim.

One agency owner wrote: “The interplay between the E&O policy, technology E&O, and cyber/privacy coverage will be important as more agencies diversify the method in which they interact with clients/carriers.”

“We feel it’s a major area of concern,” Harris said. “There is always the possibility that absent an exclusion and, sometimes with an exclusion, a court could find coverage for cyber in the E&O policy.”

Most agency E&O policies have exclusions for cyber or will have “throw-in” coverage.

“Many carriers have gone to a ‘baby cyber policy,'” Harris said, “and add breach coverage but it’s not robust coverage.”

Others put sublimits on cyber coverage. “The real issue is dilution of the limits. If someone is going to put cyber (on an E&O policy) as a throw-in, make sure they are not diluting limits,” he said.

These advisors agree that just as agents tell their clients that cyber exposures are becoming so important that coverage should be on a separate policy, so are they important enough for an agency to have a separate policy. Angelucci advises agents to look for policies that include breach notification services, not just reimbursement for expenses incurred for notification.

Social Media

New E&O exposures are emerging. One is business defamation as it relates to social media, where negative comments made about a competitor are looked at as libelous, according to Utica’s Angelucci.

“The use of social media is becoming an increasing part of how agents interact with their clients,” he said. Agencies need to communicate with clients about the proper way to make requests. “If an action occurs via social media it should be documented in their agency management system.”

Angelucci says an agency must strike a balance when making claims about its agency’s capabilities versus a competitor. n “Factual statements must be used and you must be cautious about any reference to a third party or competitor,” he said.

The most common type of defamation claim in an E&O context concern statements made to clients or prospects. “Social media creates the potential for any statement to be communicated to a much larger audience than a statement made in person,” he noted.

In cases against agents for E&O claims, agency websites and marketing materials (which could include social media posts or blogs) are used as evidence to argue the merit of a claim.

Thus agencies need to be cautious about making any statements, especially unflattering ones, about others on social media. “This is where a well written social media policy for agency employees is important,” Angelucci said.

Angelucci offered the following tips for a good staff social media policy:

- Lay out which social media tools are acceptable or not acceptable for business use.

- Detail the need to be careful about disclosing confidential customer information on any social media sites.

- Be sure that everyone who may use social media sites for the company understands the behavioral expectations when communicating in this forum (respectful, honest, accurate, etc.).

- Determine what correspondence or requests the agency will accept from customers or prospective customers with these tools and how to properly document and handle them.

“For example, will you take an endorsement request via a Facebook posting? If so, do you expect a screen shot of the request to be copied to the customer’s file in your agency management system? Or will your agency not accept any requests except via phone call or written correspondence? Expectations need to be specifically laid out in either situation,” Angelucci said.

The complete 2016 Agency E&O Survey is available from Insurance Journal’s Research and Trends division. Insurance Journal thanks Demotech Inc., its official research partner, for providing analysis once again for this year’s survey.The survey obtained responses from 297 agency owners across the country from Sept. 26, 2016 to Oct. 21, 2016. This article is an edited and abbreviated version of an article that originally appeared in Insurance Journal print magazine.

Was this article valuable?

Here are more articles you may enjoy.

Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  ‘Tow Godz’ and Auto Glass Businessmen Charged in Carolina Fraud Schemes

‘Tow Godz’ and Auto Glass Businessmen Charged in Carolina Fraud Schemes  NYC Mayor Mamdani’s Rent Freeze Heaps Pressure on a Teetering CMBS Deal

NYC Mayor Mamdani’s Rent Freeze Heaps Pressure on a Teetering CMBS Deal