The hurricane season is officially over, but it didn’t go by without leaving a major mark on Florida and its insurance industry.

Hurricane Irma, a name most in the state won’t soon forget, first hit the Florida Keys as a category 4 storm on Sunday, Sept. 10, with 130-mile per hour winds. It then worked its way north passing over the east and west coasts.

Loss estimates from Hurricane Irma have ranged between $25 billion to $65 billion by catastrophe modelers. The Florida Office of Insurance Regulation (OIR) reported total estimated insured losses at more than $5.8 billion as of Nov. 13, with more than 689,000 residential property claims and 51,396 commercial property claims. Business interruption claims reached more than 3,700 as of Nov. 3.

In the immediate aftermath of the storm, 6.7 million homes and businesses — about 65 percent of the state — were without power.

The Florida Hurricane Catastrophe Fund said the state fund that provides backing to private insurers would pay about $5.1 billion in claims. Florida estimated it had spent nearly $650 million on emergency resources and clean up from the storm.

Florida’s state-run insurer of last resort, Citizens, expects $1.2 billion in insured losses and 70,000 Hurricane Irma claims over the next 18-24 months. The carrier said Nov. 29 it had closed nearly two-thirds of the 62,000 claims it had seen so far, including more than 42,400 claims in Miami-Dade, Broward and Monroe counties.

The damage to Florida crops was also epic. According to The Associated Press, Florida Agriculture Commissioner Adam Putnam said Irma’s path couldn’t have been “more lethal” for Florida agriculture, with few crops spared. More than half of the state’s iconic orange crop is estimated to be lost.

Could Have Been Worse

Hurricane Irma will go down as one of the top hurricanes in Florida history, but experts say it could have been worse.

As the storm tracked towards Florida in early September, some estimates put the cost of damage from Irma as high as $200 billion. But something called the “Bermuda High,” threw the hurricane slightly off course, sparing the most populated area of South Florida from the brunt of the storm. Bloomberg reported that the circular system hovering over Bermuda “jostled Irma onto Northern Cuba … where being over land sapped it of some power.”

Florida escaped the worst because “Irma’s powerful eye shifted westward, away from the biggest population center of Miami-Dade County,” Bloomberg said.

“The fact that it took a left turn at the last minute and didn’t give Miami a punch in the nose was a blessing,” said Marsh US Property Practice Leader Duncan Ellis.

Recovery Ongoing

Still, Irma did pack a powerful punch and the recovery will go on for some time. Companies are now working on getting insureds back on their feet.

One of the biggest issues in the aftermath of Irma has been a shortage of claims adjusters. The storm came just two weeks after Hurricane Harvey hit Texas and the industry has scrambled to bring in adjusters, leading to delays in resolving claims.

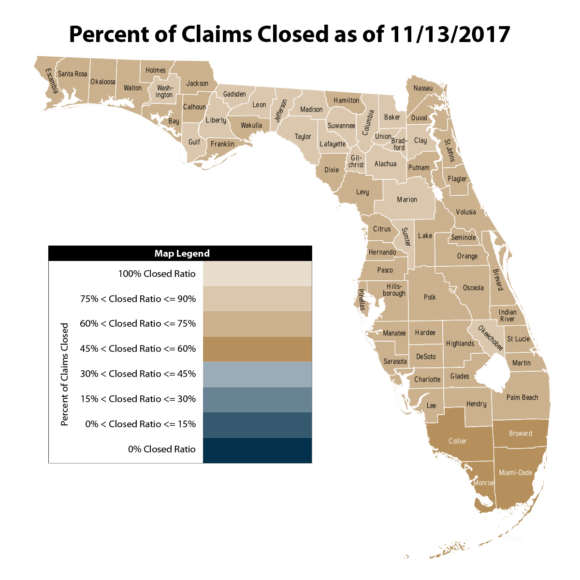

OIR reported in its Nov. 13 claims data that about 235,759 residential property claims reported to insurers remained open. The percentage of commercial property claims closed was 29.5 percent.

“The biggest challenge is you get a backlog when catastrophes hit like this. [Hurricane Harvey] was so close to what happened in Florida,” said Bobby Raymond, owner of Jacksonville, Fla.-based Brightway, The Fort Caroline Agency. “There’s a limited pool of claims adjusters in the universe. We’ve warned clients carriers are doing the best they can, but they [could] take a while to get back to you.”

Raymond himself couldn’t get a claims adjuster out for almost a month after Irma caused two trees to fall on homes he owns. “That’s just typical,” he said.

Carriers have turned to technology, such as drones, to help with assessing claims.

EagleView, an aerial imagery provider, does inspections for insurance companies, including roof and structure damage, and property damage measurements. Kenneth Cook, SVP of EagleView OnSite Solutions, said its drone technology has handled thousands of Irma claims for insurers.

“It’s a new method for them to get their work done. After any kind of a storm event — especially with two major events back to back — insurance adjusters are busy around the country, and insurance companies are always looking for faster more efficient ways to help customers,” Cook said.

