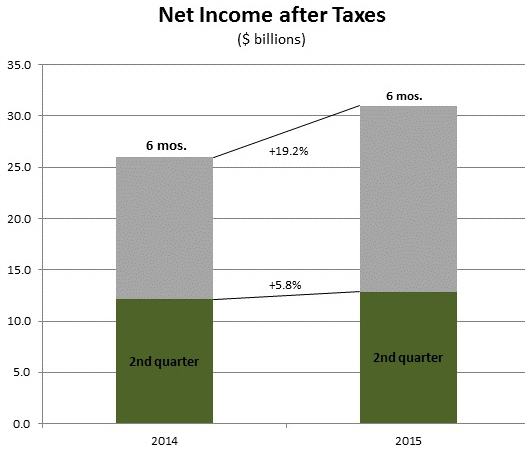

Private U.S. property/casualty insurers’ net income after taxes grew to $31.0 billion in the first half of 2015 from $26.0 billion in the first half of 2014, according to a report today from Verisk Analytics’ ISO unit and the Property Casualty Insurers Association of America (PCI).

Private U.S. P/C insurers’ $31.0 billion net income for the first six months of 2015 represents its highest first-half level since the $32.7 billion recorded for first-half 2007, ISO and PCI noted.

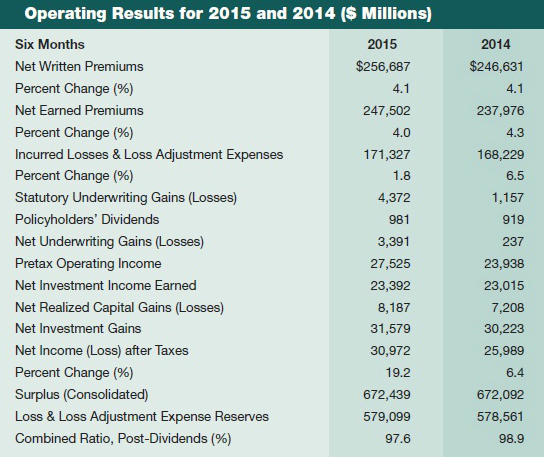

The report also found that insurers’ combined ratio improved to 97.6 percent for first-half 2015 from 98.9 percent for first-half 2014, while their net underwriting gains increased to $3.4 billion from $0.2 billion. Net written premium growth remained unchanged at 4.1 percent for the first half of 2014 and 2015.

Additionally, the insurers’ net investment income increased to $23.4 billion in the first half of 2015 from $23.0 billion a year earlier, and realized capital gains increased to $8.2 billion from $7.2 billion, resulting in $31.6 billion in net investment gains for first-half 2015. The net investment gains were the highest first-half investment gains since the beginning of ISO’s quarterly records in 1986, and the realized capital gains were the highest since the $8.5 billion recorded for 1998.

The report noted that improvements in underwriting results and elevated investment gains pushed insurers’ annualized overall rate of return for first-half 2015 to 9.2 percent from 7.8 percent for first-half 2014. However, the report noted, this is just 0.2 percentage points above the 30-year average annualized rate of return for first-half results.

Underwriting Results

The report said the improvement in underwriting results is mainly due to the growth in earned premiums in excess of the growth in losses and loss adjustment expenses (LLAE). In first-half 2015, earned premiums grew 4.0 percent to $247.5 billion, while LLAE rose just 1.8 percent to $171.3 billion, other underwriting expenses grew 4.7 percent to $71.8 billion, and policyholders’ dividends were unchanged at $1.0 billion. As a result, net underwriting gains increased to $3.4 billion from $0.2 billion.

The report noted that the 1.8 percent rise in LLAE in first-half 2015 compares favorably to the 6.5 percent increase a year earlier.

A decline in catastrophe losses slowed down the rise in overall LLAE, the report found. Private U.S. insurers’ net LLAE from catastrophes declined $2.1 billion to $10.8 billion for first-half 2015 from $13.0 billion a year ago. Net LLAE for losses other than catastrophes rose $5.2 billion, or 3.4 percent, to $160.5 billion in first-half 2015 from $155.2 billion in first-half 2014.

According to the report, direct insured property losses from catastrophes striking the U.S. totaled $10.3 billion in first-half 2015, down $2.3 billion from $12.6 billion in first-half 2014 and $0.6 billion below the $10.9 billion average for the past 10 years.

The report also found that underwriting results benefited from $8.1 billion in favorable development of LLAE reserves in first-half 2015, based on new information and updated estimates for the ultimate cost of claims from prior accident years. The $8.1 billion of favorable reserve development in first-half 2015 follows $7.9 billion of favorable development in first-half 2014.

