A hedge fund that last year delivered its best result ever thanks to catastrophe bonds is now scaling back its position, based on a bet that the market is headed for a rough patch.

Tenax Capital, which has a €100 million ($110 million) portfolio of insurance-linked securities — an asset class that’s dominated by catastrophe bonds — delivered an 18% return last year thanks to the strategy. Now, the fund is converting a large chunk of its stake into cash, Marco della Giacoma, who manages the portfolio, told Bloomberg.

It’s not a great time to be in cat bonds when “everyone is trying to buy, no one wants to sell,” Toby Pughe, an analyst at London-based Tenax, said in an interview.

Hedge Funds’ Mega Returns Set Off Demand Spiral for Catastrophe Bonds

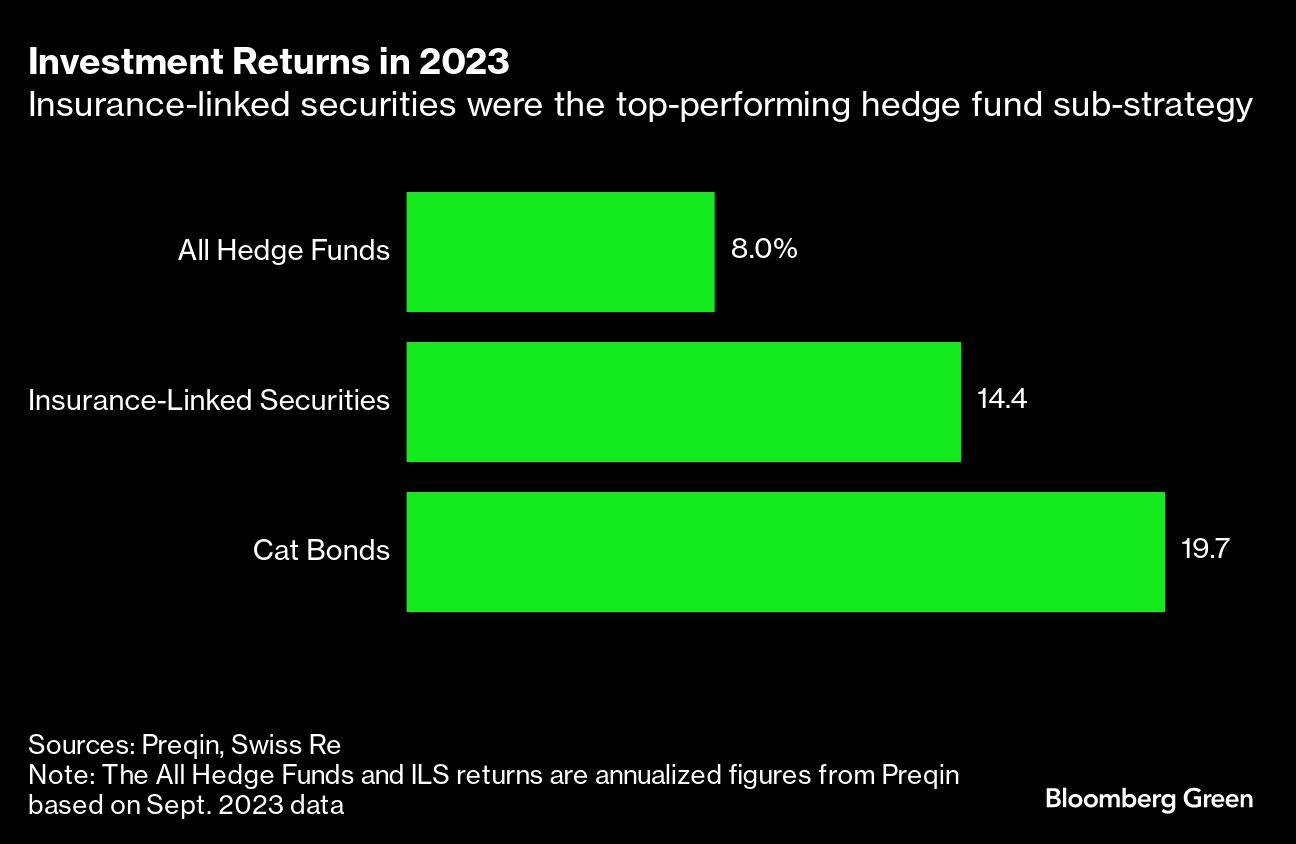

Tenax is among a handful of hedge funds along with Fermat Capital Management and Tangency Capital that delivered record returns in 2023 thanks to bets on insurance-linked securities. According to Preqin, a consultancy that provides data on the alternative asset management industry, ILS was the best performing of all hedge fund strategies last year, delivering more than 14% overall compared with an 8% benchmark. Cat bonds gained 20% in 2023, Swiss Re data show.

Catastrophe bonds reward buyers for taking on insurance-market risk linked to natural disasters such as hurricanes and earthquakes. If catastrophe strikes, bondholders pay out. If it doesn’t, they stand to reap outsized returns.

Issuance this year is expected to rise by about 20% from 2023 to $20 billion, according to GAM Investments, which holds cat bonds on behalf of its clients. Professional investors in insurance-linked securities agree they’re unlikely to see the huge returns of 2023 continue into 2024. But Tenax is more wary than most.

Fermat, the world’s biggest cat bond investor, isn’t retreating, “but we are being a bit picky about which perils we allocate capital to,” said Brett Houghton, a managing director at the hedge fund manager. He also notes that the market “has grown a lot in terms of issuers and types of bonds,” which “gives us a lot more choice.”

Global Insured Losses $ Billion

Last year, everything came together in a uniquely profitable cocktail for investors in the securities. The number of catastrophes was down, while the supply of bonds with double-digit coupons was ample thanks to the panic that followed hurricane Ian in 2022.

That dynamic has since shifted. Growing investor interest has driven up prices on existing bonds and pushed down coupons on new bonds, eroding potential returns.

Tenax says it has walked away from several deals in recent weeks, including a German cat bond with a 5% risk premium. Another offered a 6% risk premium for wind risk in the northeastern US, the kind of bond on which investors would have enjoyed an 8% premium just last year, according to Pughe.

Tenax is now aiming to shift 15% of its portfolio into cash by August, from 8% today. Keeping the position in cash allows it to quickly go back into the cat bond market when prices look more appealing.

“We’re reluctant to invest right now,” said della Giacoma of Tenax. “Psychologically, people have realized we’ve gone to the peak.”

Other cat bond investors are also making adjustments.

Neuberger Berman, which oversees a $3.3 billion ILS portfolio — including $1.4 billion in cat bonds — has decided that now is “a good time to reassess if there are positions to sell,” said Peter DiFiore, a managing director at the New York-based firm. “We’re opportunistically trimming some positions in anticipation that spreads could widen.”

How Do Cat Bonds Work?

Investors in cat bonds make a payment to an insurer when a contractually defined disaster strikes and specific parameters are met, such as wind speed in a hurricane. Investors can lose some or all their money, which is then used to pay insurance claims.

A cat bond’s return is made up of a risk premium —- to compensate for the possibility the disaster will occur — plus a risk-free amount, usually the prevailing Treasury rate. The risk premium for one set of so-called multiperil cat bonds tracked by Swiss Re Capital Markets fell to about 8% in January from roughly 13% a year earlier. The risk premium for a riskier set of cat bonds slipped to about 6% from 9% in the same period.

A key factor behind the shift in pricing is the large volume of cat bonds that matured in January, leaving investors flush with cash that needed to be reinvested.

The maturities “put a lot of capital back into the system,” said MariaGiovanna Guatteri, chief investment officer of Swiss Re Insurance-Linked Investment Advisors Corp., which has about $1.5 billion of assets under management. It’s partly why spreads “are a little out of sync as new issuance is still ramping up.”

GAM Investments expects a risk premium ranging from 8% to 9% this year, which is still higher than the historical range of 4%-6%.

Even at the forecast level, the spread for 2024 will be about four times greater than the bonds’ average one-year forward expected loss of about 2.1%. By comparison, the spread for short-dated corporate bonds with a similar credit rating profile is only 1.4 times the expected loss.

Cat bonds “give you much better compensation for each unit of risk you take” than a lot of other debt instruments, said Ralph Gasser, head of fixed income investment specialists at GAM, whose clients have about $5 billion invested in the securities via three GAM-labeled funds on which Fermat acts as an adviser.

What Bloomberg Intelligence Says:

“A 360% rise in insured losses in the past 30 years from the increased frequency and intensity of natural disasters is leading insurers to hike premiums and exit high-risk areas. At the same time transition risk associated with the assets backing these liabilities is pressuring insurers to cut coverage of polluting sectors in their investment portfolios.”

The fate of the cat bond market partly depends on how weather patterns evolve, a dynamic increasingly influenced by climate change. An area of the tropical Atlantic known as “hurricane alley” saw July-like temperatures in mid-February. And a March report by the National Oceanic and Atmospheric Administration has warned about the “increasing odds” of a La Nina event this summer.

Warmer seas and La Nina are a potent combination that could trigger a “blockbuster” season of storms, according to Accuweather. WeatherBell, another forecaster, warns of “a hurricane season from hell.”

It’s another reason to stay cautious, according to Tenax.

“The season could be pretty active,” said Pughe. “I’ve got the feeling we’re walking into a bit of disaster.”

Photograph: Yachts piled along the shore following Hurricane Ian in Fort Myers, Florida, on Oct. 3, 2022. Photo credit: Eva Marie Uzcategui/Bloomberg

Related:

- Risk Models Behind Insurance-Linked Securities Are Getting a Lot Harder to Crack

- Hedge Funds Rake in Huge Profits Betting on Catastrophe Risk

- Hedge Fund Fermat Has Best Year Ever as Catastrophe Bonds Deliver Record Results

- Catastrophe Bonds – A to Z

Topics Catastrophe

Was this article valuable?

Here are more articles you may enjoy.

Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal

Mapfre to Acquire Safety Insurance for $1.54 Billion in Cash Deal  Company at Center of Cyclospora Outbreak Complained to White House, Source Says

Company at Center of Cyclospora Outbreak Complained to White House, Source Says  After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed

After 55 Years in Florida Insurance, Tom Lynch Reflects on Agencies, Changes Needed