EagleView contracts with drone hobbyists and provides them with insurance certification training, including how to inspect a home for claims purposes. In some areas of Florida that were impacted by Irma, Cook said drones were not a good solution because of structural damage, but in other areas drones can capture detailed images of damage like missing shingles, fences blown down, or missing roof tiles.

“There are thousands of claims that drones are perfect for because in just 25 minutes the pictures are taken and uploaded, saving the carrier a lot of time,” he said.

New hurricane policies were also put to the test in the aftermath of Hurricane Irma. Policyholders of the new StormPeace product from Assured Risk Cover (ARC) and California-based Topa Insurance Co. were reimbursed right away for hurricane expenses ranging from $1,000 to $15,000.

Alok Jha, CEO and founder of ARC, said about 98 percent of claimants were paid within three days of attesting to an Irma loss.

The StormPeace product uses mobile technology to alert costumers in declared storm areas so they be paid right away for evacuation costs or damage to their homes.

“This product has no exclusions and pays promptly after a hurricane,” Jha said.

A contractor shortage has also delayed recovery efforts. Jake Morin, president of Construction for ProSight Specialty Insurance, said demand has surged for contractors in hurricane-hit areas, and so has demand for coverage. The company is working quickly to get contractors insured so they can help with rebuilding.

“Homeowners and businesses want to make sure they are working with a licensed and reputable contractor,” he said. “There is a flood of contractors trying to capitalize; make sure the work they are doing is the work they need to be doing.”

Lessons Learned

Experts are already looking at whether the state was adequately prepared for Irma and what should be done differently next time.

“Much hard work and preparation over the last few years has paid off during Citizens initial response to Hurricane Irma,” said Chris Gardner, chairman of Citizens’ board of governors, shortly after the storm. “However, given the magnitude of reported claims, we are sure to encounter unforeseen challenges. We will continue to learn, prepare and improve our response capabilities with each storm situation.”

Agency owner Raymond said despite the adjuster shortage, he’s been impressed with how carriers have improved their cat response and capabilities to process large claims volumes since Hurricane Matthew.

“We had less complaints from customers this year about not being able to get through to their carrier,” he said.

Marsh’s Ellis says Irma is a reminder of the importance of adequate insurance coverage, and that agents should take the time now to sit down with their clients and evaluate their coverage needs.

“People forget how significant these events are. It’s an eyeopener for people, especially in the residential space where flood isn’t covered,” Ellis said.

ProSight’s Morin agrees.

“Insurance is one of those items that you buy, but you don’t know what you have until you need it. Customers truly rely on their insurance agent to be their counsel and point them in the right direction and make sure they are covered,” he said.

Doug Wiles, president of Herbie Wiles Insurance Agency in St. Augustine, Fla., said Irma’s aftermath has highlighted the important work that insurance agents do. For instance, he has spent countless hours keeping information flowing between carriers and customers since the storm.

“It can be tough to get through to insurance companies and you are speaking to a different representative each time — it’s not like talking to an old friend or neighbor. The value of an agent at a time like this is incredible,” he said.

He added that the increasing frequency of catastrophes should not be overlooked.

“With the change in our climate, I am concerned we are going to see more of this activity and I am concerned about what that is going to do to the insurance industry, especially for those companies who have focused their business in Florida,” he said. “I think we need to take a careful look at how we spread that risk — and whatever that means to the companies involved.”

Related:

- 2017 Hurricane Season Ranks as Costliest Ever for U.S.

- Florida Insurance Agents Recount Hurricane Irma’s Personal Impact

- Insurers, Reinsurers Tally Maria, Irma, Harvey and Other Disaster Losses

- 4 Hurricane Irma-Affected U.S. Attorney Offices Form Fraud Task Forces

- Florida to Deploy Anti-Fraud Strike Teams to Areas Hard-Hit by Irma

- Lloyd’s Pays Claims of $1.7B for Hurricanes Harvey, Irma; Maria – So Far

- More than 63K Recreational Boats Destroyed by Hurricanes Harvey and Irma

- Irma Dealt Devastating Blow to Florida Citrus, Other Crops

Correction: This story has been updated from an earlier version that incorrectly identified the company Assured Risk Cover (ARC) as Assured Risk Concepts.

Topics Catastrophe Natural Disasters Carriers Florida Claims Agribusiness Property Hurricane Contractors Drones

Was this article valuable?

Here are more articles you may enjoy.

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver  Berry Producer Driscoll’s Sued Over Alleged Greenwashing, Use of Forever Chemicals

Berry Producer Driscoll’s Sued Over Alleged Greenwashing, Use of Forever Chemicals  Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks  Florida Appeals Court Strikes Jury’s $335,000 Award in Universal Plumbing Claim

Florida Appeals Court Strikes Jury’s $335,000 Award in Universal Plumbing Claim