In addition, net written premiums climbed $10.1 billion, or 4.1 percent, to $256.7 billion in first-half 2015 from $246.6 billion in first-half 2014. The net written premium growth rate of 4.1 percent is unchanged from first-half 2014 and just slightly below the 4.2 percent growth rate for full-year 2014, the report said.

Policyholders’ Surplus Fell Slightly

The report noted that despite insurers’ $31.0 billion in net income after taxes in first-half 2015, the industry’s surplus declined to $672.4 billion as of June 30, 2015 — down $2.8 billion from a record high of $675.2 billion at year-end 2014, mostly because of $20.1 billion in dividends to stockholders and $8.7 billion in unrealized capital losses.

Still, policyholders’ surplus for first-half 2015 remained above any pre-2014 values, the report found. Additions to surplus in first-half 2015 included $31.0 billion in net income after taxes and $4.8 billion in new funds. The deductions from surplus consisted of $8.7 billion in unrealized capital losses on investments (not included in net income), $20.1 billion in dividends to shareholders, and $9.7 billion in miscellaneous charges against surplus.

The report said the $8.7 billion in unrealized capital losses in first-half 2015 represents a $16.5 billion swing from the $7.8 billion in unrealized capital gains for first-half 2014. Miscellaneous charges against surplus grew to $9.7 billion in first-half 2015 from $2.4 billion in first-half 2014.

“While Old Man Winter did his best to disrupt things in the Northeast, during the first half of 2015 insurers overall incurred lower domestic catastrophe losses than they did during the first half of last year due to a relatively quiet tornado season and the slow start to hurricane season,” said Robert Gordon, PCI’s senior vice president for policy development and research.

“Insurers’ combined ratio and rate of return all improved in the first half of 2015, while premium growth and investment income remained relatively stable,” Gordon said.

Still, it’s important to note that U.S. catastrophe losses during the first half of 2015 were only slightly lower than the 10-year average, added Beth Fitzgerald, president of ISO Solutions.

“As the devastation caused by meteorological conditions associated with Hurricane Joaquin highlights, it’s crucial for insurers to remain disciplined in their underwriting and look at analytics to be ready not only for weather disasters but also for other major challenges the future may hold,” she said.

2015 Q2 Results Improved

The report also showed that the P/C insurance industry’s consolidated net income after taxes rose to $12.8 billion in second-quarter 2015, up from $12.1 billion in second-quarter 2014.

Insurers’ annualized rate of return on average surplus increased to 7.6 percent in second-quarter 2015 from 7.3 percent a year earlier.

Net written premiums rose $5.5 billion, or 4.4 percent, to $130.6 billion in second-quarter 2015 from $125.1 billion in second-quarter 2014. The industry’s combined ratio improved to 99.4 percent in second-quarter 2015 from 100.6 percent in second-quarter 2014.

Direct insured losses from catastrophes striking the U.S. in second-quarter 2015 totaled $6.7 billion — down $2.9 billion from the $9.6 billion in direct insured losses caused by catastrophes that struck the U.S. in second-quarter 2014.

The $11.7 billion in net investment income for the industry overall in second-quarter 2015 was $0.1 billion below $11.8 billion for second-quarter 2014.

The ISO/PCI study defines the U.S. P/C insurance industry as all private P/C insurers domiciled in the U.S., including excess and surplus insurers and domestic insurers owned by foreign parents, but excluding state funds for workers’ compensation and other residual market carriers.

Source: ISO/Verisk Analytics, Property Casualty Insurers Association of America

Related:

- P/C Insurance Industry’s Low Unemployment Rate Likely to Go Lower

- Can U.S. P/C Insurers Handle Equity Market Volatility?

- For P/C Insurers, 2014 Was Better Than Average Year

- P/C Insurers’ Surplus Rose, Profitability Fell in 2014’s First 9 Months

Topics USA Catastrophe Carriers Profit Loss Excess Surplus Underwriting Property Casualty

Was this article valuable?

Here are more articles you may enjoy.

FTC Sues Hims & Hers for Sending User Health Info to Meta, Snap

FTC Sues Hims & Hers for Sending User Health Info to Meta, Snap  State Farm to Begin Issuing Dividend Payments to Louisiana Drivers

State Farm to Begin Issuing Dividend Payments to Louisiana Drivers  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  OpenAI Finds Evidence Other AI Agents Escaped Containment as it Widens Probe

OpenAI Finds Evidence Other AI Agents Escaped Containment as it Widens Probe