Analysts at the AM Best ratings firm say their initial stress tests of insurance companies globally to gauge the preliminary impact from the COVID-19 pandemic on their financial strength found good news: “most insurers’ capital levels provided an adequate buffer against a potential shock to their balance sheets.”

Sensitivity to the pandemic was greater for life/health insurers with high asset and mortality risks; insurers with material exposures to mortgage loans; carriers operating in domiciles in higher country-risk tiers; and companies with smaller capital bases.

AM Best believes that the initial negative impact on the P/C insurance industry will likely be in the form of a significant decline in earnings. Reputational risk may also be a problem, as any legal disputes become more visible.

“Insurers are likely to see a significant hit to earnings in 2020, rather than a material decline in risk-adjusted capitalization,” said Mahesh Mistry, senior director, AM Best Rating Services. “Reputational risk in certain markets may also be a problem, as any legal disputes become more visible to consumers, policyholders, regulators and legislators.”

The stress test focused on the impact of COVID-19 on underwriting and assets, as well as available capital. Since the stress test, market conditions have evolved rapidly, and AM Best said it recognizes that insurers “need to be proactive in monitoring economic, regulatory, and industry developments.”

The AM Best stress test did not take into account a scenario in which contracts might be voided by legislation or the courts. But the report warns that if attempts to change contract language on business interruption are “successful in forcing insurers to retroactively apply cover for losses from COVID-19 related business interruption — despite specific exclusions in their policies — these considerations would have grave impacts for the industry, specifically for commercial lines insurers.”

Stress Test Results

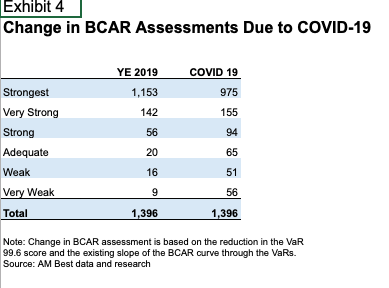

As explained in its Best’s Special Report, “Stress Testing Rated Companies for COVID-19,” the stress test analysis covered approximately 1,400 rating units worldwide, and focused on the impact of COVID-19 on underwriting and assets. Overall results showed that the median Best’s Capital Adequacy Ratio (BCAR) score at VaR 99.6 of the rated population declined to 43% from an estimated year-end 2019 BCAR of 49%, “demonstrating the resilience of the insurance industry.”

Because the insurance market is well capitalized, most companies were able to comfortably withstand the stress test, with no change to the BCAR assessment for 75% of rating units (most of which remain in the “Strongest” category), while 14% moved down by one assessment category.

Property/casualty insurers in the U.S. and Canada performed relatively well, compared with life/annuity and U.S. health insurers. Most companies in the Asia-Pacific market generally performed well also, as did those in Europe, the Middle East, and Africa and in Latin America.

Given the solid capitalization of the U.S. and Canadian P/C markets, most companies saw no change in their BCAR assessments in the stress test. AM Best considers the overall level of risky assets in P/C insurers’ portfolios modest. The median P/C insurer’s BCAR score experienced a modest decline of three points.

The BCARs of most P/C companies in Europe remained largely in the “Strongest” category, similarly to their U.S. counterparts. However, there are concerns regarding business interruption and event cancellation. Reputational risk may also be a concern as insurers dispute claims.

AM Best notes that companies that have performed well on AM Best’s stress test could still face credit rating pressure if conditions deteriorate beyond the prescribed scenarios. According to AM Best, these include a second wave of mortality losses arising from a resurgence of the pandemic; a significant spike in claims experience for commercial lines segments, such as event cancellation, business interruption or trade credit insurance; rulings on contract clauses, results of litigation and government decisions; and further deterioration of financial markets resulting in material investment losses or write-downs of assets.

The property/casualty analysis assumed a moderate increase of 5% in the loss ratio for certain commercial lines. If there is any additional worsening experience for business interruption, event cancellation, workers’ compensation, travel insurance or trade credit insurance, these business lines “will need to be addressed case by case as developments unfold.”

AM Best said it will continue to monitor developments and adjust its analysis.

Topics USA Carriers AM Best Property Casualty Market

Was this article valuable?

Here are more articles you may enjoy.

US Mortgage Rates Rise for Third Straight Week

US Mortgage Rates Rise for Third Straight Week  Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks

Record-Low Danube Water Levels Leave Boats Beached, Reveal Decades-Old Shipwrecks  Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver

Jury Awards 78-Year-Old Victim $56 Million for Crash Caused by Amazon Delivery Driver  Company at Center of Cyclospora Outbreak Complained to White House, Source Says

Company at Center of Cyclospora Outbreak Complained to White House, Source Says From This Issue