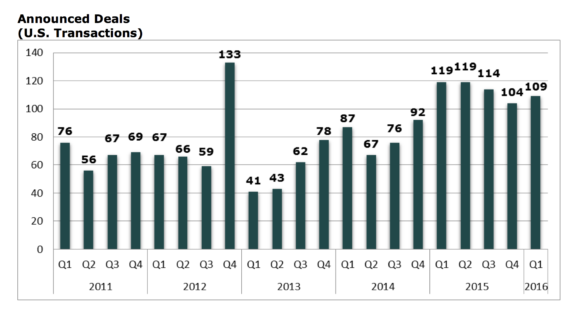

Deal count for the first quarter of 2016 was down slightly relative to the record-breaking first quarter of 2015, but was still the second most active first quarter in the past 10 years. There were 109 announced transactions in the first quarter of 2016 compared with 119 announced transactions in the same timeframe of 2015 (a decrease of 8.4 percent). Some 44 transactions closed in January, 24 in February and 41 transactions occurred in March. By comparison, historical first quarter deal counts over the last five years were 67 in 2012, 41 in 2013, 87 in 2014, 119 in 2015, and 109 in 2016 (average of 84.6 per year).

For the first quarter of 2016, 46 percent of all acquired agencies were property/casualty (P/C) firms, 42 percent were multi-line agencies and 12 percent were employee benefits firms. Specialty distributors made up 24 percent of the total deal activity year-to-date. This is a slight increase from 23 percent recorded in 2015 and 20 percent in 2014 for the same time period.

Private-equity backed buyers were once again the most active acquirers with 53 closed transactions (compared to 55 in the first quarter of 2015). This represented 48.6 percent of all deal activity in the first quarter of 2016. Independent agencies completed 33 transactions and public brokers accounted for 10 transactions over the same time period. Insurance companies, banks and other buyers closed 13 deals in 2016.

The top five buyers for the year represented 33 percent of total deal activity through the first quarter of 2016 and the top 10 accounted for 43.1 percent. Once again, AssuredPartners Inc. was the most active acquirer with 11 announced U.S.-based transactions. AssuredPartners acquisitions were evenly spread throughout the country.

Hub International Limited was the second most active buyer with nine U.S.-based closed transactions in the first quarter of 2016. Hub purchased three agencies in the West, three agencies in the South/Southeast, and two in Midwest/East. Hub continued to expand internationally by purchasing an agency in Canada and one in Puerto Rico.

Arthur J. Gallagher & Co. Inc. was the third most active acquirer and the most active public broker in the marketplace with six deal closings in the first quarter of 2016. Gallagher’s acquisitions were evenly spread throughout the country and consisted of both retail and wholesale agencies.

BroadStreet Partners Inc. and USI Insurance Services LLC both closed five deals in the first quarter of 2016. We have seen that Broadstreet typically applies a co-ownership structure to its acquisitions where agency owners and/or key employees retain some ownership in the agency. Along with P/C retail agencies, USI acquired an employee benefits wholesaler.

Acrisure LLC does not announce all of its deal closings so it is difficult to know exactly how many deals they closed in the first quarter, but they did announce three transactions. Confie Seguros and Hilb Group LLC also announced three deals each. Confie Seguros is mainly a non-standard auto specialist that targets P/C agencies and program administrators. Hilb Group, a private equity-backed broker formed in 2009, has mostly targeted agencies in the Eastern states, Florida and Texas.

There were six buyers that had two deals each: Brown & Brown Inc.; Higginbotham & Associates LLC; Marsh & McLennan Cos. Inc.; Ryan Specialty Group LLC; The Carlyle Group; and World Insurance Associates LLC.

Acquisition activity is down slightly from the ferocious pace set in 2015, but demand appears to remain strong. Private equity-backed brokers continue to be driving the market while public brokers, independent brokers, banks and insurance companies continue to be aggressive in their search for growth and talent.

Was this article valuable?

Here are more articles you may enjoy.

Great American Escapes Coverage for Grocery’s Opioid Litigation Settlement

Great American Escapes Coverage for Grocery’s Opioid Litigation Settlement  Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?

Viewpoint: Who Gets Credit for Successful Renewal During Soft Reinsurance Market?  Trump’s Diversity Crackdown Reverberates Through US Boardrooms

Trump’s Diversity Crackdown Reverberates Through US Boardrooms  As US Residential Solar Industry Craters, Florida Bucks Trend

As US Residential Solar Industry Craters, Florida Bucks Trend

From This Issue