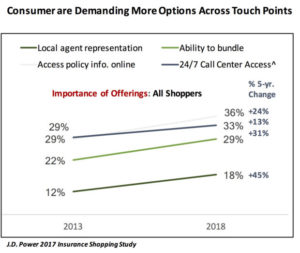

Auto insurance shoppers are placing a greater importance on having more services provided to them today versus five years ago, underscoring the fact that shoppers are increasingly demanding more product options and more and different ways to connect with their insurer, according to the J.D. Power 2018 Insurance Shopping Study.

The study also found that representation by a local agent has increased in importance the most over the past five years (45 percent) compared to other touch points, and “reliance on agents” was especially true among first-time shoppers.

The J.D. Power 2017 Large Commercial Study also found 34 percent of the risk managers who responded to the survey based their buying decisions on their agent’s recommendations, while 38 percent of the small commercial buyers, as reported in the J.D. Power 2017 Small Commercial Satisfaction Study, looked to their agent to recommend a carrier.

These findings suggest that agents still have a vital role in providing expertise and guidance throughout the sales, onboarding and servicing of both personal and commercial insurance policies.

The importance of the agent, direct or independent, from a customer perspective, is not only evident during the buying process but also throughout the life cycle of a customer’s experience with a carrier. What the 2018 J.D. Power studies (both shopping and claims) found was that the customer is more likely to look to their agent for advice, counsel and support when dealing with insurance matters over any other resource such as a carrier’s call center or website. This need on the part of customers is key to the survival and growth of the agency system in the United States.

Regardless of the advancements in technology, there is still a strong need for a personal connection, even if that connection is manifested through a digital pathway between a customer and an insurance professional. Customers want access to policy information and other services 24/7, and they look to online access for much of this information. However, in terms of making key decisions and getting support for such activities as reporting a claim, customers want to deal with a person who can answer questions, offer empathy and instill a level of confidence that the customer is doing the right thing or making the right decision.

Regardless of the advancements in technology, there is still a strong need for a personal connection, even if that connection is manifested through a digital pathway between a customer and an insurance professional. Customers want access to policy information and other services 24/7, and they look to online access for much of this information. However, in terms of making key decisions and getting support for such activities as reporting a claim, customers want to deal with a person who can answer questions, offer empathy and instill a level of confidence that the customer is doing the right thing or making the right decision.

Given the development of artificial intelligence (AI), customers may likely be able to have a fully digital interaction with their carrier in the future using chatbot or even more advanced technology to replicate the personal interaction. But for the foreseeable future, customers—even the youngest cohorts—are not willing to give up that personal connection, especially when reporting a claim, and it is up to carriers and agents to foster a customer experience to match rapidly changing consumer expectations.

Carrier vs. Agent Priorities

Historically, agents and carriers have touted their support for each other, but in reality both groups generally have different priorities:

- They don’t communicate effectively.

- Carriers have been pushing for greater access to customers without any real coordination with agents.

- Carriers are notorious for disrupting relationships with their agents by making unilateral decisions.

- Agents are more likely to use carriers to block markets or test quotes against incumbents with no real intent of moving business.

If these practices continue, the ability of both carriers and agents to meet customer expectations over the long term is suspect.

Carriers and agents working to improve the customer experience without involving each other may have short-term successes. In the long term, however, they will likely open the market for more disruptions from the continued growth of the InsurTech sector or even from other innovators such as Amazon, Walmart and possibly banks that have moved much further in the development of their mobile capabilities than most insurance carriers.

To elevate the relationship to a level that customers expect, carriers and agents must find a way to integrate their interactions with customers into a single conversation instead of disjointed transactions where customers must repeat themselves because different entities within the insurance company and the agency are not using the same information.

To achieve a single conversation, carriers and agents need to digitize routine matters, eliminate the need for multiple workflows and access points, and there must be a reconnection between agents and carriers that allows agents to truly act on behalf of their carriers. Achieving these kinds of improvements must begin by simply communicating with each other.

Good Communication

The first and most critical step for agents and carriers is focused, honest and cooperative communications. As with any good collaborative effort, communication must be two-way, with each party genuinely listening to the other.

Findings of the J.D. Power 2018 Independent Agent Study show that greater communications and training have a strong effect on the overall satisfaction level of agents. Increasing the communication and support a carrier provides to its agents shows an improvement in agent satisfaction of more than 200 points (on a 1,000-point scale) among both commercial and personal agents.

Agent satisfaction is even higher when the carrier provides ongoing and regular training or support sessions throughout the year.

Without regular and clear agency/carrier communications and ongoing carrier support (training and development), the kind of customer experience carriers and agents need to provide is highly suspect.

To achieve a more lasting and sustainable relationship between carrier and agent, both will need to better align their resources. In other words, agents should align themselves with carriers that target the markets the agent services, offer the broadest products for the agent’s markets, and are willing to have an integrated digital footprint that supports the agency and the customers being serviced.

For carriers, their agency forces must be aligned with their targeted markets, be a part of the carrier’s integrated processes, and work within a reasonable and sustainable commission structure. They should also support a profit-sharing plan that is based on long-term profitability.

The agent’s role is still vital to the insurance process, but that role and the carrier’s ability to reach and sustain higher levels of customer satisfaction will be tested.

Agents and carriers must better align their digital strategies and clearly design a division of work that allows the agents to focus more on being an adviser throughout the life cycle of the policy. Carriers must be willing to provide a stable and sustainable marketplace. Finally, agents and carriers must agree on a long-term, sustainable compensation system that supports both growth and profit.

This transformation must come sooner rather than later, and the customer must be at the center of every action taken by both the agents and carriers.

This article was originally published by Wells Media Group’s Carrier Management, the publication for property/casualty insurance executives.

Topics InsurTech Carriers Agencies Tech Training Development

Was this article valuable?

Here are more articles you may enjoy.

NYC Halts Construction at 222 Broadway Office-to-Residence Tower

NYC Halts Construction at 222 Broadway Office-to-Residence Tower  After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed  Company at Center of Cyclospora Outbreak Complained to White House, Source Says

Company at Center of Cyclospora Outbreak Complained to White House, Source Says  Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver