Home fortifications, from roof tie-downs to window protections, have been recognized as key factors in reducing losses, claims and premiums in hurricane-prone states like Florida.

But relying on the incentive of premium discounts is not enough to prompt widespread adoption of mitigation measures, especially for low- and moderate-income households, according to a new study that examined more than 20 years of data from Florida’s Citizens Property Insurance Corp.

“Our findings underscore that rising insurance premiums can increase adaptation, but only if paired with policies that target financial constraints for low-income and low-wealth households,” the study concluded.

The paper was authored by four professors at three universities, including Vikas Soni, assistant professor and director of the Merrill Lynch Wealth Management Center at the University of South Florida. It was published by the Brookings Institution’s Hutchins Center on Fiscal and Monetary Policy.

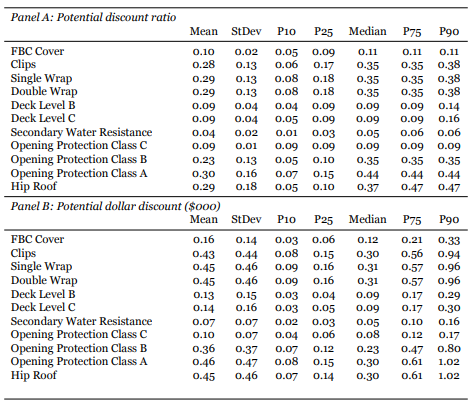

The study acknowledged that the $300 million My Safe Florida Home program, which prioritizes lower-income homeowners, provides state-funded matching grants of up to $10,000 for retrofits, for qualified applicants. And property insurers in Florida offer discounts of as much as 44% for some mitigation steps, such as window and door opening protection. Opening protections and stronger roof-to-wall connections, such as hurricane clips and straps, can provide the largest discounts, amounting to a mean value of about $6,000 over 25 to 30 years, the report indicated.

But the policyholders who need to save the most on homeowners insurance premiums are least likely to pay for protective retrofits, the study found. Wealthier homeowners will respond to higher insurance costs by investing more in climate-resistant building features. The premium discounts—greater for higher-value homes—outweigh the cost of hardening work.

“In contrast, lower-income households and those facing higher adaptation costs reduce their investments when premiums rise—premium increases tighten an already binding budget constraint, crowding out the upfront expenditures required for adaptation,” the authors wrote.

Changes in public and insurance industry policy could help, they said. The My Safe Florida Home program, similar to mitigation grant programs in other states, offers one template, the study said. But others are needed, including targeted subsidies for upgrades, more low-interest financing for home retrofits, and means-tested premium assistance programs that preserve the incentive to adapt while relieving financial strain.

The study was posted the same day another report found that property insurance rates are expected to more than triple in some parts of the country over the next decade.

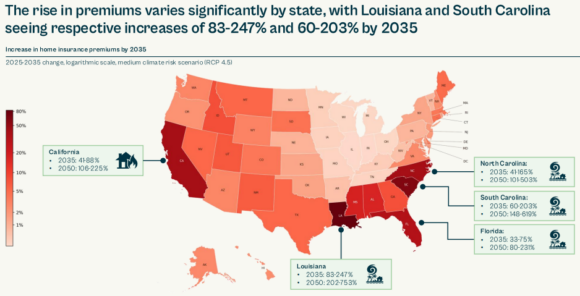

Louisiana and South Carolina will see the steepest average premium increases by the year 2035—as much as 203% for South Carolina and 247% for Louisiana properties, said the study published by the Coalition for an Insurable Future and Mandala Partners. The results of the study were based on data from the Federal Emergency Management Agency, the Federal Insurance Office and other sources and studies.

The report argued that climate change is a growing threat to insurers and insureds, and California and most Southeastern states are most at risk for spiking costs and losses.

“Without action, climate risk will push premiums higher and leave more households without cover, creating significant costs for the economy,” the report noted.

Rates will vary greatly inside states: Low-lying coastal areas in Louisiana, South Carolina as well as North Carolina are the most vulnerable. Hyde County in eastern North Carolina, for example, will likely see average homeowner premium increases of 709% to 5,900% (as much as $101,000) by 2035, the report predicted.

Florida, which has seen its share of soaring property insurance premiums in recent years, followed by moderate rate decreases in 2025 and 2026, may be slightly less affected than neighboring states in the years to come. Indian River and Gulf counties will likely see the sharpest increases in premiums, of about 20% by 2035, under a “medium increase” scenario.

The authors urged action to reduce the impact of climate change on the most vulnerable areas.

“States are taking actions to address the crisis, but effectiveness is mixed and the burden falls primarily on homeowners, insurers, and taxpayers rather than the sources of the underlying climate risk,” the report reads.

Correction: Economist Carolyn Kousky is a member of the Coalition for an Insurable Future but did not lead the study.

Topics Trends

Was this article valuable?

Here are more articles you may enjoy.

Models Stripped of Insurance Cover for Club’s Unauthorized Use of Their Images

Models Stripped of Insurance Cover for Club’s Unauthorized Use of Their Images  NYC Says Source of Legionnaires’ Disease Has Been Eliminated

NYC Says Source of Legionnaires’ Disease Has Been Eliminated  Majority of Small Business Are Underinsured as Other Expenses Prioritized

Majority of Small Business Are Underinsured as Other Expenses Prioritized  Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal

Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal