In 2022, the U.S. private auto insurance industry reported its worst underwriting results in over two decades, according to a S&P Global Market Intelligence analysis.

The net combined ratio for the sector — when excluding policyholder dividends — was 111.8. That figure was 11 points higher than 2021’s ratio.

The 2022 net combined ratio topped the previous high of the past 27 years — 110.4 seen in 2000 — according to the S&P review of available annual regulatory statements.

The motor vehicle insurance consumer price index soared by 15.5% year-over-year in April — more than three times the overall CPI, and the highest such increase since 1977, when adjusting for the one-time impact of COVID-19 premium rebates.

“Because underwriting results were so poor in 2022, consumers can expect to see significant increases in their higher auto insurance premiums for at least the balance of 2023, and in some cases, into 2024,” said Tim Zawacki, Principal Insurance Analyst, S&P Global Market Intelligence.

Key Highlights from the Analysis

- While rising premium rates have yet to catch up to the losses insurers are sustaining, S&P Global Market Intelligence projected in October 2022 that the business line should be close to breakeven in 2024 and see a sub-100% combined ratio in 2025 and 2026.

- Total net underwriting expenses were down for the second year in a row to $58.05 billion in 2022, compared to $58.33 billion and $59.03 billion in 2021 and 2020, respectively. Lower expenses and higher sequential net premiums written pushed the industry’s expense ratio to 21.7%, the lowest annual expense ratio since 1996.

- Higher net premiums earned through rate increases during 2022 were not enough to overcome the increased claims cost the insurers faced during the year. The rising costs were spread across both private auto physical damage and liabilities coverages.

- The total dollar amount of incurred losses for physical damage and the combined liability lines of business increased by 23.3% and 23.7%, respectively, year-over-year in 2022, while net premiums earned only increased by 6.4% and 3.4%, respectively. Inflation and unfavorable reserve development pushed the net incurred loss ratio to 79.8% in 2022, considerably worse than the previous high of 70.9% in 2000 and the 67.6% seen in 2021.

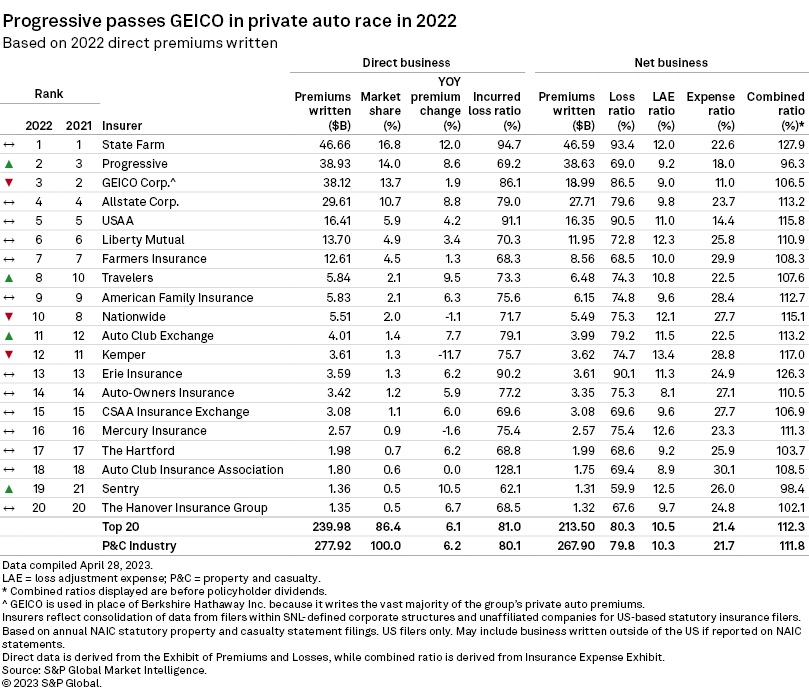

Progressive Slides into Second

State Farm reported a private auto combined ratio of 127.9% in 2022, which was the highest ratio among the 20 largest private auto underwriters.

S&P said State Farm remained the largest U.S. private auto insurer based on 2022 direct premiums written, but among notable changes to the top 20 was Progressive’s move ahead of GEICO into second place. Progressive was one of two auto insurers with a combined ratio below 100 in 2022.

Also, Travelers and Nationwide switched spots from the prior year.

Topics Auto

Was this article valuable?

Here are more articles you may enjoy.

Zurich CEO Says Staff Let Go as Regulator Finma Imposes Partial Sales Ban

Zurich CEO Says Staff Let Go as Regulator Finma Imposes Partial Sales Ban  Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks  CBIZ Brokerage to Be Spun Off, Backed by Private Equity, After $5B Grant Thornton Deal

CBIZ Brokerage to Be Spun Off, Backed by Private Equity, After $5B Grant Thornton Deal